Вам также может понравиться

- Corporate Governance: A practical guide for accountantsОт EverandCorporate Governance: A practical guide for accountantsРейтинг: 5 из 5 звезд5/5 (1)

- DOC-20240120-WA0000.Документ14 страницDOC-20240120-WA0000.Nikhil KumarОценок пока нет

- CSR AssignmentДокумент7 страницCSR AssignmentNiharikac1995Оценок пока нет

- CorpДокумент3 страницыCorpMuskan KhatriОценок пока нет

- Corporate Social Responsibility Policy: Page 1 of 9Документ9 страницCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurОценок пока нет

- Corporate Social Responsibility RevisedДокумент12 страницCorporate Social Responsibility RevisedVipul NarwalОценок пока нет

- ApplicabilityДокумент4 страницыApplicabilityvasantharaoОценок пока нет

- Corporate Social Responsibility 2013Документ8 страницCorporate Social Responsibility 2013sanjeevseshannaОценок пока нет

- Piyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Документ6 страницPiyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Piyali MitraОценок пока нет

- Unit - 5 Study Material ACGДокумент16 страницUnit - 5 Study Material ACGAbhijeet UpadhyayОценок пока нет

- Warner Bros. Pictures (India) Private LimitedДокумент8 страницWarner Bros. Pictures (India) Private Limitedsaurav singhОценок пока нет

- Indian Companies Act 2013Документ2 страницыIndian Companies Act 2013Waesh AliОценок пока нет

- CHAPTER 7Документ5 страницCHAPTER 7Divyam sharma Roll no 175Оценок пока нет

- Corporate Social ResponsibilityДокумент33 страницыCorporate Social ResponsibilitySharma VishnuОценок пока нет

- CSR Policy PDFДокумент12 страницCSR Policy PDFAkanksha DhandareОценок пока нет

- Companies Act CSRДокумент6 страницCompanies Act CSRNaveen MettaОценок пока нет

- CORPORATE SOCIAL RESPONSIBILITY UNDER COMPANIES ACT 2013Документ41 страницаCORPORATE SOCIAL RESPONSIBILITY UNDER COMPANIES ACT 2013Narender KumarОценок пока нет

- CSR - A Panoramic View - DR Bhasker ChatterjiДокумент39 страницCSR - A Panoramic View - DR Bhasker ChatterjicodemakitОценок пока нет

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Документ12 страницCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiОценок пока нет

- Corporate Social ResponsibilityДокумент8 страницCorporate Social Responsibilityvishad srivastavaОценок пока нет

- CSR Mohammed G A Who Is Currently Pursuing, From NUJS, Kolkata, Discusses Corporate Social Responsibility in IndiaДокумент14 страницCSR Mohammed G A Who Is Currently Pursuing, From NUJS, Kolkata, Discusses Corporate Social Responsibility in IndiaSonu KumarОценок пока нет

- CSR and Sustainability Policy - New PDFДокумент10 страницCSR and Sustainability Policy - New PDFNaniОценок пока нет

- Corporate Social Responsibility Law in IndiaДокумент12 страницCorporate Social Responsibility Law in IndiaShivam RazorОценок пока нет

- Indian Oil Vs Reliance CSR ActivitiesДокумент14 страницIndian Oil Vs Reliance CSR ActivitiesShubhashree SoubhagyarashmiОценок пока нет

- CSR Corporate Governance ReportДокумент7 страницCSR Corporate Governance ReportFariba NabaviОценок пока нет

- Chapter 3Документ16 страницChapter 3Mayank SenОценок пока нет

- CSR PolicyДокумент14 страницCSR PolicyJilla Vishwas100% (1)

- CSR Policy - BilingualДокумент15 страницCSR Policy - BilingualRanjeet DongreОценок пока нет

- AA CSR Rules, 2021Документ5 страницAA CSR Rules, 2021AkshitaОценок пока нет

- CSR PolicyДокумент3 страницыCSR Policyoluyemisi FajogunОценок пока нет

- Unit 4 CGДокумент12 страницUnit 4 CGakashkakade15aОценок пока нет

- CSR LawДокумент16 страницCSR LawKarthikОценок пока нет

- CSR Footnotes2Документ5 страницCSR Footnotes2Priyadarshan NairОценок пока нет

- CSR FaqДокумент3 страницыCSR Faqmerayogdaan123Оценок пока нет

- Corporate Social ResponsibilityДокумент7 страницCorporate Social ResponsibilitySiva Sankar SanthoshОценок пока нет

- An Brief Overview On Corporate Social ResponsibilityДокумент8 страницAn Brief Overview On Corporate Social ResponsibilityMansangat Singh KohliОценок пока нет

- Corporate Social Responsibility: An Overview of The Companies Act, 2013Документ22 страницыCorporate Social Responsibility: An Overview of The Companies Act, 2013Nilesh ShobhaneОценок пока нет

- 0016 Avantika Tijare Assignment 2Документ4 страницы0016 Avantika Tijare Assignment 2AKSHAT SINGHОценок пока нет

