Вам также может понравиться

- 02 Project Insight OverviewДокумент17 страниц02 Project Insight OverviewMateoLagardoОценок пока нет

- Auditing The Art and Science of Assurance Engagements by Alvin Arens Z Liborgpdf PDF Free 264 289 DikonversiДокумент37 страницAuditing The Art and Science of Assurance Engagements by Alvin Arens Z Liborgpdf PDF Free 264 289 DikonversiLabora Dwi PutriОценок пока нет

- AuditingДокумент27 страницAuditingaazamchОценок пока нет

- Audit Engagement Letter FarДокумент4 страницыAudit Engagement Letter FarSyed Zulqarnain HaiderОценок пока нет

- Exercises 01 - EMS LAC, IG, Issue 4.2, 10-23-08Документ61 страницаExercises 01 - EMS LAC, IG, Issue 4.2, 10-23-08victor100% (1)

- Audit I-Chapter OneДокумент7 страницAudit I-Chapter Onethedalesh weldeОценок пока нет

- Auditing & Assurance Principles-Lesson 1Документ12 страницAuditing & Assurance Principles-Lesson 1Joe P PokaranОценок пока нет

- Assignment Set-1: Q.1 Discuss Is Auditing Is A Luxury AnsДокумент14 страницAssignment Set-1: Q.1 Discuss Is Auditing Is A Luxury Ansvaishnavbipin5555Оценок пока нет

- Name: Dilip Kumar. G Roll No.: 520947355Документ10 страницName: Dilip Kumar. G Roll No.: 520947355Dilipk86Оценок пока нет

- Master of Business Administration - MBA Semester 3Документ16 страницMaster of Business Administration - MBA Semester 3Mihir DesaiОценок пока нет

- Chapter 7 AuditingДокумент25 страницChapter 7 AuditingMisshtaCОценок пока нет

- AUD It - A N Over ViewДокумент27 страницAUD It - A N Over ViewYamateОценок пока нет

- 7.0 Topic 7 Public Sector Auditing 7.1 S PDFДокумент17 страниц7.0 Topic 7 Public Sector Auditing 7.1 S PDFhezronОценок пока нет

- Chapter 02 Overview of AuditingДокумент26 страницChapter 02 Overview of AuditingRichard de LeonОценок пока нет

- Chapter 2 & 4 AuditingДокумент23 страницыChapter 2 & 4 AuditingAimae Inot MalinaoОценок пока нет

- Ayub Aslam & Co.Документ213 страницAyub Aslam & Co.Usman Afzal100% (1)

- Mid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Документ7 страницMid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Ashilla Nadya AmanyОценок пока нет

- Chapter 1-3 SummaryДокумент10 страницChapter 1-3 SummaryLovely Jane Raut CabiltoОценок пока нет

- Lesson Number: 02 Topic: Audits of Financial Information Learning ObjectivesДокумент18 страницLesson Number: 02 Topic: Audits of Financial Information Learning ObjectivesDavid alfonsoОценок пока нет

- 10.1007@978 3 319 90521 11Документ14 страниц10.1007@978 3 319 90521 11Ibtissam EljedaouyОценок пока нет

- Module - Auditing - Chapter 2Документ10 страницModule - Auditing - Chapter 2Kathleen Ebuen EncinaОценок пока нет

- Presentation 2Документ35 страницPresentation 2Ma. Elene MagdaraogОценок пока нет

- Manonmaniam Sundaranar University: For More Information Visit: HTTP://WWW - Msuniv.ac - inДокумент100 страницManonmaniam Sundaranar University: For More Information Visit: HTTP://WWW - Msuniv.ac - inAproviderОценок пока нет

- Module 2 - Introduction To FS AuditДокумент5 страницModule 2 - Introduction To FS AuditLysss EpssssОценок пока нет

- General Types of Audit: Review QuestionsДокумент7 страницGeneral Types of Audit: Review QuestionsRomulus AronОценок пока нет

- Auditing in Cis: President Ramon Magsaysay State University College of Accountancy and Business AdministrationДокумент13 страницAuditing in Cis: President Ramon Magsaysay State University College of Accountancy and Business AdministrationSharmaine VillalobosОценок пока нет

- Topic 1 - Audit - An OverviewДокумент22 страницыTopic 1 - Audit - An OverviewPara Sa PictureОценок пока нет

- C9ay1 HsijbДокумент15 страницC9ay1 HsijbEyob FirstОценок пока нет

- Audit IIДокумент85 страницAudit IISamuel DebebeОценок пока нет

- Module 1 Audit An OverviewДокумент27 страницModule 1 Audit An OverviewGONZALES, MICA ANGEL A.Оценок пока нет

