Вам также может понравиться

- Chapter 7 Accounting For Franchise Operations FranchisorДокумент15 страницChapter 7 Accounting For Franchise Operations FranchisorKaren BalibalosОценок пока нет

- Afar QuestionsДокумент16 страницAfar QuestionsJessarene Fauni Depante50% (18)

- Home Office, Branch and Agency Accounting: Problem 11-1: True or FalseДокумент13 страницHome Office, Branch and Agency Accounting: Problem 11-1: True or FalseVenz Lacre100% (1)

- Advanced Accounting Home Office, Branch and Agency TransactionsДокумент7 страницAdvanced Accounting Home Office, Branch and Agency TransactionsMajoy Bantoc100% (1)

- Accounting Policies, Changes in Accounting Estimates and ErrorsДокумент6 страницAccounting Policies, Changes in Accounting Estimates and ErrorsGlen JavellanaОценок пока нет

- Chapter 5 - Teacher's Manual - Afar Part 1Документ15 страницChapter 5 - Teacher's Manual - Afar Part 1Mayeth BotinОценок пока нет

- Chapter 10Документ9 страницChapter 10chan.charanchan100% (1)

- Insurance Contracts ChapterДокумент10 страницInsurance Contracts ChapterGloowwjОценок пока нет

- DBP V ArcillaДокумент137 страницDBP V ArcillajeysonregОценок пока нет

- Prelim Quiz 001 - Joint Arrangements: Contributions Profit andДокумент3 страницыPrelim Quiz 001 - Joint Arrangements: Contributions Profit andJashim Usop100% (1)

- Corporation LiquidationДокумент2 страницыCorporation LiquidationPatrishaОценок пока нет

- VELUNTA - Ass. in ASTДокумент4 страницыVELUNTA - Ass. in ASTLiberty VeluntaОценок пока нет

- 11 - Substantive Tests of Property, Plant and EquipmentДокумент27 страниц11 - Substantive Tests of Property, Plant and EquipmentArleneCastroОценок пока нет

- Acctg 11 Q1 - FinalsДокумент8 страницAcctg 11 Q1 - FinalsIvy SaliseОценок пока нет

- Afar 2 Module CH 4 PDFДокумент20 страницAfar 2 Module CH 4 PDFRazmen Ramirez PintoОценок пока нет

- Business Combinations: Fees of Finders and Registration Fees Consultants For Equity Securities IssuedДокумент5 страницBusiness Combinations: Fees of Finders and Registration Fees Consultants For Equity Securities IssuedHanna Mendoza De Ocampo0% (3)

- Chapter 8 - Teacher's Manual - Afar Part 1Документ7 страницChapter 8 - Teacher's Manual - Afar Part 1Angelic100% (3)

- Corporate Liquidation & Reorganization Quiz ResultsДокумент8 страницCorporate Liquidation & Reorganization Quiz ResultsAngelica DuarteОценок пока нет

- Joint operation profit and cash received calculationДокумент1 страницаJoint operation profit and cash received calculationelsana philip100% (1)

- AFAR - FINAL EXAMINATION - 03.22.2019 Wo ANSWERSДокумент5 страницAFAR - FINAL EXAMINATION - 03.22.2019 Wo ANSWERSrain suansingОценок пока нет

- Advac 1 Corporate Liquidationdoc PDFДокумент3 страницыAdvac 1 Corporate Liquidationdoc PDFaldrinОценок пока нет

- APPLIED AUDITING PRELIM EXAMДокумент9 страницAPPLIED AUDITING PRELIM EXAMChristopher NogotОценок пока нет

- Joint Arrangement With The AssignmentДокумент28 страницJoint Arrangement With The AssignmentIvan Bendiola0% (2)

- Acquiring IMMATURE: Estimating GoodwillДокумент1 страницаAcquiring IMMATURE: Estimating GoodwillRiselle Ann Sanchez50% (2)

- Use The Fact Pattern Below For The Next Three Independent CasesДокумент5 страницUse The Fact Pattern Below For The Next Three Independent CasesMichael Bongalonta0% (1)

- Pracc2 ReviewerДокумент8 страницPracc2 ReviewerLucas GalingОценок пока нет

- Sample partnership liquidation problemsДокумент3 страницыSample partnership liquidation problemsJay Bee SalvadorОценок пока нет

- Chapter 14 - Bus. Combination Part 2Документ16 страницChapter 14 - Bus. Combination Part 2PutmehudgJasdОценок пока нет

- Corporate LiquidationДокумент4 страницыCorporate LiquidationMayla Lei PabloОценок пока нет

- Multiple choice questions on business combinationsДокумент12 страницMultiple choice questions on business combinationsHerwin Mae BoclarasОценок пока нет

