Вам также может понравиться

- Home Depot - GROUP 2Документ10 страницHome Depot - GROUP 2Karthik KotaОценок пока нет

- DPMC-12a, Unit Schedule BreakdownДокумент4 страницыDPMC-12a, Unit Schedule BreakdownFranc GrošeljОценок пока нет

- AAT Chapter ActivitiesДокумент13 страницAAT Chapter ActivitiesabushohagОценок пока нет

- Short Notes CostingДокумент32 страницыShort Notes CostingViswanathan Srk100% (1)

- Chemalite BДокумент12 страницChemalite BTatsat Pandey100% (2)

- Manac Asn4 HydrochemДокумент6 страницManac Asn4 HydrochemNikhil JindalОценок пока нет

- Case Study 4 3 Copies ExpressДокумент7 страницCase Study 4 3 Copies Expressamitsemt100% (2)

- Chemalite Inc. Case Study SolutionДокумент8 страницChemalite Inc. Case Study SolutionSaswata BanerjeeОценок пока нет

- Chemalite Sol Final 011112Документ9 страницChemalite Sol Final 011112pankyagr75% (4)

- Case Report - Grenell FarmДокумент5 страницCase Report - Grenell Farmajsibal100% (1)

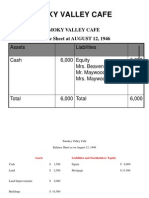

- Smoky Valley CafeДокумент3 страницыSmoky Valley Cafemohit_namanОценок пока нет

- Dispensers of CaliforniaДокумент4 страницыDispensers of CaliforniaShweta GautamОценок пока нет

- Chemalite PDFДокумент2 страницыChemalite PDFShashank Yadav100% (2)

- Case Forest City Tennis ClubДокумент9 страницCase Forest City Tennis ClubAhmedNiaz100% (1)

- Variable (Direct) CostingДокумент3 страницыVariable (Direct) CostingMela carlonОценок пока нет

- Lewis Corporation Assignment Case 6-2 KTMДокумент7 страницLewis Corporation Assignment Case 6-2 KTMSudeep ShahОценок пока нет

- Chemalite SolutionHBSДокумент10 страницChemalite SolutionHBSManoj Singh0% (1)

- Chema LiteДокумент8 страницChema LiteHàMềmОценок пока нет

- PM Study Notes MayДокумент234 страницыPM Study Notes May77 Raj Bhanushali100% (1)

- Case Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkДокумент7 страницCase Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkAdarsh Nayan100% (1)

- The Garden Spot 1Документ25 страницThe Garden Spot 1Saad Arain0% (1)

- Chemalite IncДокумент2 страницыChemalite IncRaju Milan100% (2)

- Chemalite, Inc. (B) Case BackgroundДокумент2 страницыChemalite, Inc. (B) Case BackgroundAnuragОценок пока нет

- Case Analysis - Rosemont Hill Health Center - V3Документ8 страницCase Analysis - Rosemont Hill Health Center - V3thearpan100% (2)

- Planter Nut Case Analysis PDF FreeДокумент2 страницыPlanter Nut Case Analysis PDF Freesidra imtiaz50% (2)

- Case Study MOPДокумент6 страницCase Study MOPLorenc BogovikuОценок пока нет

- Income Statements 2010Документ10 страницIncome Statements 2010Shivam GoelОценок пока нет

- Maria Hernandez & AssociatesДокумент2 страницыMaria Hernandez & AssociatesManish Kumar33% (3)

- Module 12 - Relevant Costing and Short-Term Decision MakingДокумент8 страницModule 12 - Relevant Costing and Short-Term Decision MakingAndrea ValdezОценок пока нет

- Software Associates Case AnalysisДокумент8 страницSoftware Associates Case AnalysisMuhammad AsifОценок пока нет

- Lori Crump Accounting Case StudyДокумент1 страницаLori Crump Accounting Case StudyHarsh Anchalia100% (1)

- Chemilite Case StudyДокумент12 страницChemilite Case StudyRavi Pratap Singh Tomar100% (3)

- Chemalite Case Analysis Indirect MethodДокумент1 страницаChemalite Case Analysis Indirect MethodSujit Prapti33% (3)

- Lone Pine Cafe SolutionДокумент5 страницLone Pine Cafe SolutionRitu ChhipaОценок пока нет

- Thumbs-Up Inc.Документ4 страницыThumbs-Up Inc.Rakshit Chandra Shekhar JoshiОценок пока нет

- Case Analysis Rosemont Hill Health Center V3 PDFДокумент8 страницCase Analysis Rosemont Hill Health Center V3 PDFPoorvi SinghalОценок пока нет

- 7-2 John Holtz (C) Case Study SolutionsДокумент14 страниц7-2 John Holtz (C) Case Study SolutionsAashima Grover100% (1)

