Вам также может понравиться

- PRM Handbook Introduction and ContentsДокумент23 страницыPRM Handbook Introduction and ContentsMike Wong0% (1)

- Economic Capital Allocation with Basel II: Cost, Benefit and Implementation ProceduresОт EverandEconomic Capital Allocation with Basel II: Cost, Benefit and Implementation ProceduresОценок пока нет

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsОт EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsОценок пока нет

- Measuring Operational and Reputational Risk: A Practitioner's ApproachОт EverandMeasuring Operational and Reputational Risk: A Practitioner's ApproachРейтинг: 5 из 5 звезд5/5 (1)

- Risk Management At The Top: A Guide to Risk and its Governance in Financial InstitutionsОт EverandRisk Management At The Top: A Guide to Risk and its Governance in Financial InstitutionsРейтинг: 5 из 5 звезд5/5 (2)

- Economic Capital: How It Works, and What Every Manager Needs to KnowОт EverandEconomic Capital: How It Works, and What Every Manager Needs to KnowОценок пока нет

- Operational Risk Management System A Complete Guide - 2020 EditionОт EverandOperational Risk Management System A Complete Guide - 2020 EditionОценок пока нет

- Operational Risk Modeling in Financial Services: The Exposure, Occurrence, Impact MethodОт EverandOperational Risk Modeling in Financial Services: The Exposure, Occurrence, Impact MethodОценок пока нет

- The Essentials of Risk Management, Second EditionОт EverandThe Essentials of Risk Management, Second EditionРейтинг: 2 из 5 звезд2/5 (7)

- Pricing, Risk, and Performance Measurement in Practice: The Building Block Approach to Modeling Instruments and PortfoliosОт EverandPricing, Risk, and Performance Measurement in Practice: The Building Block Approach to Modeling Instruments and PortfoliosОценок пока нет

- ISO 31000 Risk Management Best Practice A Complete Guide - 2020 EditionОт EverandISO 31000 Risk Management Best Practice A Complete Guide - 2020 EditionОценок пока нет

- Operational Risk Control with Basel II: Basic Principles and Capital RequirementsОт EverandOperational Risk Control with Basel II: Basic Principles and Capital RequirementsОценок пока нет

- Enterprise Risk Management Plan A Complete Guide - 2021 EditionОт EverandEnterprise Risk Management Plan A Complete Guide - 2021 EditionОценок пока нет

- Value at Risk and Bank Capital Management: Risk Adjusted Performances, Capital Management and Capital Allocation Decision MakingОт EverandValue at Risk and Bank Capital Management: Risk Adjusted Performances, Capital Management and Capital Allocation Decision MakingОценок пока нет

- Third Party Risk Management Framework A Complete Guide - 2021 EditionОт EverandThird Party Risk Management Framework A Complete Guide - 2021 EditionОценок пока нет

- Risk Management Technology in Financial Services: Risk Control, Stress Testing, Models, and IT Systems and StructuresОт EverandRisk Management Technology in Financial Services: Risk Control, Stress Testing, Models, and IT Systems and StructuresОценок пока нет

- Basel II-III Credit Risk Modelling and Validation Training BrochureДокумент7 страницBasel II-III Credit Risk Modelling and Validation Training BrochuremakorecОценок пока нет

- PRM QuestДокумент18 страницPRM QuestabhijeetkaushalОценок пока нет

- IT Security Risk Assessment A Complete Guide - 2020 EditionОт EverandIT Security Risk Assessment A Complete Guide - 2020 EditionОценок пока нет

- Operational Risk with Excel and VBA: Applied Statistical Methods for Risk Management, + WebsiteОт EverandOperational Risk with Excel and VBA: Applied Statistical Methods for Risk Management, + WebsiteРейтинг: 3 из 5 звезд3/5 (1)

- Financial Risk Management: Applications in Market, Credit, Asset and Liability Management and Firmwide RiskОт EverandFinancial Risk Management: Applications in Market, Credit, Asset and Liability Management and Firmwide RiskОценок пока нет

- Financial Risk Management: A Practitioner's Guide to Managing Market and Credit RiskОт EverandFinancial Risk Management: A Practitioner's Guide to Managing Market and Credit RiskРейтинг: 2.5 из 5 звезд2.5/5 (2)

- Operations Risk: Managing a Key Component of Operational RiskОт EverandOperations Risk: Managing a Key Component of Operational RiskРейтинг: 4 из 5 звезд4/5 (2)