- Module 1 Home Office and Branch Accounting General ProceduresДокумент4 страницыModule 1 Home Office and Branch Accounting General ProceduresDaenielle EspinozaОценок пока нет

- Arpia Lovely Rose Quiz - Chapter 6 - Joint Arrangements - 2020 EditionДокумент4 страницыArpia Lovely Rose Quiz - Chapter 6 - Joint Arrangements - 2020 EditionLovely ArpiaОценок пока нет

- Chapter 13 Multiple Choice QuestionsДокумент8 страницChapter 13 Multiple Choice QuestionsMel ChuaОценок пока нет

- Franchise: Jan. 1, 20x1 Feb. 1, 20x1 Apr. 1, 20x1Документ4 страницыFranchise: Jan. 1, 20x1 Feb. 1, 20x1 Apr. 1, 20x1Vine AlparitoОценок пока нет

- D. All of ThemДокумент6 страницD. All of ThemRyan CapistranoОценок пока нет

- Business Combination NotesДокумент3 страницыBusiness Combination NotesKenneth Calzado67% (3)

- CPA Exam Chapter 2 ReviewДокумент7 страницCPA Exam Chapter 2 Reviewlopo100% (1)

- Corporate Liquidation Quiz 5docxДокумент5 страницCorporate Liquidation Quiz 5docxAngelica Duarte33% (6)

- Use The Following Information For The Next Seven Questions:: Activity 2.4Документ2 страницыUse The Following Information For The Next Seven Questions:: Activity 2.4Tine Vasiana Duerme0% (1)

- AFAR Final Preboard 2018 PDFДокумент22 страницыAFAR Final Preboard 2018 PDFcardos cherryОценок пока нет

- Joint Operation Case 1 reconciliationДокумент4 страницыJoint Operation Case 1 reconciliationCarl Adrian ValdezОценок пока нет

- Joint Operation Case 2Документ7 страницJoint Operation Case 2Carl Adrian ValdezОценок пока нет

- Asset Liabilities + Owner'S EquityДокумент4 страницыAsset Liabilities + Owner'S EquitydenixngОценок пока нет

- Pea Company Soup Company Debit Credit Debit Credit: Income StatementДокумент2 страницыPea Company Soup Company Debit Credit Debit Credit: Income StatementSARA ALKHODAIRОценок пока нет

- Supply Chain - ExcerciseДокумент22 страницыSupply Chain - ExcerciseMd. Ariful HassanОценок пока нет

- Solution Chapter 6 Joint ArrangementsДокумент17 страницSolution Chapter 6 Joint ArrangementsMariz QuintoОценок пока нет

- Joint Arrangement Problems and SolutionsДокумент15 страницJoint Arrangement Problems and SolutionsVernnОценок пока нет

- Application Problems 1 Through 3Документ5 страницApplication Problems 1 Through 3api-4072164490% (1)

- Problem 2-2A: InstructionsДокумент6 страницProblem 2-2A: Instructionspratik2000Оценок пока нет

- Excel For Accounting CycleДокумент15 страницExcel For Accounting CycleLois RazonОценок пока нет

- UntitledДокумент2 страницыUntitledjima nugusОценок пока нет

- Q and A PartnershipДокумент9 страницQ and A PartnershipFaker MejiaОценок пока нет

- Journal Transactions: Dwyer Delivery ServiceДокумент10 страницJournal Transactions: Dwyer Delivery ServiceClara Saty M LambaОценок пока нет

- The Van Boheemen 1Документ3 страницыThe Van Boheemen 1PrasangОценок пока нет

- Aggregate Consumption FunctionДокумент4 страницыAggregate Consumption FunctionPalos DoseОценок пока нет

- AssigmentДокумент1 страницаAssigmentM. AlkamelОценок пока нет

- Excel For Accounting CycleДокумент6 страницExcel For Accounting CycleSANDEEP KUMARОценок пока нет

- Lot Size Fixed or Lot For Lot: Steps in The MRP Process Nett, Explode, OffsetДокумент2 страницыLot Size Fixed or Lot For Lot: Steps in The MRP Process Nett, Explode, OffsetAslam SoniОценок пока нет

- Tugas Pert 9 AKL LANJT 1 (P6-1) - Siti Rahmah - 2019210010Документ2 страницыTugas Pert 9 AKL LANJT 1 (P6-1) - Siti Rahmah - 2019210010Siti RahmahОценок пока нет

- Module 2 Handout 2 Business ComДокумент3 страницыModule 2 Handout 2 Business ComPara Sa PictureОценок пока нет

