Вам также может понравиться

- Chapter 9 - Accounting For ReceivablesДокумент10 страницChapter 9 - Accounting For ReceivablesMajan Kaur100% (1)

- Megan Jenkins Gemini StatementДокумент2 страницыMegan Jenkins Gemini StatementJonathan Seagull LivingstonОценок пока нет

- Financial Accounting - Want to Become Financial Accountant in 30 Days?От EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Рейтинг: 5 из 5 звезд5/5 (1)

- ACC101 Chapter7new PDFДокумент23 страницыACC101 Chapter7new PDFJana Kryzl DibdibОценок пока нет

- Accounting For ReceivablesДокумент23 страницыAccounting For ReceivablesFelekePhiliphosОценок пока нет

- Kashato Shirts Practice SetFS 1Документ100 страницKashato Shirts Practice SetFS 1Raven Ann DimapilisОценок пока нет

- Three Column Cash BookДокумент5 страницThree Column Cash Bookvinodksrini007100% (2)

- Chapter 8Документ37 страницChapter 8Léo Audibert100% (2)

- Logistics ReadingДокумент147 страницLogistics ReadingAdityaОценок пока нет

- Quiz - Dissolution and Liquidation (Answers)Документ8 страницQuiz - Dissolution and Liquidation (Answers)peter pakerОценок пока нет

- ReceivablesДокумент5 страницReceivablesHanns Lexter PadillaОценок пока нет

- Chap010.ppt Supply Chain Management 000Документ27 страницChap010.ppt Supply Chain Management 000Saad Khadur EilyesОценок пока нет

- (PDF) Latihan Soal Sap Finance Lengkap Ada JawabanДокумент6 страниц(PDF) Latihan Soal Sap Finance Lengkap Ada JawabanRoftadiaWgОценок пока нет

- PR 4-5BДокумент15 страницPR 4-5BNoveliaОценок пока нет

- Lec7 - Account ReceivablesДокумент33 страницыLec7 - Account ReceivablesDylan Rabin PereiraОценок пока нет

- This Study Resource Was: Philippine School of Business AdministrationДокумент6 страницThis Study Resource Was: Philippine School of Business AdministrationNah HamzaОценок пока нет

- Accounting For ReceivablesДокумент49 страницAccounting For Receivablesdwi studyОценок пока нет

- Accounts Receivable: Financial AccountingДокумент27 страницAccounts Receivable: Financial AccountingHassan AliОценок пока нет

- Accounting For Receivables: Weygandt - Kieso - KimmelДокумент49 страницAccounting For Receivables: Weygandt - Kieso - KimmelHaftom YitbarekОценок пока нет

- Lec 8 - First HalfДокумент24 страницыLec 8 - First HalfNidus PhrykeОценок пока нет

- Financial Accounting, 4eДокумент47 страницFinancial Accounting, 4eEka Aliyah FauziОценок пока нет

- Accounting Principle II Chapter3Документ7 страницAccounting Principle II Chapter3aarka soomalidaОценок пока нет

- Cash To Inventory Reviewer 1Документ15 страницCash To Inventory Reviewer 1Patricia Camille AustriaОценок пока нет

- Accounting For ReceivablesДокумент37 страницAccounting For ReceivablesHaftom YitbarekОценок пока нет

- Accounting For Receivables PDFДокумент23 страницыAccounting For Receivables PDFjess calderonОценок пока нет

- Accounting For Receivables 1Документ48 страницAccounting For Receivables 1ramadhan wiprayogaОценок пока нет

- Estimation of Doubtful AccountsДокумент3 страницыEstimation of Doubtful AccountsClar AgramonОценок пока нет

- Account Recivable Bet Teacher NoteДокумент39 страницAccount Recivable Bet Teacher NoteHaftom YitbarekОценок пока нет

- Warren SM Ch.09 FinalДокумент23 страницыWarren SM Ch.09 FinalAA BB MMОценок пока нет

- Revenue Recognition and Receivables: Financial Accounting - Lecture 5Документ30 страницRevenue Recognition and Receivables: Financial Accounting - Lecture 5Peter ShangОценок пока нет

- Accounts Receivable Inventory Management - .DocmДокумент11 страницAccounts Receivable Inventory Management - .DocmellishОценок пока нет

- Module 3 - Accounts Receivable Part II - 111702467Документ11 страницModule 3 - Accounts Receivable Part II - 111702467shimizuyumi53Оценок пока нет

