Вам также может понравиться

- Module 3 Nominal and Effective IRДокумент19 страницModule 3 Nominal and Effective IRkikiОценок пока нет

- SRDC Method v1.3Документ66 страницSRDC Method v1.3api-3816484100% (3)

- Cfroi HoltДокумент7 страницCfroi Holtamro_baryОценок пока нет

- EC3332 Tutorial 3 AnswersДокумент3 страницыEC3332 Tutorial 3 AnswersKabir MishraОценок пока нет

- Lecture 7 - Budget & TreasuryДокумент81 страницаLecture 7 - Budget & TreasuryHüsən PirmuradovОценок пока нет

- Modelling Cost at Risk - A Preliminary Approach - 0Документ16 страницModelling Cost at Risk - A Preliminary Approach - 0Uzair Ul HaqОценок пока нет

- TD 2014.04 - Versão FinalДокумент43 страницыTD 2014.04 - Versão Finaljc224Оценок пока нет

- MODULE 2 - Introduction To Measuring FDFIДокумент37 страницMODULE 2 - Introduction To Measuring FDFIEricaОценок пока нет

- Fiscal Exposures: Implications For Debt Management and The Role For SaisДокумент48 страницFiscal Exposures: Implications For Debt Management and The Role For SaisCherry R. SanchezОценок пока нет

- Debt Management Policies SwedenДокумент11 страницDebt Management Policies SwedenTamoghna Sadhu100% (1)

- ProjectДокумент11 страницProjectFatima MubarakОценок пока нет

- Imf Troika Report DntekДокумент31 страницаImf Troika Report DntektakzacharОценок пока нет

- Sovereign Debt AnalysisДокумент25 страницSovereign Debt AnalysisWellington MudyawabikwaОценок пока нет

- Identifying The Objectives and Scope For Debt Management, MTDS: Step 1Документ17 страницIdentifying The Objectives and Scope For Debt Management, MTDS: Step 1HarpreetОценок пока нет

- World Bank Debt Management: Questions and AnswersДокумент20 страницWorld Bank Debt Management: Questions and Answersk_Dashy8465Оценок пока нет

- IMF - Christian MulderДокумент22 страницыIMF - Christian MulderAsian Development BankОценок пока нет

- Staff Guidance Note On The Implementation of Public Debt Limits in Fund-Supported ProgramsДокумент33 страницыStaff Guidance Note On The Implementation of Public Debt Limits in Fund-Supported ProgramsLiliya RepaОценок пока нет

- IMF Public Debt ManagementДокумент37 страницIMF Public Debt ManagementTanisha singhОценок пока нет

- Lesson 5 - DFI 301 MONETARY POLICYpptxДокумент26 страницLesson 5 - DFI 301 MONETARY POLICYpptxsaiidОценок пока нет

- Paper - Teoria de CuerdasДокумент12 страницPaper - Teoria de CuerdasSolver TutorОценок пока нет

- Probability of DefaultДокумент5 страницProbability of DefaultafjkjchhghgfbfОценок пока нет

- Preparing For Basel II Modeling Requirements: Part 4: Stress TestingДокумент6 страницPreparing For Basel II Modeling Requirements: Part 4: Stress Testingjbsimha3629Оценок пока нет

- Government Cash Management Good - and Bad - Practice: Mike WilliamsДокумент33 страницыGovernment Cash Management Good - and Bad - Practice: Mike WilliamslelumenОценок пока нет

- Literature ReviewДокумент3 страницыLiterature ReviewneerjamОценок пока нет

- Parameters of MPДокумент10 страницParameters of MPJuglaryОценок пока нет

- Lazzari Wong - Dimension ReductionДокумент73 страницыLazzari Wong - Dimension ReductionCourtney WilliamsОценок пока нет

- Practical Ifrs 09Документ10 страницPractical Ifrs 09Farooq HaiderОценок пока нет

- Role of Treasury FunctionДокумент4 страницыRole of Treasury Functionadnan040% (1)

- Chapter 9 - Interest Rate and Currency Swaps (Q&A)Документ5 страницChapter 9 - Interest Rate and Currency Swaps (Q&A)Nuraisyahnadhirah MohamadtaibОценок пока нет

- Macroprudential Policy Interactions in A Sectoral Dsge Model With Staggered Interest RatesДокумент64 страницыMacroprudential Policy Interactions in A Sectoral Dsge Model With Staggered Interest RatesjackieОценок пока нет

