Вам также может понравиться

- Case StudyДокумент4 страницыCase StudyTabish Iftikhar Syed100% (1)

- Accountant ResumeДокумент1 страницаAccountant ResumeSahiba SheikhОценок пока нет

- The Steel War - Mittal Vs ArcelorДокумент25 страницThe Steel War - Mittal Vs ArcelorAsiri PrasadОценок пока нет

- Short-Term Sources For Financing Current Assets: S A R Q P I. QuestionsДокумент12 страницShort-Term Sources For Financing Current Assets: S A R Q P I. QuestionsAngel CoОценок пока нет

- Equity Valuation: Models from Leading Investment BanksОт EverandEquity Valuation: Models from Leading Investment BanksJan ViebigОценок пока нет

- ACCA P2INT Notes J15 PDFДокумент256 страницACCA P2INT Notes J15 PDFopentuitionID100% (1)

- Company Analysis (IHH Healthcare Berhad)Документ78 страницCompany Analysis (IHH Healthcare Berhad)Nurulain100% (4)

- 4.EF232.FIM (IL-II) Solution CMA 2023 January ExamДокумент6 страниц4.EF232.FIM (IL-II) Solution CMA 2023 January ExamnobiОценок пока нет

- CS-Professional Paper-3 Financial, Treasury and Forex Management (Dec - 2010)Документ11 страницCS-Professional Paper-3 Financial, Treasury and Forex Management (Dec - 2010)manjinderjodhka8903Оценок пока нет

- 3.EF232. FIM IL II Solution CMA September 2022 Exam.Документ5 страниц3.EF232. FIM IL II Solution CMA September 2022 Exam.nobiОценок пока нет

- Corporate Finance - SS 11, Reading 35 - Capital BudgetingДокумент45 страницCorporate Finance - SS 11, Reading 35 - Capital Budgetingud100% (1)

- Chapter Four Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationДокумент23 страницыChapter Four Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationTung HarryОценок пока нет

- Capital Structure Lecture 9Документ45 страницCapital Structure Lecture 9koketsoОценок пока нет

- Tutorial 3 QuestionsДокумент6 страницTutorial 3 QuestionshrfjbjrfrfОценок пока нет

- Bora Assignment FinalДокумент12 страницBora Assignment FinalBora AslanОценок пока нет

- Ueht3 2021 - Finc3015 - Trần Hữu Phước - 20448989.Документ8 страницUeht3 2021 - Finc3015 - Trần Hữu Phước - 20448989.phuoc.tran23006297Оценок пока нет

- Main Exam 2015Документ7 страницMain Exam 2015Diego AguirreОценок пока нет

- FIN 440: Individual Assignment Total: 50Документ12 страницFIN 440: Individual Assignment Total: 50ImrAn KhAnОценок пока нет

- CORPORATE FINANCE Final Exam June 2022Документ11 страницCORPORATE FINANCE Final Exam June 2022Fungai MajuriraОценок пока нет

- ACC314 Business Finance Management Resit Answers (SEPT) R 19-20Документ8 страницACC314 Business Finance Management Resit Answers (SEPT) R 19-20Rukshani RefaiОценок пока нет

- Cost of Capital (Problem)Документ4 страницыCost of Capital (Problem)Rio RegalaОценок пока нет

- Mock 2 - Afternoon - AnswersДокумент27 страницMock 2 - Afternoon - Answerspagis31861Оценок пока нет

- Chapter 5: Cost of Capital Dec 2014Документ7 страницChapter 5: Cost of Capital Dec 2014swarna dasОценок пока нет

- Short-Term Sources For Financing Current AssetsДокумент11 страницShort-Term Sources For Financing Current AssetsAlexandra TagleОценок пока нет

- Capital BudgetingДокумент21 страницаCapital BudgetingGabriella RaphaelОценок пока нет

- Corporate Finance LOS 36Документ26 страницCorporate Finance LOS 36RamОценок пока нет

- Section A: Gross ProfitДокумент8 страницSection A: Gross ProfitkangОценок пока нет

- ACFA-TCF-Workshop-2-Answers (Read-Only) PDFДокумент21 страницаACFA-TCF-Workshop-2-Answers (Read-Only) PDFnummoОценок пока нет