- Part B: Computerised AccountingДокумент6 страницPart B: Computerised AccountingSonakshi JainОценок пока нет

- Notes 08Документ11 страницNotes 08FantayОценок пока нет

- StudyGuideChap08 PDFДокумент27 страницStudyGuideChap08 PDFNarjes DehkordiОценок пока нет

- CH09Документ28 страницCH09Will TrầnОценок пока нет

- Chapter 07 - Accounts and Notes Receivable. Chapter OutlineДокумент6 страницChapter 07 - Accounts and Notes Receivable. Chapter OutlinesatyaОценок пока нет

- Financial Accounting Module 2 SummaryДокумент2 страницыFinancial Accounting Module 2 Summarymohita.gupta4Оценок пока нет

- Chapter 7Документ39 страницChapter 7juls100% (1)

- Adjustment Entries II - Accounting-Workbook - Zaheer-SwatiДокумент6 страницAdjustment Entries II - Accounting-Workbook - Zaheer-SwatiZaheer SwatiОценок пока нет

- Debit and Credit: Fundamentals of Accountancy, Business and Management 1Документ10 страницDebit and Credit: Fundamentals of Accountancy, Business and Management 1triicciaa faith100% (1)

- CHAP 7 - LECTURER'S NOTES (1) (AutoRecovered)Документ11 страницCHAP 7 - LECTURER'S NOTES (1) (AutoRecovered)ManzMalayaОценок пока нет

- Unit 9Документ5 страницUnit 9Anonymous Fn7Ko5riKTОценок пока нет

- Account Receivable ClassДокумент30 страницAccount Receivable ClassBeast aОценок пока нет

- Account Receivable ClassДокумент30 страницAccount Receivable ClassBeast aОценок пока нет

- Accounts Receivable and Estimating Doubtful AccountsДокумент7 страницAccounts Receivable and Estimating Doubtful AccountsMiles SantosОценок пока нет

- Zeus MillanДокумент7 страницZeus MillanannyeongОценок пока нет

- Cengage Learning Accounting 27th Edition-Copy RemovedДокумент4 страницыCengage Learning Accounting 27th Edition-Copy Removedkaya waffles12Оценок пока нет

- Account Receivables Cheat Sheet NoviДокумент1 страницаAccount Receivables Cheat Sheet Novisiddesh pachkawadeОценок пока нет

- Trial Balance and Rectification of Errors: Accountancy 180Документ46 страницTrial Balance and Rectification of Errors: Accountancy 180kofirОценок пока нет

- POA Topic 12Документ3 страницыPOA Topic 12Ian ChanОценок пока нет

- Chapter 4 Accounts Receivable Learning Objectives: Receivables."Документ4 страницыChapter 4 Accounts Receivable Learning Objectives: Receivables."Misiah Paradillo JangaoОценок пока нет

- Accounting Lecture V HandoutsДокумент34 страницыAccounting Lecture V HandoutsКамилла МолдалиеваОценок пока нет

- ch09 ACCOUNTING FOR RECEIVABLESДокумент47 страницch09 ACCOUNTING FOR RECEIVABLESJemal SeidОценок пока нет

- Accounts Receivable ManagementДокумент21 страницаAccounts Receivable ManagementNeris SaturdayОценок пока нет

- 8.7.1 Allowance MethodДокумент5 страниц8.7.1 Allowance MethodAkkamaОценок пока нет

- Acc. ReceivableДокумент11 страницAcc. ReceivableUswatun HsnОценок пока нет

- Stern CorporationsДокумент30 страницStern CorporationsShubham MallikОценок пока нет

- Acc CH 4Документ15 страницAcc CH 4Bicaaqaa M. AbdiisaaОценок пока нет

- Chapter 8 Feb.5Документ51 страницаChapter 8 Feb.5AaaОценок пока нет

- CH.8 Notes - Accounting For ReceivablesДокумент19 страницCH.8 Notes - Accounting For ReceivablesLEEN hashemОценок пока нет

- Acc CH 4Документ16 страницAcc CH 4Tajudin Abba RagooОценок пока нет

- Afda G2 ReceivablesДокумент9 страницAfda G2 ReceivablesSharina DevarasОценок пока нет

- Lect 5 ReceivablesДокумент40 страницLect 5 Receivablesjoeltan111Оценок пока нет

- Welcomeback: Workshop SixДокумент55 страницWelcomeback: Workshop SixLeah StonesОценок пока нет