- INC Resume TemplateДокумент1 страницаINC Resume TemplateVenz LacreОценок пока нет

- Afar Crc-Ace PW SolutionsДокумент18 страницAfar Crc-Ace PW SolutionsVenz Lacre100% (1)

- CAT B I Can Save The Earth PDFДокумент2 страницыCAT B I Can Save The Earth PDFVenz LacreОценок пока нет

- Nonprofit OrganizationДокумент5 страницNonprofit OrganizationVenz LacreОценок пока нет

- Cannon Ball Review Part 4Документ20 страницCannon Ball Review Part 4Jhopel Casagnap Eman100% (1)

- Storytelling Etc 2019 Guidelines and Mechanics 1Документ4 страницыStorytelling Etc 2019 Guidelines and Mechanics 1Venz LacreОценок пока нет

- Learning Session Storytelling Invite PDFДокумент1 страницаLearning Session Storytelling Invite PDFVenz LacreОценок пока нет

- PH Tax in A Dot Amendments Withholding Tax Regulations Train Law 21mar2018 PDFДокумент9 страницPH Tax in A Dot Amendments Withholding Tax Regulations Train Law 21mar2018 PDFVenz LacreОценок пока нет

- Tariff and Custom CodeДокумент12 страницTariff and Custom CodeAmy Olaes Dulnuan100% (1)

- Chapter11.Flexible Budgeting and The Management of Overhead and Support Activity CostsДокумент38 страницChapter11.Flexible Budgeting and The Management of Overhead and Support Activity CostsMangoStarr Aibelle Vegas75% (4)

- 00 Test Bank Title PageДокумент1 страница00 Test Bank Title PageVenz LacreОценок пока нет

- Chapter 5 - Teacher's Manual - Afar Part 1Документ15 страницChapter 5 - Teacher's Manual - Afar Part 1Mayeth BotinОценок пока нет

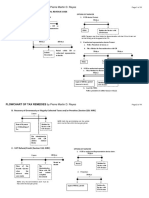

- Flowchart of Tax Remedies 2017 Update PRДокумент11 страницFlowchart of Tax Remedies 2017 Update PRMarjorie Kate CresciniОценок пока нет

- Chapter 21 FinalДокумент16 страницChapter 21 FinalMichael HuОценок пока нет

- If Trees Could Talk Kindergarten Storytelling PieceДокумент1 страницаIf Trees Could Talk Kindergarten Storytelling PieceVenz LacreОценок пока нет

- Chapter 9 Consignment Sales ProblemsДокумент4 страницыChapter 9 Consignment Sales ProblemsVenz LacreОценок пока нет

- 4Документ7 страниц4Venz LacreОценок пока нет

- Chapter 5 - Teacher's Manual - Afar Part 1Документ15 страницChapter 5 - Teacher's Manual - Afar Part 1Mayeth BotinОценок пока нет

- Bank Recon - Summary - A Project of Barters PHДокумент3 страницыBank Recon - Summary - A Project of Barters PHkenneth pugalОценок пока нет

- Partnership - Part 2: Problem 2-1: True or FalseДокумент8 страницPartnership - Part 2: Problem 2-1: True or FalseVenz LacreОценок пока нет

- Chapter 1 - Teacher's Manual - Afar Part 1-1Документ10 страницChapter 1 - Teacher's Manual - Afar Part 1-1Mayeth BotinОценок пока нет

- Sales Agency Pledge MortgageДокумент13 страницSales Agency Pledge MortgagePhilip Castro67% (3)

- Leris Online Step by StepДокумент22 страницыLeris Online Step by StepPRC Board85% (13)

- #02 Conceptual FrameworkДокумент5 страниц#02 Conceptual FrameworkZaaavnn VannnnnОценок пока нет

- 2009 F-9 Class NotesДокумент4 страницы2009 F-9 Class NotesClarize R. MabiogОценок пока нет

- Auditing Theory 250 QuestionsДокумент39 страницAuditing Theory 250 Questionsxxxxxxxxx75% (4)

- Donor's Tax Rates and ExemptionsДокумент7 страницDonor's Tax Rates and ExemptionsRanel Clark D. Tabios50% (2)

- DERIVATIVES ACCOUNTINGДокумент5 страницDERIVATIVES ACCOUNTINGVenz LacreОценок пока нет

- 10 PDFДокумент5 страниц10 PDFIndira BanerjeeОценок пока нет

- Danh sách đ tài Đ c nglunvăn ề ề ươ ậ HK1/19-20Документ47 страницDanh sách đ tài Đ c nglunvăn ề ề ươ ậ HK1/19-20LONG Trương MinhОценок пока нет