- Indian Electricals Limited (Complete) 1Документ8 страницIndian Electricals Limited (Complete) 1Prashant BarsingОценок пока нет

- Hamilton - Case A - 5 PDFДокумент2 страницыHamilton - Case A - 5 PDFJayash Kaushal0% (1)

- Case Problem EZ Trailers, Inc.Документ3 страницыCase Problem EZ Trailers, Inc.Something ChicОценок пока нет

- Stafford Press SolvedДокумент2 страницыStafford Press SolvedMurali DharanОценок пока нет

- Problem Set 1 PDFДокумент3 страницыProblem Set 1 PDFrenjith0% (2)

- Northboro Machine Tools CorporationДокумент9 страницNorthboro Machine Tools Corporationsheersha kkОценок пока нет

- Breathe Screen Inc CommentsДокумент2 страницыBreathe Screen Inc CommentsSanchit Duggal100% (1)

- Case 7 3 StaffordДокумент5 страницCase 7 3 StaffordArjun Khosla0% (2)

- Solution AllДокумент4 страницыSolution AllLanka SaikiranОценок пока нет

- Himachal Fertilizers Corporation (A) : An Ethical ConundrumДокумент7 страницHimachal Fertilizers Corporation (A) : An Ethical Conundrumkrishna sharma50% (2)

- Stafford Press CaseДокумент4 страницыStafford Press CaseAmit Kumar AroraОценок пока нет

- Solman 12 Second EdДокумент23 страницыSolman 12 Second Edferozesheriff50% (2)

- Amore PacificДокумент12 страницAmore PacificAditiaSoviaОценок пока нет

- Modern Pharma SolnДокумент3 страницыModern Pharma SolnSakshiОценок пока нет

- Rosemont Health Center Rev01Документ7 страницRosemont Health Center Rev01Amit VishwakarmaОценок пока нет

- 4thsession - RIL Bonds CaseДокумент6 страниц4thsession - RIL Bonds CaseVignesh_230% (2)

- Case ChemaliteДокумент1 страницаCase ChemaliteRosario PhillipsОценок пока нет

- HEWLETT PACKARD - Computer Systems Organization: Selling To Enterprise CustomersДокумент16 страницHEWLETT PACKARD - Computer Systems Organization: Selling To Enterprise CustomersAbhishek GaikwadОценок пока нет

- About This TemplateДокумент4 страницыAbout This TemplateianachieviciОценок пока нет

- Orgl 3331-Dddmii - Artifact-Rgv Memo v2Документ9 страницOrgl 3331-Dddmii - Artifact-Rgv Memo v2api-632483826Оценок пока нет

- Project Report: IT & IT Enabled UnitДокумент58 страницProject Report: IT & IT Enabled Unitdeshdeepak srivastavaОценок пока нет

- SteamДокумент8 страницSteamdulceОценок пока нет

- SSantos - Accounting Analysis Assignment 4 PDFДокумент13 страницSSantos - Accounting Analysis Assignment 4 PDFSimone SassDiddy SantosОценок пока нет

- Annual Business BudgetДокумент4 страницыAnnual Business BudgetdanielebenezerОценок пока нет

- Chapter 7 Supplement 1Документ9 страницChapter 7 Supplement 1nigam34Оценок пока нет

- Personal Monthly Budget 1Документ1 страницаPersonal Monthly Budget 1Antonio Centeno BenjaminОценок пока нет

- Project Status Reporting - V5Документ14 страницProject Status Reporting - V5Talks of MindsОценок пока нет

- 12 Month Cash Flow statement1AZXДокумент17 страниц12 Month Cash Flow statement1AZXTehseenHussainNasirОценок пока нет

- Account YTD YTD Remaining Number Account Title Actual Budget Budget $Документ17 страницAccount YTD YTD Remaining Number Account Title Actual Budget Budget $mukhleshОценок пока нет

- 17-BMR League-Organizers ReqId 050820191950 1565094504347Документ1 страница17-BMR League-Organizers ReqId 050820191950 1565094504347Anamika ChauhanОценок пока нет

- Investments: List of All Funding Rounds in Esports League Organizers Market by StageДокумент1 страницаInvestments: List of All Funding Rounds in Esports League Organizers Market by StageAnamika ChauhanОценок пока нет

- 18-BMR League-Organizers ReqId 050820191950 1565094504347Документ1 страница18-BMR League-Organizers ReqId 050820191950 1565094504347Anamika ChauhanОценок пока нет

- Investments: List of All Funding Rounds in Esports League Organizers Market by StageДокумент1 страницаInvestments: List of All Funding Rounds in Esports League Organizers Market by StageAnamika ChauhanОценок пока нет

- 9 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsДокумент1 страница9 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsAnamika ChauhanОценок пока нет