- IMF-Supported Programs and Crisis Prevention: An Analytical FrameworkДокумент39 страницIMF-Supported Programs and Crisis Prevention: An Analytical Frameworkjgun73Оценок пока нет

- Debt - and Reserve-Related Indicators of External VulnerabilityДокумент54 страницыDebt - and Reserve-Related Indicators of External VulnerabilityMuhammad Abubakar RiazОценок пока нет

- Chapter 4 Credit Portfolio ManagementДокумент12 страницChapter 4 Credit Portfolio ManagementCarl AbruquahОценок пока нет

- What Is Asset and Liability ManagementДокумент18 страницWhat Is Asset and Liability ManagementRuhi KapoorОценок пока нет

- IMF StatisticalDeftPublicSectorDebtДокумент21 страницаIMF StatisticalDeftPublicSectorDebtligia.ourivesОценок пока нет

- Executive Summary by Dr. Eugene Brigham and Dr. Joel HoustonДокумент12 страницExecutive Summary by Dr. Eugene Brigham and Dr. Joel HoustonCharisseMaeM.CarreonОценок пока нет

- Resume 11Документ5 страницResume 11MariaОценок пока нет

- Moody's App To RTG Con LN ABS 2012Документ21 страницаMoody's App To RTG Con LN ABS 2012Zaid AbdulrahmanОценок пока нет

- RAROC ValuationДокумент20 страницRAROC ValuationRochak AgarwalОценок пока нет

- Khade IFДокумент47 страницKhade IFPratik GosaviОценок пока нет

- Using SAS For Effective Credit Risk ManagementДокумент10 страницUsing SAS For Effective Credit Risk ManagementaminiotisОценок пока нет

- CONCEPTUAL FRAMEWORK PROGRAMME - VIII - (B)Документ8 страницCONCEPTUAL FRAMEWORK PROGRAMME - VIII - (B)najiath mzeeОценок пока нет

- Recommendations of Narsimha CommitteeДокумент10 страницRecommendations of Narsimha CommitteePrathamesh DeoОценок пока нет

- ShadzДокумент13 страницShadzAjinkya AgrawalОценок пока нет

- Stress Testing of Firm Level Credit RiskДокумент34 страницыStress Testing of Firm Level Credit RiskjeganrajrajОценок пока нет

- Budjet Estimate, Performance BudjetДокумент28 страницBudjet Estimate, Performance BudjetYashoda SatputeОценок пока нет

- W I L L Tolerate Considerable: SalaryДокумент2 страницыW I L L Tolerate Considerable: Salarymq5cltОценок пока нет

- Flash Memory StatementДокумент4 страницыFlash Memory StatementVeso OjiamboОценок пока нет

- Financial TransactionsДокумент5 страницFinancial TransactionsmehdiОценок пока нет

- Alm Review of LiteratureДокумент17 страницAlm Review of LiteratureSai ViswasОценок пока нет

- Corporate Finance - Assignment1Документ16 страницCorporate Finance - Assignment1pranav1931129Оценок пока нет

- Bank of England, Tha Role of Macroprudential PolicyДокумент38 страницBank of England, Tha Role of Macroprudential PolicyCliffordTorresОценок пока нет

- Mahnoor FRM Bba 182040Документ3 страницыMahnoor FRM Bba 182040mahnoor amirОценок пока нет

- Innov. in Banking Proj.Документ6 страницInnov. in Banking Proj.Yog CoolОценок пока нет

- Project Report On Treasury ManagementДокумент6 страницProject Report On Treasury ManagementnoordonОценок пока нет

- Research Paper On Debt RestructuringДокумент7 страницResearch Paper On Debt Restructuringafnhfbgwoezeoj100% (1)

- Multinational Capital Budgeting Presentation.Документ14 страницMultinational Capital Budgeting Presentation.Edlamu AlemieОценок пока нет

- Sovereign Debt Management: A Risk Management Focus: Ian Storkey Storkey & Co LimitedДокумент4 страницыSovereign Debt Management: A Risk Management Focus: Ian Storkey Storkey & Co LimitedSaurav SinghОценок пока нет

- Asset Liability Management in BanksДокумент8 страницAsset Liability Management in Bankskpved92Оценок пока нет

- Name of The Student Course Professor University FinanceДокумент16 страницName of The Student Course Professor University FinanceBharat KoiralaОценок пока нет

