Вам также может понравиться

- Research Work NEWДокумент17 страницResearch Work NEWRitikaОценок пока нет

- UNIT 3 BBA VI SemДокумент17 страницUNIT 3 BBA VI SemRitikaОценок пока нет

- Sales Model in Financial Products: Dsa/Dma, Casa Strategy, Cross Selling, Priority BankingДокумент12 страницSales Model in Financial Products: Dsa/Dma, Casa Strategy, Cross Selling, Priority BankingRitikaОценок пока нет

- Chapt Er 26: Nature and Process of ControllingДокумент12 страницChapt Er 26: Nature and Process of ControllingRitikaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Statement of Receipts SourcesДокумент3 страницыStatement of Receipts SourcesctoadminОценок пока нет

- AIS615 PBL QUESTION MAC-JUNE2019 UiTM SARAWAKДокумент6 страницAIS615 PBL QUESTION MAC-JUNE2019 UiTM SARAWAKMon Luffy100% (2)

- State of The Municipality Address by Mayor Rolando B. Distura 2013, Dumangas, IloiloДокумент102 страницыState of The Municipality Address by Mayor Rolando B. Distura 2013, Dumangas, IloiloLakanPHОценок пока нет

- Budgeting For Planning and ControlДокумент23 страницыBudgeting For Planning and ControlMuhammad AbrarОценок пока нет

- ACIB Past Questions PDFДокумент208 страницACIB Past Questions PDFdamola2real100% (1)

- Costacctg13 SolPPT ch02Документ18 страницCostacctg13 SolPPT ch02eriski_1100% (2)

- Index: SR - No Topic PG No RemarksДокумент21 страницаIndex: SR - No Topic PG No RemarksFatema PrimaswallaОценок пока нет

- Maths Project: Planning A Home BudgetДокумент10 страницMaths Project: Planning A Home BudgetFaiz100% (8)

- A Marketing Plan For HSBC NomanДокумент8 страницA Marketing Plan For HSBC Nomanhassan_MuqarrabОценок пока нет

- Chap 001Документ19 страницChap 001WilliamОценок пока нет

- Phiamphu TrustДокумент12 страницPhiamphu TrustHau PhiamphuОценок пока нет

- ACCT 3110 CH 7 Homework E 4 8 13 19 20 27Документ7 страницACCT 3110 CH 7 Homework E 4 8 13 19 20 27John Job100% (1)

- Practice Problem On Capital BudgetingДокумент29 страницPractice Problem On Capital BudgetingPadyala Sriram90% (10)

- Boral Investor PresentationДокумент43 страницыBoral Investor PresentationTim MooreОценок пока нет

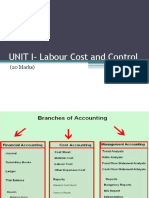

- Labour Cost and ControlДокумент65 страницLabour Cost and Controlaishwarya raikarОценок пока нет

- Literature ReviewДокумент9 страницLiterature ReviewDaleОценок пока нет

- Financial Accounting and Reporting EllioДокумент181 страницаFinancial Accounting and Reporting EllioThủy Thiều Thị HồngОценок пока нет

- BP Plastic, AnalysisДокумент5 страницBP Plastic, AnalysisChiaki HidayahОценок пока нет

- FSA - Tutorial 6-Fall 2021Документ5 страницFSA - Tutorial 6-Fall 2021Ging freexОценок пока нет

- Railway Accounting: Indian Railway Accounts ServiceДокумент5 страницRailway Accounting: Indian Railway Accounts ServiceAbhijeet AsthanaОценок пока нет

- Topic TwoДокумент67 страницTopic TwoMerediths KrisKringleОценок пока нет

- Estate and Donor RulingsДокумент27 страницEstate and Donor Rulingscmv mendozaОценок пока нет

- Gross Estate InclusionДокумент4 страницыGross Estate InclusionAlaineОценок пока нет

- Philippine National Bank vs. Court of Appeals G.R. No. 97995 - January 21, 1993 FactsДокумент5 страницPhilippine National Bank vs. Court of Appeals G.R. No. 97995 - January 21, 1993 FactsPatricia SanchezОценок пока нет

- Cir Vs CaДокумент11 страницCir Vs Caeinel dcОценок пока нет

- FS 2020 Queries AnsweredДокумент44 страницыFS 2020 Queries AnsweredCha MaderazoОценок пока нет

- To Do Path: How To Define Company StructureДокумент55 страницTo Do Path: How To Define Company Structurepragyaa4Оценок пока нет

- Motion To Sell Adak PlantДокумент12 страницMotion To Sell Adak PlantDeckbossОценок пока нет

- High School Franchise Rs. 8.02 Million Sep-2020Документ19 страницHigh School Franchise Rs. 8.02 Million Sep-2020Zeeshan NazirОценок пока нет

- Margo Depression Family Group WorkДокумент17 страницMargo Depression Family Group Workapi-284278077100% (6)