- Bank Risk Management in Developing Economies: Addressing the Unique Challenges of Domestic BanksОт EverandBank Risk Management in Developing Economies: Addressing the Unique Challenges of Domestic BanksОценок пока нет

- Evaluation of Value at Risk-ModelsДокумент58 страницEvaluation of Value at Risk-ModelsEphone HoОценок пока нет

- Risk Management: Foundations For a Changing Financial WorldОт EverandRisk Management: Foundations For a Changing Financial WorldWalter V. "Bud" Haslett, Jr.Рейтинг: 3 из 5 звезд3/5 (1)

- Alternative Risk Transfer: Integrated Risk Management through Insurance, Reinsurance, and the Capital MarketsОт EverandAlternative Risk Transfer: Integrated Risk Management through Insurance, Reinsurance, and the Capital MarketsОценок пока нет

- CH 6 Credit Risk Measurement and Management 8KUA8G1F13Документ202 страницыCH 6 Credit Risk Measurement and Management 8KUA8G1F13Tushar MehndirattaОценок пока нет

- BASEL 3 - Interest Rate Risk in The Banking BookДокумент51 страницаBASEL 3 - Interest Rate Risk in The Banking BookJenny DangОценок пока нет

- 2019 FRM Study GuideДокумент26 страниц2019 FRM Study GuideRavinder Kumar100% (4)

- The FRM Exam - What To DoДокумент51 страницаThe FRM Exam - What To DoAditya BajoriaОценок пока нет

- GARP FRM Practice Exam 2011 Level2Документ63 страницыGARP FRM Practice Exam 2011 Level2Kelvin TanОценок пока нет

- MlArm GuidebookДокумент8 страницMlArm GuidebookMzukisi0% (1)

- Market Risk SlidesДокумент80 страницMarket Risk SlidesChen Lee Kuen100% (5)

- Pragya: The Best FRM Revision Course!Документ26 страницPragya: The Best FRM Revision Course!mohamedОценок пока нет

- FRM Part II Mock ExamДокумент96 страницFRM Part II Mock Examdudesaggi.bhuvanОценок пока нет

- Samlpe Questions FMP FRM IДокумент6 страницSamlpe Questions FMP FRM IShreyans Jain0% (1)

- Sample Foundations v1Документ10 страницSample Foundations v1Lu KingОценок пока нет

- Guidelines On Risk Appetite Practices For BanksДокумент34 страницыGuidelines On Risk Appetite Practices For BanksPRIME ConsultoresОценок пока нет

- FRM Learning Objectives 2023Документ58 страницFRM Learning Objectives 2023Tejas JoshiОценок пока нет

- Designed To Deliver Exam Day Excellence.: The Iia'S Cia Learning SystemДокумент4 страницыDesigned To Deliver Exam Day Excellence.: The Iia'S Cia Learning SystemSyed Muhammad HassanОценок пока нет

- SAMPLE Master Distribution Agreement DRAFT 042213 (3) - 1Документ17 страницSAMPLE Master Distribution Agreement DRAFT 042213 (3) - 1Syed Muhammad HassanОценок пока нет

- OnRisk 2020 ReportДокумент40 страницOnRisk 2020 ReportSyed Muhammad HassanОценок пока нет

- Guideline - Food Guideline - Food Business Licence ApplicationBusiness Licence ApplicationДокумент19 страницGuideline - Food Guideline - Food Business Licence ApplicationBusiness Licence ApplicationSyed Muhammad HassanОценок пока нет

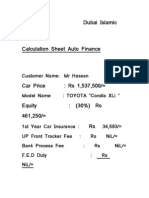

- Dubai Islamic Bank Calculation Sheet Auto Finance: Customer Name MR Hassan Model Name: Toyota "Corolla Xli "Документ3 страницыDubai Islamic Bank Calculation Sheet Auto Finance: Customer Name MR Hassan Model Name: Toyota "Corolla Xli "Syed Muhammad HassanОценок пока нет

- PSMCДокумент1 страницаPSMCSyed Muhammad HassanОценок пока нет

- Bulletin: Psychoacoustic Test Bench BZ 5301Документ1 страницаBulletin: Psychoacoustic Test Bench BZ 5301Brianna Daniela VARGAS MERMAОценок пока нет

- Q-3-Q-4 - PREDICTIVE ANALYTICS For ClassДокумент32 страницыQ-3-Q-4 - PREDICTIVE ANALYTICS For ClassRAJESH VОценок пока нет