- Central Bank Digital Currencies - Financial Stability Implications (BIS)Документ30 страницCentral Bank Digital Currencies - Financial Stability Implications (BIS)Ji_yОценок пока нет

- The Basel II Risk Parameters: Estimation, Validation, Stress Testing - with Applications to Loan Risk ManagementОт EverandThe Basel II Risk Parameters: Estimation, Validation, Stress Testing - with Applications to Loan Risk ManagementРейтинг: 1 из 5 звезд1/5 (1)

- Work Within Legal & Ethical Framework CHCCS301A PDFДокумент78 страницWork Within Legal & Ethical Framework CHCCS301A PDFqwertyuiopОценок пока нет

- Issue GRE PDFДокумент16 страницIssue GRE PDFqwertyuiopОценок пока нет

- Honor Killing in IndiaДокумент2 страницыHonor Killing in IndiaqwertyuiopОценок пока нет

- GRE AWA Practice PDFДокумент12 страницGRE AWA Practice PDFqwertyuiopОценок пока нет

- GRE Analytical Writing Sample GT PDFДокумент27 страницGRE Analytical Writing Sample GT PDFqwertyuiopОценок пока нет

- Health Aff-1992-Priester-84-107 PDFДокумент26 страницHealth Aff-1992-Priester-84-107 PDFqwertyuiopОценок пока нет

- AnnualReport 0708 PDFДокумент454 страницыAnnualReport 0708 PDFqwertyuiopОценок пока нет

- Institution of Ombudsman Was First Conceived and Put Into Operation in SwedenДокумент1 страницаInstitution of Ombudsman Was First Conceived and Put Into Operation in SwedenqwertyuiopОценок пока нет

- 792 Pages PDFДокумент792 страницы792 Pages PDFsfavОценок пока нет

- Guests Are GodДокумент1 страницаGuests Are GodqwertyuiopОценок пока нет

- Principles of Mangement mg2351 Notes PDFДокумент156 страницPrinciples of Mangement mg2351 Notes PDFAshishHegdeОценок пока нет

- A Change of LuckДокумент5 страницA Change of LuckqwertyuiopОценок пока нет

- CH 30 Mod 2 BSM Option Pricing FunctionДокумент1 страницаCH 30 Mod 2 BSM Option Pricing FunctionqwertyuiopОценок пока нет

- Banas EcoДокумент22 страницыBanas EcoVipul RanjanОценок пока нет

- Wage Price Setting 2016 10 17 10 26 34Документ18 страницWage Price Setting 2016 10 17 10 26 34qwertyuiopОценок пока нет

- GVHJNДокумент3 страницыGVHJNqwertyuiopОценок пока нет

- Civil Engineer Resume TemplateДокумент1 страницаCivil Engineer Resume TemplateJulius Vincent C. CalipongОценок пока нет

- Viii. C E: W D S A ?: Hapter Ight Hat Is EBT Ustainability NalysisДокумент24 страницыViii. C E: W D S A ?: Hapter Ight Hat Is EBT Ustainability NalysisqwertyuiopОценок пока нет

- CUTN QuestionPaper Computational ESДокумент2 страницыCUTN QuestionPaper Computational ESqwertyuiopОценок пока нет

- How Comparable Are India's Labour Market Surveys?: CSE Working PaperДокумент28 страницHow Comparable Are India's Labour Market Surveys?: CSE Working PaperqwertyuiopОценок пока нет

- Part 2 Unit 9 DebtopiaДокумент35 страницPart 2 Unit 9 DebtopiaqwertyuiopОценок пока нет

- Ilo - Low Female LFPR in IndiaДокумент2 страницыIlo - Low Female LFPR in IndiasivaramanlbОценок пока нет

- Part 2 Unit 4 Debtopia BaselineДокумент33 страницыPart 2 Unit 4 Debtopia BaselineqwertyuiopОценок пока нет

- Outsmart The Po PoДокумент3 страницыOutsmart The Po PoqwertyuiopОценок пока нет

- Skills For The Growth Sub-Sectors in The Agricultural and Informal SectorsДокумент13 страницSkills For The Growth Sub-Sectors in The Agricultural and Informal SectorsqwertyuiopОценок пока нет

- FPP1x Video Transcript Module 0Документ13 страницFPP1x Video Transcript Module 0qwertyuiopОценок пока нет