- Acquisition & Mergers ValuationДокумент18 страницAcquisition & Mergers ValuationAqeel HanjraОценок пока нет

- Capital Budgeting HandoutsДокумент13 страницCapital Budgeting HandoutsCoke Aidenry SaludoОценок пока нет

- Fm-May-June 2015Документ18 страницFm-May-June 2015banglauserОценок пока нет

- Jun 2003 SolutionsДокумент10 страницJun 2003 SolutionsJosh LebetkinОценок пока нет

- ADL 13 Ver2+Документ9 страницADL 13 Ver2+DistPub eLearning Solution100% (1)

- FM Unit 8 Lecture Notes - Capital BudgetingДокумент4 страницыFM Unit 8 Lecture Notes - Capital BudgetingDebbie DebzОценок пока нет

- ICAI - Question BankДокумент6 страницICAI - Question Bankkunal mittalОценок пока нет

- f9 2018 Marjun QДокумент6 страницf9 2018 Marjun QDilawar HayatОценок пока нет

- Revision For The Final Exam (With Results) : Instructor: Course: SemesterДокумент12 страницRevision For The Final Exam (With Results) : Instructor: Course: SemesterashibhallauОценок пока нет

- Managerial FinanceДокумент23 страницыManagerial Financenourkhaled1218Оценок пока нет

- Suggested Answers To Even-Numbered Problems: Analysis For Financial Management, 10eДокумент2 страницыSuggested Answers To Even-Numbered Problems: Analysis For Financial Management, 10eDr-Émpòrìó MàróОценок пока нет

- Sesion 11 Chapter 10 Dan 11Документ60 страницSesion 11 Chapter 10 Dan 11Gilang Akbar RizkyanОценок пока нет

- SEx 4Документ24 страницыSEx 4Amir Madani100% (3)

- Bfi 4301 Financial Management Paper 1Документ10 страницBfi 4301 Financial Management Paper 1Paul AtariОценок пока нет

- Chapter 20 - AnswerДокумент11 страницChapter 20 - AnswerLove FreddyОценок пока нет

- Chapter 5Документ41 страницаChapter 5Project MgtОценок пока нет

- Mock Exam 2023 #2 Second Session Corporate Finance, Equity, FixedДокумент90 страницMock Exam 2023 #2 Second Session Corporate Finance, Equity, Fixedvedant.diwan26Оценок пока нет

- Dani IFM AssignmentДокумент9 страницDani IFM AssignmentdanielОценок пока нет

- Unit 12Документ13 страницUnit 12Mîñåk ŞhïïОценок пока нет

- Directorate of Distance Education and Open Learning (Ddeol)Документ9 страницDirectorate of Distance Education and Open Learning (Ddeol)Mabvuto PhiriОценок пока нет

- CityU - CF 01 SolutionДокумент4 страницыCityU - CF 01 SolutionKhanh LinhОценок пока нет

- FE (201312) Paper II - Answer PDFДокумент12 страницFE (201312) Paper II - Answer PDFgaryОценок пока нет

- Bodie10ce SM CH19Документ12 страницBodie10ce SM CH19beadand1Оценок пока нет

- 4 The Firm's Capital Structure and Degree of LeverageДокумент9 страниц4 The Firm's Capital Structure and Degree of LeverageMariel GarraОценок пока нет

- Sample Questions For Finance PaperДокумент4 страницыSample Questions For Finance PaperRahul AtodariaОценок пока нет

- Acca Paper F9 Financial Management June 2015 Revision Mock 2 - Marking SchemeДокумент14 страницAcca Paper F9 Financial Management June 2015 Revision Mock 2 - Marking SchemeSidra QamarОценок пока нет

- CH 5Документ15 страницCH 5Gizaw BelayОценок пока нет

- Sample Exam December 2019Документ10 страницSample Exam December 2019miguelОценок пока нет

- Financial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Документ12 страницFinancial Reporting II ACC 402/602, Section 1001-1002 Practice Exam 1Joel Christian MascariñaОценок пока нет