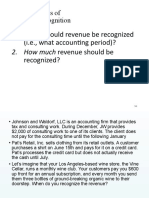

- When Should Revenue Be Recognized 2. How Much Revenue Should BeДокумент25 страницWhen Should Revenue Be Recognized 2. How Much Revenue Should BeKen AdamsОценок пока нет

- Financial and Management Accounting: BITS PilaniДокумент29 страницFinancial and Management Accounting: BITS PilaniSajid RehmanОценок пока нет

- Chapter 6 - Reporting Revenues, Receivables and Cash - StudentДокумент29 страницChapter 6 - Reporting Revenues, Receivables and Cash - StudentTimmy QuinnОценок пока нет

- Tran Hoai Anh Bai Tap Chap 4Документ16 страницTran Hoai Anh Bai Tap Chap 4Vũ Nhi AnОценок пока нет

- Bracey Company Manufactures and Sells One ProductДокумент2 страницыBracey Company Manufactures and Sells One ProductKailash KumarОценок пока нет

- Adjusting EntriesДокумент3 страницыAdjusting Entriesnreid2701Оценок пока нет

- Lesson 08a - Financial Statements From TB - 2023Документ66 страницLesson 08a - Financial Statements From TB - 2023IGTDRipZОценок пока нет

- A Crane Video Company Bank Reconciliation Statement DescriptionДокумент6 страницA Crane Video Company Bank Reconciliation Statement Descriptionsazkia fatmandaОценок пока нет

- LES MEILLEURS TRANSITAIRES ALIBABA - Chine Vers Les Pays de LAfrique Et Dautres Pays Du MondeДокумент22 страницыLES MEILLEURS TRANSITAIRES ALIBABA - Chine Vers Les Pays de LAfrique Et Dautres Pays Du Mondemabou5887Оценок пока нет

- SAP MRP What Is SAP MRP - Material Requirement PlanningДокумент2 страницыSAP MRP What Is SAP MRP - Material Requirement Planningswayam100% (1)

- Soal Latihan Sia 20192020 Dagang-JasaДокумент3 страницыSoal Latihan Sia 20192020 Dagang-JasaJhoni LimОценок пока нет

- Plantilla de Estructuras Organizacionales - HubSpotДокумент8 страницPlantilla de Estructuras Organizacionales - HubSpotAsesor 3GОценок пока нет

- PRR 10748 WM Franchise Fee July 16 2007 To July 15 2015 PDFДокумент98 страницPRR 10748 WM Franchise Fee July 16 2007 To July 15 2015 PDFRecordTrac - City of OaklandОценок пока нет

- Account Statement: Penyata AkaunДокумент8 страницAccount Statement: Penyata Akaunsgconstruction94Оценок пока нет

- Managerial MidtermДокумент6 страницManagerial MidtermIqtidar KhanОценок пока нет

- CHAPTER 6 - Accrual and PrepaymentskdДокумент15 страницCHAPTER 6 - Accrual and PrepaymentskdAinaОценок пока нет

- Director Global Supply Chain in USA Resume Amol BiniwaleДокумент2 страницыDirector Global Supply Chain in USA Resume Amol BiniwaleAmolBiniwaleОценок пока нет

- Account StatementДокумент12 страницAccount StatementRiteshОценок пока нет

- Chapter 2 SolutionsДокумент22 страницыChapter 2 SolutionsNLSatyanarayanaОценок пока нет

- Treasury Rules TR STRДокумент407 страницTreasury Rules TR STREngr Rameez PatoliОценок пока нет

- Ledger Accounting and Double Entry Bookkeeping: Chapter Learning ObjectivesДокумент46 страницLedger Accounting and Double Entry Bookkeeping: Chapter Learning Objectiveskoti kebele100% (1)

- Financial Accounting, 5e: Weygandt, Kieso, & KimmelДокумент31 страницаFinancial Accounting, 5e: Weygandt, Kieso, & KimmelAuora BiancaОценок пока нет

- Manufacturing Buyer Planner in Lancaster PA Resume Melissa SmithДокумент2 страницыManufacturing Buyer Planner in Lancaster PA Resume Melissa SmithMelissaSmith1Оценок пока нет

- Ibiz 009801005561307 20230901 20230916 1694856792864478677.Документ7 страницIbiz 009801005561307 20230901 20230916 1694856792864478677.yunitahikmah59Оценок пока нет