- Soal Uas Statistik Lanjutan Ganjil 2017 2018 Utk Sahril Dewi Ratna SjariДокумент9 страницSoal Uas Statistik Lanjutan Ganjil 2017 2018 Utk Sahril Dewi Ratna SjariLuthfia Puspa wulandariОценок пока нет

- The Effect of Financial Literacy On Investment Decisions (A Study On Millennial Generation in Five Big Cities in Indonesia)Документ9 страницThe Effect of Financial Literacy On Investment Decisions (A Study On Millennial Generation in Five Big Cities in Indonesia)Yuslia Nandha Anasta SariОценок пока нет

- PGD DS BrochureДокумент9 страницPGD DS BrochureJASMER SINGH 1611118Оценок пока нет

- Attitude Toward Teamwork and Effective TeamingДокумент8 страницAttitude Toward Teamwork and Effective TeamingShiela May BarrientosОценок пока нет

- Wells Copper Smith 1994Документ29 страницWells Copper Smith 1994Dario PaezОценок пока нет

- BAC-note Za Corr & RegrДокумент26 страницBAC-note Za Corr & RegrEnock MaunyaОценок пока нет

- Dataset Security For Machine Learning: Data Poisoning, Backdoor Attacks, and DefensesДокумент37 страницDataset Security For Machine Learning: Data Poisoning, Backdoor Attacks, and DefensessdasdОценок пока нет

- Take Home Exam UkpДокумент4 страницыTake Home Exam Ukpvkey_viknes2579Оценок пока нет

- Ekonomi Sumber Daya ManusiaДокумент59 страницEkonomi Sumber Daya ManusiaRasyid FikriОценок пока нет

- Response Surface Augmented Moment Method For EfficientДокумент12 страницResponse Surface Augmented Moment Method For EfficientJa VaОценок пока нет

- IIyear R Mid2 Question BankДокумент2 страницыIIyear R Mid2 Question Bankssrkm guptaОценок пока нет

- Dias Et Al 2008Документ8 страницDias Et Al 2008Fru Toosie PaloozaОценок пока нет

- OutputДокумент6 страницOutputANNISAОценок пока нет

- Hydro Systems Engineering and ManagementДокумент8 страницHydro Systems Engineering and ManagementAvinash RaiОценок пока нет

- Basic Econometrics: The Nature of Regression AnalysisДокумент9 страницBasic Econometrics: The Nature of Regression AnalysisAmin HaleebОценок пока нет

- MAS224: Biostatistical Methods ProjectДокумент5 страницMAS224: Biostatistical Methods ProjectThu ThảoОценок пока нет

- Acemoglu Et Al. - 2014 - Democracy Does Cause Growth PDFДокумент66 страницAcemoglu Et Al. - 2014 - Democracy Does Cause Growth PDFindifferentjОценок пока нет

- Business Analytics June 2022 CalendarДокумент1 страницаBusiness Analytics June 2022 CalendarKowshik KunduОценок пока нет

- Saha-Petersen2012 Article DetectingPriceArtificialityAndДокумент18 страницSaha-Petersen2012 Article DetectingPriceArtificialityAndCarolina FajardoОценок пока нет

- The Perception of Investors Towards Initial Public Offering: Evidence of NepalДокумент11 страницThe Perception of Investors Towards Initial Public Offering: Evidence of NepalSunisha PoudelОценок пока нет

- DDE 602 Research MethodДокумент9 страницDDE 602 Research Methodமரு.ஆதம்Оценок пока нет

- TOPIC 4 - Curve Fiiting and InterpolationДокумент23 страницыTOPIC 4 - Curve Fiiting and InterpolationBryan YuОценок пока нет

- Binder 2Документ178 страницBinder 2Sarah TaniОценок пока нет

- Ekonometrika Terapan Lecture 1 2022Документ34 страницыEkonometrika Terapan Lecture 1 2022erickОценок пока нет

- Quantile RegressionДокумент122 страницыQuantile RegressionXurumela AtomicaОценок пока нет

- How To Model Residual Errors To Correct Time Series Forecasts With PythonДокумент22 страницыHow To Model Residual Errors To Correct Time Series Forecasts With PythonPradeep SinglaОценок пока нет

- CNHP 6000 Final Exam Study GuideДокумент1 страницаCNHP 6000 Final Exam Study Guideulka07Оценок пока нет

- Demand Estimation and ForecastingДокумент56 страницDemand Estimation and ForecastingAsnake GeremewОценок пока нет