Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Overview of NTPC Finance FunctionДокумент17 страницOverview of NTPC Finance FunctionSamОценок пока нет

- Starbucks StoryДокумент27 страницStarbucks Storymushi_ak4u100% (15)

- Zig Ziglars Secrets of Closing The Sale PDFДокумент10 страницZig Ziglars Secrets of Closing The Sale PDFhuguesОценок пока нет

- A Case Study Ford Motor CompanyДокумент5 страницA Case Study Ford Motor Companysaleem razaОценок пока нет

- Training Module For SHG Book Keepers: SHG Books of Records Duration: 3 DaysДокумент32 страницыTraining Module For SHG Book Keepers: SHG Books of Records Duration: 3 DaysONYANGO JohnnyОценок пока нет

- Dwnload Full Managerial Accounting 9th Edition Crosson Solutions Manual PDFДокумент35 страницDwnload Full Managerial Accounting 9th Edition Crosson Solutions Manual PDFfistularactable.db4f100% (9)

- 2021 Annual Member StatementДокумент9 страниц2021 Annual Member Statementkz2w4tx6prОценок пока нет

- Making Globalization Work: Joseph E. StiglitzДокумент26 страницMaking Globalization Work: Joseph E. StiglitzsaraaqilОценок пока нет

- What Is ChangeДокумент3 страницыWhat Is ChangeCalonneFrОценок пока нет

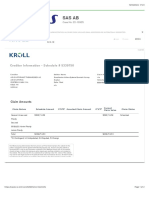

- Kroll Restructuring AdministrationДокумент2 страницыKroll Restructuring AdministrationMarОценок пока нет

- Sales of Goods ActДокумент56 страницSales of Goods ActCharu ModiОценок пока нет

- AER Presentation On RAB MultiplesДокумент18 страницAER Presentation On RAB MultiplesKGОценок пока нет

- Deductible Vs Excess (Insurance)Документ1 страницаDeductible Vs Excess (Insurance)gopinathan_karuthedaОценок пока нет

- Moyer FINANZAS CUESTIONARIOДокумент26 страницMoyer FINANZAS CUESTIONARIOMariana Cordova100% (2)

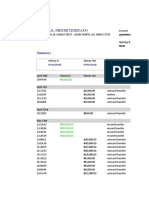

- Customer StatementДокумент20 страницCustomer StatementDonaldОценок пока нет

- Paige Begody Resume 11 2 23Документ1 страницаPaige Begody Resume 11 2 23api-700591109Оценок пока нет

- Implementation of Fake Product Review Monitoring System and Real Review Generation by Using Data Mining MechanismДокумент10 страницImplementation of Fake Product Review Monitoring System and Real Review Generation by Using Data Mining MechanismAjayi FelixОценок пока нет

- Chapter 6Документ20 страницChapter 6shiv kumarОценок пока нет

- POs Pre Joining Study Material PDFДокумент152 страницыPOs Pre Joining Study Material PDFKushagra Pratap SinghОценок пока нет

- COBIT 2019 Foundation ExamДокумент28 страницCOBIT 2019 Foundation ExamVitor Suzarte100% (1)

- Sales: P1-,27A, OAO - 1LZB, O00 - )Документ1 страницаSales: P1-,27A, OAO - 1LZB, O00 - )Lovely Mae LariosaОценок пока нет

- Data Analytics: This Study Resource Was Shared ViaДокумент5 страницData Analytics: This Study Resource Was Shared ViaAmeya SakpalОценок пока нет

- MGT602 Final Subjective by USMAN ATTARIДокумент12 страницMGT602 Final Subjective by USMAN ATTARImaryamОценок пока нет

- Cel2106 SCL Worksheet Week 4Документ3 страницыCel2106 SCL Worksheet Week 4raed nasrallahОценок пока нет

- SNGPL - Web BillДокумент1 страницаSNGPL - Web BillHartly MarieОценок пока нет

- Design and Construction of Offshore Concrete Structures: February 2017Документ18 страницDesign and Construction of Offshore Concrete Structures: February 2017Suraj PandeyОценок пока нет

- eBayReturnLabel 5135454522 PDFДокумент2 страницыeBayReturnLabel 5135454522 PDFsherry webberОценок пока нет

- L6 - Developing A Brand NameДокумент15 страницL6 - Developing A Brand NameJohn ManawisОценок пока нет

- Green Marketing Goes NegativeДокумент8 страницGreen Marketing Goes NegativeFrankОценок пока нет

- Production Logistics and Human-Computer Interaction - State-Of-The-Art, Challenges and Requirements For The FutureДокумент19 страницProduction Logistics and Human-Computer Interaction - State-Of-The-Art, Challenges and Requirements For The FutureBladimir MendezОценок пока нет