- In Depth Guide To Public Company AuditingДокумент20 страницIn Depth Guide To Public Company AuditingAhmed Rasool BaigОценок пока нет

- AUDITING PRINCIPLES I - NotesДокумент69 страницAUDITING PRINCIPLES I - Notesyebegashet100% (1)

- Mcs AuditДокумент28 страницMcs AuditVaibhav BanjanОценок пока нет

- Chapter 3 (Auditing Theory)Документ7 страницChapter 3 (Auditing Theory)Rae YaОценок пока нет

- Sabid - MC Neill - Bsma - 4 - I Am Lost! I Know I UnderstandДокумент11 страницSabid - MC Neill - Bsma - 4 - I Am Lost! I Know I UnderstandMC NEILL SABIDОценок пока нет

- ACC115 ModuleДокумент68 страницACC115 ModuleMaricar CachilaОценок пока нет

- PSA 120, PSA 200, AND Attestation Audit ACCTG 4110: Agreed Upon-ProceduresДокумент12 страницPSA 120, PSA 200, AND Attestation Audit ACCTG 4110: Agreed Upon-ProceduresMC NEILL SABIDОценок пока нет

- Solman Arens Chapeter 26Документ14 страницSolman Arens Chapeter 26Rizal Pandu NugrohoОценок пока нет

- Audit I CHAPTER 2Документ38 страницAudit I CHAPTER 2Samuel GirmaОценок пока нет

- Smieliauskas 6e - Solutions Manual - Chapter 01Документ8 страницSmieliauskas 6e - Solutions Manual - Chapter 01scribdteaОценок пока нет

- AUD 2 Overview of AuditДокумент9 страницAUD 2 Overview of AuditJayron NonguiОценок пока нет

- Audit Term PaperДокумент39 страницAudit Term Papersamuel kebedeОценок пока нет

- Chapter I - Overview of AuditДокумент16 страницChapter I - Overview of AuditMarj Manlagnit100% (1)

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Документ18 страницAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizОценок пока нет

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Документ18 страницAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizОценок пока нет

- My ReportДокумент5 страницMy ReportZaber ChowdhuryОценок пока нет

- Mod 1Документ15 страницMod 1Marie claire Delos santosОценок пока нет

- In-Depth Guide To Public Company Auditing:: The Financial Statement AuditДокумент20 страницIn-Depth Guide To Public Company Auditing:: The Financial Statement AuditThùy Vân NguyễnОценок пока нет

- Topic 1 INTRO TO AUDITING - 211114 - 152450Документ7 страницTopic 1 INTRO TO AUDITING - 211114 - 152450Mirajii OlomiiОценок пока нет

- Issai 100 20210906114606Документ37 страницIssai 100 20210906114606Eddy ETMОценок пока нет

- Module #02 - Audits of Historical Financial InformationДокумент3 страницыModule #02 - Audits of Historical Financial InformationRhesus UrbanoОценок пока нет

- Audit in Nursing Management and AdministrationДокумент31 страницаAudit in Nursing Management and Administrationbemina jaОценок пока нет

- AUD Internal ControlДокумент11 страницAUD Internal ControlChrismand CongeОценок пока нет

- At 02Документ5 страницAt 02Mitch PacienteОценок пока нет

- Audit Chapter 1111 PDFFFFДокумент25 страницAudit Chapter 1111 PDFFFFAlex HaymeОценок пока нет

- Chapter 1 Auditing I - 2012Документ4 страницыChapter 1 Auditing I - 2012Tilahun MikiasОценок пока нет

- AAP - Assignment 3Документ5 страницAAP - Assignment 3Cyra EllaineОценок пока нет

- AuditДокумент19 страницAuditRuzel DayluboОценок пока нет

- PSBA - Introduction To Assurance and Related ServicesДокумент6 страницPSBA - Introduction To Assurance and Related ServicesephraimОценок пока нет

- Acctg. Major 6 - Auditing and Internal ControlДокумент12 страницAcctg. Major 6 - Auditing and Internal ControlTrayle HeartОценок пока нет

- MODULE 1 2 ExercisesДокумент8 страницMODULE 1 2 ExercisesAMОценок пока нет

- Summer Internship RepoertДокумент24 страницыSummer Internship RepoertNarvada Shankar SinghОценок пока нет

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОт EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОценок пока нет

- Visperas, Chelsea May MДокумент2 страницыVisperas, Chelsea May MChelsea VisperasОценок пока нет

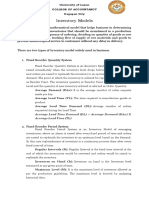

- Inventory Models: Provide Uninterrupted Service To Customers Without Any Delay in DeliveryДокумент5 страницInventory Models: Provide Uninterrupted Service To Customers Without Any Delay in DeliveryChelsea VisperasОценок пока нет