- FPP1x Video Transcript Module 4Документ36 страницFPP1x Video Transcript Module 4qwertyuiopОценок пока нет

- E-40 Lyrics: "Drought Season"Документ3 страницыE-40 Lyrics: "Drought Season"qwertyuiopОценок пока нет

- Office Market Snapshot: Northern VirginiaДокумент2 страницыOffice Market Snapshot: Northern VirginiaAnonymous Feglbx5Оценок пока нет

- International Financial Management Abridged 10 Edition: by Jeff MaduraДокумент21 страницаInternational Financial Management Abridged 10 Edition: by Jeff MaduraZohaib MaqboolОценок пока нет

- Coaltraderintl PlattsДокумент10 страницCoaltraderintl PlattsAnonymous wze4zUОценок пока нет

- L06 (1) - IMF's Vulnerability Exercise For Emerging Economies (VEE)Документ48 страницL06 (1) - IMF's Vulnerability Exercise For Emerging Economies (VEE)Dekon MakroОценок пока нет

- Hedging With Options: Peter Carr Bloomberg LP/Courant Institute, NYUДокумент48 страницHedging With Options: Peter Carr Bloomberg LP/Courant Institute, NYUKarthick NklОценок пока нет

- Nism Series V B - Mutual Fund Foundation ExamДокумент17 страницNism Series V B - Mutual Fund Foundation Examnewbie1947Оценок пока нет

- Introducing To FinanceДокумент38 страницIntroducing To FinancejuliancaoОценок пока нет

- The 2011 J. P. Morgan Global ETF HandbookДокумент48 страницThe 2011 J. P. Morgan Global ETF HandbooklgfinanceОценок пока нет

- Money Word PuzzleДокумент2 страницыMoney Word PuzzleMaria Chacón CarbajalОценок пока нет

- 3 TIMELESS Setups That Have Made Me TENS OF MILLIONS! - QullamaggieДокумент1 страница3 TIMELESS Setups That Have Made Me TENS OF MILLIONS! - Qullamaggietawatchai lim100% (1)

- 2015 BT2 CS Question Paper FinalДокумент9 страниц2015 BT2 CS Question Paper FinalsaffronОценок пока нет

- Stock Market of BangladeshДокумент13 страницStock Market of BangladeshPaul DonОценок пока нет

- Constituents of The Financial System DD Intro NewДокумент17 страницConstituents of The Financial System DD Intro NewAnonymous bf1cFDuepPОценок пока нет

- 2010 08 21 - 142723 - P11 2aДокумент3 страницы2010 08 21 - 142723 - P11 2aJessica DragonIvyОценок пока нет

- Map Financial MarketesДокумент3 страницыMap Financial MarketesBryan Ivann MacasinagОценок пока нет

- Disgorge The Cash: The Disconnect Between Corporate Borrowing and InvestmentДокумент38 страницDisgorge The Cash: The Disconnect Between Corporate Borrowing and InvestmentRoosevelt Institute100% (1)

- 2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebДокумент51 страница2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebOmar A TavarezОценок пока нет

- India Case StudyДокумент4 страницыIndia Case StudyMakame Mahmud DiptaОценок пока нет

- STPM Integration SolutionДокумент8 страницSTPM Integration SolutionSKОценок пока нет

- Chapter 7Документ25 страницChapter 7Cynthia AdiantiОценок пока нет

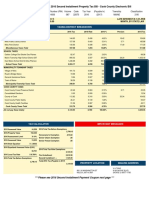

- Cook County Propertytax Bill 2016 Second InstallmentДокумент2 страницыCook County Propertytax Bill 2016 Second InstallmentbenОценок пока нет

- Book 29.04.2011Документ432 страницыBook 29.04.2011David Kommers BarrientosОценок пока нет

- 1234 WWWWДокумент11 страниц1234 WWWWbrainhub50Оценок пока нет

- Factsheet NIFTY Quality Low-Volatility 30Документ2 страницыFactsheet NIFTY Quality Low-Volatility 30Rajesh KumarОценок пока нет

- Black Scholes DerivationДокумент4 страницыBlack Scholes DerivationNathan EsauОценок пока нет

- Index of ContentsДокумент1 страницаIndex of ContentskrutibhattОценок пока нет

- Operations and Mechanism of Mutual Funds CoДокумент11 страницOperations and Mechanism of Mutual Funds CoShobhit ShuklaОценок пока нет