- CSR MariottДокумент7 страницCSR MariottPrasanth KumarОценок пока нет

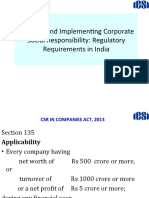

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaДокумент23 страницыPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaОценок пока нет

- Blackbook-Csr in Insurance SectorsДокумент43 страницыBlackbook-Csr in Insurance Sectorsforum67% (3)

- CHAPTER IV-061c1ab81c492b4.39496850Документ14 страницCHAPTER IV-061c1ab81c492b4.39496850RohanОценок пока нет

- Company LawДокумент11 страницCompany LawShaghil NasidОценок пока нет

- Company Law AssignmentДокумент5 страницCompany Law AssignmentABISHEK SRIRAM S 17BLA1008Оценок пока нет

- CSR PolicyДокумент7 страницCSR PolicyRaaj SinghОценок пока нет

- Company Law Research Paper (Ajith)Документ9 страницCompany Law Research Paper (Ajith)Ajith ReddyОценок пока нет

- Changes in CSR Changes in CSR Laws: IndiaДокумент7 страницChanges in CSR Changes in CSR Laws: IndiaAparajita MarwahОценок пока нет

- CSR Policy - Otis IndiaДокумент7 страницCSR Policy - Otis IndiaRakesh SharmaОценок пока нет

- Rar Unit 4Документ12 страницRar Unit 4raval123690Оценок пока нет

- Timken - Corporate-Social-Responsibility-PolicyДокумент5 страницTimken - Corporate-Social-Responsibility-Policyadi.arrow7Оценок пока нет

- Corporate Social ResponsibilityДокумент3 страницыCorporate Social ResponsibilityabcОценок пока нет

- Unit 4 CSRДокумент10 страницUnit 4 CSRRooby SpiritsОценок пока нет

- Should Corporate Social Responsibility Spending Be A Mandatory Legal Requirement?Документ19 страницShould Corporate Social Responsibility Spending Be A Mandatory Legal Requirement?KESHAV RATHI 01Оценок пока нет

- The Corporate Social Responsibility of TATA GroupДокумент27 страницThe Corporate Social Responsibility of TATA GroupBhaumik100% (9)

- Company Law CIA III CSRДокумент6 страницCompany Law CIA III CSRVedant GoswamiОценок пока нет

- DsdsdsdsdsДокумент2 страницыDsdsdsdsdssuvendu beheraОценок пока нет

- Corporate Social Responsibility in IndiaДокумент8 страницCorporate Social Responsibility in IndiaRishabh ChorariaОценок пока нет

- Introduction to Reliance Industries' CSR InitiativesДокумент43 страницыIntroduction to Reliance Industries' CSR InitiativesTusharJoshi0% (2)

- 2 Percent India CSR ReportДокумент4 страницы2 Percent India CSR ReportAditi SinghОценок пока нет

- SubtitleДокумент2 страницыSubtitleRohit KoulОценок пока нет

- SubtitleДокумент2 страницыSubtitleRohit KoulОценок пока нет

- Neumann PDFДокумент16 страницNeumann PDFmirartegalleryОценок пока нет

- Framing Your Self (Ie) - CourseraДокумент1 страницаFraming Your Self (Ie) - CourseraRohit KoulОценок пока нет

- SubtitleДокумент1 страницаSubtitleRohit KoulОценок пока нет

- SubtitleДокумент1 страницаSubtitleRohit KoulОценок пока нет

- SubtitleДокумент1 страницаSubtitleRohit KoulОценок пока нет

- SubtitleДокумент2 страницыSubtitleRohit KoulОценок пока нет

- Plan For Running Training Centre For Women in RajasthanДокумент8 страницPlan For Running Training Centre For Women in Rajasthanmaneesh5Оценок пока нет

- Bierut Spreads Final Real3Документ6 страницBierut Spreads Final Real3Muhammad HassanОценок пока нет

- Corporate PDFДокумент9 страницCorporate PDFAОценок пока нет

- Brewer Dictionary of Phrase & FablesДокумент2 411 страницBrewer Dictionary of Phrase & FablesPlatonicОценок пока нет

- Lesson 1 Local Government's Historical BackgroundДокумент16 страницLesson 1 Local Government's Historical BackgroundLorienelОценок пока нет

- Tolterodine Tartrate (Detrusitol SR)Документ11 страницTolterodine Tartrate (Detrusitol SR)ddandan_2Оценок пока нет

- Google CardboardДокумент3 страницыGoogle CardboardMartínJiménezОценок пока нет

- Digestive System PowerpointДокумент33 страницыDigestive System PowerpointThomas41767% (6)

- Posters Whofic 2020Документ107 страницPosters Whofic 2020Kristel HurtadoОценок пока нет

- The Effect of Warm Ginger Compress on Hypertension Headache Scale in the ElderlyДокумент7 страницThe Effect of Warm Ginger Compress on Hypertension Headache Scale in the Elderlyjembatan gantungОценок пока нет

- Insert - Elecsys Anti-HAV IgM.07026773500.V5.EnДокумент4 страницыInsert - Elecsys Anti-HAV IgM.07026773500.V5.EnVegha NedyaОценок пока нет