- Re: Thesis PDFДокумент1 страницаRe: Thesis PDFChelsea VisperasОценок пока нет

- Agency and BranchДокумент25 страницAgency and BranchChelsea VisperasОценок пока нет

- Movie (Catch Me If You Can) PDFДокумент5 страницMovie (Catch Me If You Can) PDFChelsea VisperasОценок пока нет

- 3463afdcb438dc833d95f8d1814e4b36_8f5c0d43171d85063d48300fbb6274faДокумент4 страницы3463afdcb438dc833d95f8d1814e4b36_8f5c0d43171d85063d48300fbb6274faChelsea VisperasОценок пока нет

- ResaДокумент7 страницResaChelsea VisperasОценок пока нет

- Afar 8501-8504Документ14 страницAfar 8501-8504Chelsea VisperasОценок пока нет

- Afar 8505Документ4 страницыAfar 8505Chelsea VisperasОценок пока нет

- Dissertation On HR AuditДокумент6 страницDissertation On HR AuditBuyAPhilosophyPaperUK100% (1)

- Auditing Theory: CPA ReviewДокумент12 страницAuditing Theory: CPA ReviewThan TanОценок пока нет

- Talbot SlidesCarnivalДокумент38 страницTalbot SlidesCarnivalLester Glenn LimheyaОценок пока нет

- Ias Ac-98 Accreditation Criteria For Inspection AgenciesДокумент4 страницыIas Ac-98 Accreditation Criteria For Inspection AgenciesMario RodriguezОценок пока нет

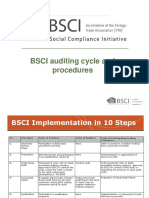

- Bsci Auditing Cycle PDFДокумент7 страницBsci Auditing Cycle PDFShiv Raj Mathur100% (1)

- CAMS QuestionsДокумент3 страницыCAMS QuestionsanwarОценок пока нет

- Nature of AuditingДокумент37 страницNature of Auditinganon_672065362Оценок пока нет

- IFMIS - The Indian ExperienceДокумент44 страницыIFMIS - The Indian ExperiencesukeshsanghiОценок пока нет

- CH 5Документ2 страницыCH 5Scholastica DaniaОценок пока нет

- Internal Control Over Financial Reporting (Chapter 3)Документ82 страницыInternal Control Over Financial Reporting (Chapter 3)PeterSarmientoОценок пока нет

- Guidance Energy Management Base On Menteri ESDM No14 Tahun 2012Документ12 страницGuidance Energy Management Base On Menteri ESDM No14 Tahun 2012Isyalendra Surya AlamОценок пока нет

- CHAPTER 22-Audit Evidence EvaluationДокумент27 страницCHAPTER 22-Audit Evidence EvaluationIryne Kim PalatanОценок пока нет

- Arens Auditing16e SM 10Документ30 страницArens Auditing16e SM 10김현중100% (1)

- 2016 4 The Khyber Pakhtunkhwa Antiquities Act 2016Документ38 страниц2016 4 The Khyber Pakhtunkhwa Antiquities Act 2016Tehmash KhanОценок пока нет

- Assertions in The Audit of Financial StatementsДокумент3 страницыAssertions in The Audit of Financial StatementsBirei GonzalesОценок пока нет

- Desktop SolutionДокумент7 страницDesktop SolutionAmira Nur Afiqah Agus SalimОценок пока нет

- Vendor Risk ManagementДокумент12 страницVendor Risk Managementrajat_rath100% (1)

- Chapter 03 QuestionsДокумент32 страницыChapter 03 QuestionsPhương NguyễnОценок пока нет

- How To Audit Fmeas Using Quality ObjectivesДокумент41 страницаHow To Audit Fmeas Using Quality ObjectivesAmir KhakzadОценок пока нет

- Bongaigaon - 488Документ513 страницBongaigaon - 488Ramesh BabuОценок пока нет

- Audit Planning and MaterialityДокумент11 страницAudit Planning and MaterialityTigRao UlyMelОценок пока нет

- Acctg 17nd-Final Exam AДокумент14 страницAcctg 17nd-Final Exam AKristinelle AragoОценок пока нет

- External Auditors' Reliance On Internal Audit in Sri LankaДокумент83 страницыExternal Auditors' Reliance On Internal Audit in Sri Lankadilu_0002100% (2)

- Audit and Assurance Concept and Application Chapter 1Документ12 страницAudit and Assurance Concept and Application Chapter 1Ceejay FrillarteОценок пока нет

- Internal Audit TrainingДокумент43 страницыInternal Audit TrainingwildanОценок пока нет

- CV of PawanДокумент2 страницыCV of Pawanpawandubey1986Оценок пока нет