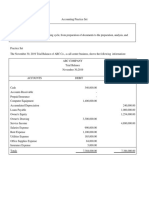

- Practice SetДокумент10 страницPractice Setkaeya alberichОценок пока нет

- NCR Cup 2 Judges' Copy - Elimination RoundДокумент17 страницNCR Cup 2 Judges' Copy - Elimination RoundMich ClementeОценок пока нет

- Bangladesh University of Professionals: Faculty of Business StudiesДокумент3 страницыBangladesh University of Professionals: Faculty of Business StudiesRahman NiloyОценок пока нет

- Financial Accounting 7th Edition Libby Solutions ManualДокумент48 страницFinancial Accounting 7th Edition Libby Solutions ManualBrandonCoopergnzxy100% (14)

- AcscacДокумент12 страницAcscacJohn Brian D. SorianoОценок пока нет

- Chapter 20 AnswerДокумент11 страницChapter 20 AnswerjennyОценок пока нет

- Chemical - Covering LetterДокумент1 страницаChemical - Covering LetterRashid JalalОценок пока нет

- Registration - No Name Total Assessment Marks Assessment Questions Total Question Marks Mapping ClosДокумент2 страницыRegistration - No Name Total Assessment Marks Assessment Questions Total Question Marks Mapping ClosRashid JalalОценок пока нет

- Laser Jet Pro PrinterДокумент1 страницаLaser Jet Pro PrinterRashid JalalОценок пока нет

- Section Course OutlineДокумент1 страницаSection Course OutlineRashid JalalОценок пока нет

- References FileДокумент3 страницыReferences FileRashid JalalОценок пока нет

- Time Table-ME-1st Semester (Session 2017)Документ1 страницаTime Table-ME-1st Semester (Session 2017)Rashid JalalОценок пока нет

- Time Table v-1.0 UpdatedДокумент10 страницTime Table v-1.0 UpdatedRashid JalalОценок пока нет

- Time Table-ME-3rd Semester (Session 2016)Документ1 страницаTime Table-ME-3rd Semester (Session 2016)Rashid JalalОценок пока нет

- Time Table-ME-1st Semester (Session 2017)Документ1 страницаTime Table-ME-1st Semester (Session 2017)Rashid JalalОценок пока нет

- Performa For Teacher's Preference of Courses For SPRING 2018 SemesterДокумент3 страницыPerforma For Teacher's Preference of Courses For SPRING 2018 SemesterRashid JalalОценок пока нет

- Time Table v-1.2 UpdatedДокумент10 страницTime Table v-1.2 UpdatedRashid JalalОценок пока нет

- Time Table-ME-5th Semester (Session 2015)Документ1 страницаTime Table-ME-5th Semester (Session 2015)Rashid JalalОценок пока нет

- Physics 1st YearДокумент2 страницыPhysics 1st YearRashid Jalal100% (1)

- Test Physics Ch#13 Test SeesДокумент2 страницыTest Physics Ch#13 Test SeesRashid JalalОценок пока нет

- Time Table-ME-7th Semester (Session 2014)Документ1 страницаTime Table-ME-7th Semester (Session 2014)Rashid JalalОценок пока нет

- Time Table-ME-3rd Semester (Session 2016)Документ1 страницаTime Table-ME-3rd Semester (Session 2016)Rashid JalalОценок пока нет

- As It Happened", The Guardian Business News, 11SEP17Документ2 страницыAs It Happened", The Guardian Business News, 11SEP17Rashid JalalОценок пока нет

- Test Ch#3 1st YearДокумент3 страницыTest Ch#3 1st YearRashid Jalal100% (1)

- Test Physics Ch#1+2 1st YearДокумент2 страницыTest Physics Ch#1+2 1st YearRashid JalalОценок пока нет

- Physics 2nd Year TestДокумент3 страницыPhysics 2nd Year TestRashid JalalОценок пока нет

- 1st Year Test PHYДокумент2 страницы1st Year Test PHYRashid Jalal100% (2)

- 1st Year Test PHYДокумент2 страницы1st Year Test PHYRashid JalalОценок пока нет

- Physics 1st YearДокумент2 страницыPhysics 1st YearRashid JalalОценок пока нет

- Chemistry 1st Year TestДокумент3 страницыChemistry 1st Year TestRashid JalalОценок пока нет