- 10 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsДокумент1 страница10 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsAnamika ChauhanОценок пока нет

- 3 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsДокумент1 страница3 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsAnamika ChauhanОценок пока нет

- 2 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsДокумент1 страница2 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsAnamika ChauhanОценок пока нет

- 1 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsДокумент1 страница1 - (23005661 - Foundations of Management) Digital Transformation of Business ModelsAnamika ChauhanОценок пока нет

- BusinessPlan 23092020Документ13 страницBusinessPlan 23092020Anamika ChauhanОценок пока нет

- CBS Digital Business Leadership Program 2020 Brochure PDFДокумент28 страницCBS Digital Business Leadership Program 2020 Brochure PDFAnamika ChauhanОценок пока нет

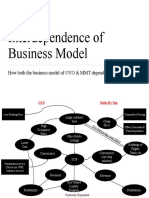

- Interdependence of Business Model: How Both The Business Model of OYO & MMT Dependent On Each Other?Документ2 страницыInterdependence of Business Model: How Both The Business Model of OYO & MMT Dependent On Each Other?Anamika ChauhanОценок пока нет

- Business Plan: 23 September2020Документ13 страницBusiness Plan: 23 September2020Anamika ChauhanОценок пока нет

- Ic 86 Real Feel TestДокумент54 страницыIc 86 Real Feel TestSamba SivaОценок пока нет

- Costing English Answer 14.07.2020Документ12 страницCosting English Answer 14.07.2020Prathmesh JambhulkarОценок пока нет

- Ch08 Responsibility Accounting, Segment Evaluation and Transfer Pricing PDFДокумент10 страницCh08 Responsibility Accounting, Segment Evaluation and Transfer Pricing PDFjdiaz_646247Оценок пока нет

- VariancesДокумент3 страницыVariancesShashankSinghОценок пока нет

- 8011 and 9011 AS - A Level Accounting Syllabus 2005Документ16 страниц8011 and 9011 AS - A Level Accounting Syllabus 2005Haran MuraliОценок пока нет

- Business-Plan g5 EntrepДокумент11 страницBusiness-Plan g5 EntrepVirly MelladoОценок пока нет

- Udah Bener'Документ4 страницыUdah Bener'Shafa AzahraОценок пока нет

- Productivity Class Practice Problems OM July 2019 UpdatedДокумент17 страницProductivity Class Practice Problems OM July 2019 UpdatedVinodshankar BhatОценок пока нет

- 2009 B-5 Class Questions PreviewДокумент10 страниц2009 B-5 Class Questions PreviewMarizMatampaleОценок пока нет

- Budget 010212Документ11 страницBudget 010212Sourav SanghiОценок пока нет

- Romanian Chart of AccountsДокумент16 страницRomanian Chart of AccountsLiviu_55Оценок пока нет

- Man Acct Exam 2018S1 PDBTAДокумент6 страницMan Acct Exam 2018S1 PDBTAkwameОценок пока нет

- Mas - 4Документ12 страницMas - 4AzureBlazeОценок пока нет

- Financial & Managerial Accounting: Information For DecisionsДокумент79 страницFinancial & Managerial Accounting: Information For DecisionsMarnelli PerezОценок пока нет

- Managerial Accounting Canadian 11th Edition Garrison Test BankДокумент35 страницManagerial Accounting Canadian 11th Edition Garrison Test Bankdeandavidsontldp100% (23)

- Revision Excercises Midterm Cost Accounting CA232Документ6 страницRevision Excercises Midterm Cost Accounting CA232Chacha gmidОценок пока нет

- PPT1Документ63 страницыPPT1Jane FransiscaОценок пока нет

- Basic Cost ConceptДокумент43 страницыBasic Cost ConceptAaron WidofanОценок пока нет

- Diffusionofnewmanagementaccountingpractices IndiaДокумент26 страницDiffusionofnewmanagementaccountingpractices IndiaWasis KurniawanОценок пока нет

- Paper 7 Cost & Management AccountingДокумент6 страницPaper 7 Cost & Management AccountingTuryamureeba Julius100% (1)

- Problem 5-51 BlocherДокумент2 страницыProblem 5-51 BlocherAlif ArmadanaОценок пока нет

- 28 Cas 13 Cost Accounting Standard On Cost of Service Cost CentreДокумент7 страниц28 Cas 13 Cost Accounting Standard On Cost of Service Cost CentrekoshaleshwarОценок пока нет

- Tugas Week 11Документ2 страницыTugas Week 11Rifda AmaliaОценок пока нет

- Câu 32 Trong Hình Tao Gửi Sai Nên Ai Làm Phần Đó Nhớ Sửa LạiДокумент11 страницCâu 32 Trong Hình Tao Gửi Sai Nên Ai Làm Phần Đó Nhớ Sửa LạiNhu Le ThaoОценок пока нет