- Use of Essential Oils Following Traumatic Burn Injury A Case StudyДокумент12 страницUse of Essential Oils Following Traumatic Burn Injury A Case StudyShandaPrimaDewiОценок пока нет

- Tushar FinalДокумент29 страницTushar FinalRaj Prixit RathoreОценок пока нет

- Vol3issue12018 PDFДокумент58 страницVol3issue12018 PDFpyrockerОценок пока нет

- Adult Health - Soap Note 5Документ3 страницыAdult Health - Soap Note 5api-546259691100% (3)

- Newborn Care Volume 1 2020-1Документ192 страницыNewborn Care Volume 1 2020-1Shyvonne PeirisОценок пока нет

- NurseCorps Part 8Документ24 страницыNurseCorps Part 8smith.kevin1420344Оценок пока нет

- Topical Agents and Dressings For Local Burn Wound CareДокумент25 страницTopical Agents and Dressings For Local Burn Wound CareViresh Upase Roll No 130. / 8th termОценок пока нет

- Risk for Infection AssessmentДокумент7 страницRisk for Infection AssessmentLouis RoderosОценок пока нет

- Dowtherm TДокумент3 страницыDowtherm Tthehoang12310Оценок пока нет

- Introduction To Public Health... 1stДокумент37 страницIntroduction To Public Health... 1stNELSONJD20195100% (3)

- Family Case AnalysisДокумент194 страницыFamily Case AnalysisDianneОценок пока нет

- 100-Bed General Hospital LayoutДокумент1 страница100-Bed General Hospital LayoutAshish chauhanОценок пока нет

- Hvis Msds PDFДокумент6 страницHvis Msds PDFsesbasar sitohangОценок пока нет

- Birads PosterДокумент1 страницаBirads PosterGopalarathnam BalachandranОценок пока нет

- Bio-Oil® Product ManualДокумент60 страницBio-Oil® Product ManualguitarristaclasicosdnОценок пока нет

- S. No Name and Address Form 25 Dated Validupto Form 28 Dated Validupto 1 List of Pharmaceuticals Manufacturing CompaniesДокумент52 страницыS. No Name and Address Form 25 Dated Validupto Form 28 Dated Validupto 1 List of Pharmaceuticals Manufacturing CompaniesSimon YiuОценок пока нет

- The Doctor-Patient Relationship and Interviewing TechniquesДокумент50 страницThe Doctor-Patient Relationship and Interviewing TechniquesPranay KumarОценок пока нет

- AIIMS Bibinagar Recruitment for Faculty PostsДокумент22 страницыAIIMS Bibinagar Recruitment for Faculty PostsavinashОценок пока нет

- Carlin Smith Child Abuse FinalДокумент12 страницCarlin Smith Child Abuse FinalCarlin SmithОценок пока нет

- Domestic Physician HeringДокумент490 страницDomestic Physician Heringskyclad_21Оценок пока нет

- 11 - Comfort, Rest and Sleep Copy 6Документ28 страниц11 - Comfort, Rest and Sleep Copy 6Abdallah AlasalОценок пока нет

- Class 7 PolityДокумент10 страницClass 7 PolityNakka nikithaОценок пока нет

- The Costly Business of DiscriminationДокумент46 страницThe Costly Business of DiscriminationCenter for American Progress100% (1)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffОт Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffРейтинг: 5 из 5 звезд5/5 (11)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoОт Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoРейтинг: 5 из 5 звезд5/5 (20)

- Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) (The Surrounded by Idiots Series) by Thomas Erikson: Key Takeaways, Summary & AnalysisОт EverandSurrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) (The Surrounded by Idiots Series) by Thomas Erikson: Key Takeaways, Summary & AnalysisРейтинг: 4.5 из 5 звезд4.5/5 (2)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeОт EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeРейтинг: 4.5 из 5 звезд4.5/5 (85)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterОт EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterРейтинг: 5 из 5 звезд5/5 (1)

- The First Minute: How to start conversations that get resultsОт EverandThe First Minute: How to start conversations that get resultsРейтинг: 4.5 из 5 звезд4.5/5 (55)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverОт EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverРейтинг: 4.5 из 5 звезд4.5/5 (186)

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurОт Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurРейтинг: 4 из 5 звезд4/5 (2)

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobОт EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobРейтинг: 4.5 из 5 звезд4.5/5 (36)

- Get to the Point!: Sharpen Your Message and Make Your Words MatterОт EverandGet to the Point!: Sharpen Your Message and Make Your Words MatterРейтинг: 4.5 из 5 звезд4.5/5 (280)

- Think Faster, Talk Smarter: How to Speak Successfully When You're Put on the SpotОт EverandThink Faster, Talk Smarter: How to Speak Successfully When You're Put on the SpotРейтинг: 5 из 5 звезд5/5 (1)

- Think and Grow Rich (1937 Edition): The Original 1937 Unedited EditionОт EverandThink and Grow Rich (1937 Edition): The Original 1937 Unedited EditionРейтинг: 5 из 5 звезд5/5 (77)