- Day Trading Money ManagementДокумент8 страницDay Trading Money ManagementJoe PonziОценок пока нет

- 6Tdvfutfrfr-S: of ofДокумент2 страницы6Tdvfutfrfr-S: of ofhim vermaОценок пока нет

- Delta Ia-Mds VFDB I TC 20070719Документ2 страницыDelta Ia-Mds VFDB I TC 20070719homa54404Оценок пока нет

- Lec4 WWW Cs Sjtu Edu CNДокумент134 страницыLec4 WWW Cs Sjtu Edu CNAUSTIN ALTONОценок пока нет

- Top 1000 World Banks Weather PandemicДокумент4 страницыTop 1000 World Banks Weather PandemicBryan MendozaОценок пока нет

- Metkon Micracut 151 201 enДокумент4 страницыMetkon Micracut 151 201 enmuqtadirОценок пока нет

- Dan John Case Study - Scaling with Facebook AdsДокумент5 страницDan John Case Study - Scaling with Facebook AdsZeynep ÖzenОценок пока нет

- Hydro Skimming Margins Vs Cracking MarginsДокумент78 страницHydro Skimming Margins Vs Cracking MarginsWon Jang100% (1)

- Nice - Folder - Bar - System - en Mbar HighlightedДокумент16 страницNice - Folder - Bar - System - en Mbar HighlightedSamastha Nair SamajamОценок пока нет

- A Tidy GhostДокумент13 страницA Tidy Ghost12345aliОценок пока нет

- 1 ST QTR MSlight 2023Документ28 страниц1 ST QTR MSlight 2023Reynald TayagОценок пока нет

- III International Congress on Teaching Cases Related to Public and Nonprofit Marketing: Nestlé's CSR in Moga District, IndiaДокумент8 страницIII International Congress on Teaching Cases Related to Public and Nonprofit Marketing: Nestlé's CSR in Moga District, IndiaIshita KotakОценок пока нет

- 2 - SM Watches Father's Day Promotion - June 2023Документ11 страниц2 - SM Watches Father's Day Promotion - June 2023Shekhar NillОценок пока нет

- Tune boilers regularlyДокумент2 страницыTune boilers regularlyEliecer Romero MunozОценок пока нет

- Overview of Sharepoint Foundation and Sharepoint Server: Collaboration and Social ComputingДокумент15 страницOverview of Sharepoint Foundation and Sharepoint Server: Collaboration and Social ComputingHarold Vargas MorenoОценок пока нет

- About 1,61,00,00,000 Results (0.20 Seconds) : All Books Shopping Videos More Settings ToolsДокумент2 страницыAbout 1,61,00,00,000 Results (0.20 Seconds) : All Books Shopping Videos More Settings Toolsupen097Оценок пока нет

- Repair Guides - Wiring Diagrams - Wiring DiagramsДокумент18 страницRepair Guides - Wiring Diagrams - Wiring DiagramsAlvaro PantojaОценок пока нет

- Data Structures CompleteДокумент255 страницData Structures Completemovie world50% (2)

- Antipsychotic DrugsДокумент23 страницыAntipsychotic DrugsASHLEY DAWN BUENAFEОценок пока нет

- Assignment: Name: Armish Imtiaz Roll No: 37: TopicДокумент3 страницыAssignment: Name: Armish Imtiaz Roll No: 37: TopicKhubaib ImtiazОценок пока нет

- NFL 101 Breaking Down The Basics of 2-Man CoverageДокумент10 страницNFL 101 Breaking Down The Basics of 2-Man Coveragecoachmark285Оценок пока нет

- Earth / Ground Test (Version 1) : Za'immul Na'imДокумент4 страницыEarth / Ground Test (Version 1) : Za'immul Na'imMd Rodi BidinОценок пока нет

- 3 Zones in 3 Weeks. Devops With Terraform, Ansible and PackerДокумент24 страницы3 Zones in 3 Weeks. Devops With Terraform, Ansible and Packermano555Оценок пока нет

- Trash and Recycling Space Allocation GuideДокумент24 страницыTrash and Recycling Space Allocation GuideJohan RodriguezОценок пока нет

- Seminar On Biodegradable PolymersДокумент19 страницSeminar On Biodegradable Polymerskeyur33% (3)

- BITUMINOUS MIX DESIGNДокумент4 страницыBITUMINOUS MIX DESIGNSunil BoseОценок пока нет

- Terms and conditions for FLAC 3D licensingДокумент2 страницыTerms and conditions for FLAC 3D licensingseif17Оценок пока нет

- Disaster Risk Reduction and LivelihoodsДокумент178 страницDisaster Risk Reduction and LivelihoodsFeinstein International Center100% (1)