- Physics 1st YearДокумент2 страницыPhysics 1st YearRashid JalalОценок пока нет

- Physics 1st YearДокумент2 страницыPhysics 1st YearRashid Jalal100% (1)

- Physics 1st YearДокумент2 страницыPhysics 1st YearRashid JalalОценок пока нет

- Physics 1st Year TestДокумент3 страницыPhysics 1st Year TestRashid JalalОценок пока нет

- India DailyДокумент72 страницыIndia DailyKhush GosraniОценок пока нет

- Auditing Problems RetypedДокумент4 страницыAuditing Problems RetypedJozelle Grace PadelОценок пока нет

- 2 Income and Business Taxation MidtermДокумент116 страниц2 Income and Business Taxation MidtermPamela PerezОценок пока нет

- Financial Supplement: January - MarchДокумент9 страницFinancial Supplement: January - MarchSanjeev ThadaniОценок пока нет

- Outline: IFMP AML/CFT Certification: o o o o oДокумент6 страницOutline: IFMP AML/CFT Certification: o o o o oRaza FОценок пока нет

- Module 6 Chapter 8 Output VAT Zero Rated SalesДокумент5 страницModule 6 Chapter 8 Output VAT Zero Rated SalesChris SumandeОценок пока нет

- Trial Balance To FSДокумент9 страницTrial Balance To FSYếnОценок пока нет

- Dividend Policy in Multinationals and Transfer PricingДокумент11 страницDividend Policy in Multinationals and Transfer PricingKaren Diane Chua RiveraОценок пока нет

- Financial Management 2 Assignment 1: Dividend Policy at FPL GroupДокумент9 страницFinancial Management 2 Assignment 1: Dividend Policy at FPL GroupDiv_nОценок пока нет

- Objective Questions and Answers of Financial ManagementДокумент22 страницыObjective Questions and Answers of Financial ManagementGhulam MustafaОценок пока нет

- Beximco Pharmaceuticals Limited Statement of Financial PositionДокумент55 страницBeximco Pharmaceuticals Limited Statement of Financial Positionrimon dasОценок пока нет

- Dandot 2008 AnnualДокумент39 страницDandot 2008 AnnualMuhammad haseebОценок пока нет

- ABC CompanyДокумент11 страницABC CompanyA DiolataОценок пока нет

- Operating Liquidity: Accounts Receivable Inventory Accounts PayableДокумент4 страницыOperating Liquidity: Accounts Receivable Inventory Accounts PayableAman Kumar SharmaОценок пока нет

- Unit 8: InvestmentsДокумент17 страницUnit 8: InvestmentsShaqeeb Ahamed 11AОценок пока нет

- Assignment#2Документ3 страницыAssignment#2Wuhao KoОценок пока нет

- Anti Takeover 1 ESSAY 1Документ13 страницAnti Takeover 1 ESSAY 1Amrita Dhasmana100% (1)

- Faculty of Law: Jamia Millia IslamiaДокумент21 страницаFaculty of Law: Jamia Millia IslamiaFaisal HassanОценок пока нет

- Talbots Harvard Case AnsДокумент4 страницыTalbots Harvard Case AnsChristel Yeo0% (1)

- Unit IДокумент10 страницUnit IsoundarpandiyanОценок пока нет

- Defenses Against Hostile TakeoverДокумент51 страницаDefenses Against Hostile TakeoverHemanshu RoyОценок пока нет

- Ifrs at A Glance IFRS 2 Share-Based PaymentДокумент5 страницIfrs at A Glance IFRS 2 Share-Based PaymentNoor Ul Hussain MirzaОценок пока нет

- Teachings Note California Pizza Kitchen - Term PaperДокумент8 страницTeachings Note California Pizza Kitchen - Term PaperDharm Veer RathoreОценок пока нет

- Trial BalanceДокумент14 страницTrial Balanceswetha_makulaОценок пока нет

- II PA Fianancial Management Ques - BankДокумент11 страницII PA Fianancial Management Ques - BankSARAVANAVEL VELОценок пока нет

- Risk and Return Formula SheetДокумент7 страницRisk and Return Formula SheetMaha Bianca Charisma CastroОценок пока нет