Вам также может понравиться

- Best Buy Usa OriginalllДокумент1 страницаBest Buy Usa OriginalllmedОценок пока нет

- RA 10142 Financial Rehabilitation and Insolvency ActДокумент25 страницRA 10142 Financial Rehabilitation and Insolvency ActCharles DumasiОценок пока нет

- Vitality-Case Analysis: Vitality Health Enterprises IncДокумент5 страницVitality-Case Analysis: Vitality Health Enterprises IncChristina Williams0% (1)

- Strategic Management and Business Policy 15e, Global EditionДокумент37 страницStrategic Management and Business Policy 15e, Global EditionTeh Chu Leong0% (1)

- Caiib Information TechnologyДокумент474 страницыCaiib Information TechnologyBiswajit GhoshОценок пока нет

- Wilson - Lowi - Policy Types - FinalДокумент40 страницWilson - Lowi - Policy Types - FinalHiroaki OmuraОценок пока нет

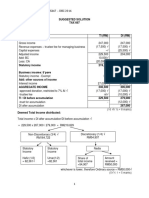

- SS CT 1 FAR270 Sem MAC2022 StudentДокумент4 страницыSS CT 1 FAR270 Sem MAC2022 Studentsharifah nurshahira sakinaОценок пока нет

- CT Question April 2018Документ4 страницыCT Question April 2018Nabila RosmizaОценок пока нет

- 21 FAR460 SS SET 1 Dec21 Kel - StudentДокумент9 страниц21 FAR460 SS SET 1 Dec21 Kel - StudentRuzaikha razaliОценок пока нет

- Fog ComputingДокумент301 страницаFog Computingorhema oluga100% (2)

- Exercise On Csopl - Associates Ruby Jade Topaz PDFДокумент2 страницыExercise On Csopl - Associates Ruby Jade Topaz PDFNoor ShukirrahОценок пока нет

- Bkas 2013 - Revision Set Suggested SolutionДокумент8 страницBkas 2013 - Revision Set Suggested SolutionsyuhunniepieОценок пока нет

- Universiti Teknologi Mara Suggested Solution For Students Common Test 1Документ5 страницUniversiti Teknologi Mara Suggested Solution For Students Common Test 1Nabila RosmizaОценок пока нет

- Maf 451 - Suggested Solutions: (A) Statement of Equivalent UnitsДокумент7 страницMaf 451 - Suggested Solutions: (A) Statement of Equivalent Unitsanis izzatiОценок пока нет

- QMT425 - Assignment 1Документ5 страницQMT425 - Assignment 1Azwan AyopОценок пока нет

- A191 Mini Case Ppe QuestionДокумент4 страницыA191 Mini Case Ppe Questiondini sofiaОценок пока нет

- 3.2 Mat112 Markup and Markdown Answer SchemeДокумент5 страниц3.2 Mat112 Markup and Markdown Answer SchemeNisha CDОценок пока нет

- Assignment 1Документ4 страницыAssignment 1Yean Liew33% (3)

- Tutorial Pengekosan KeluaranДокумент13 страницTutorial Pengekosan KeluaranatehanaОценок пока нет

- Solution Jan 2018Документ8 страницSolution Jan 2018anis izzatiОценок пока нет

- Maf151 Chapter 2Документ17 страницMaf151 Chapter 2Aiman Zikry bin AzmiОценок пока нет

- Solution Far560 - Jun 2015 (S)Документ7 страницSolution Far560 - Jun 2015 (S)MUHAMAD MUKHAIRI MUHAMAD HANIFAHОценок пока нет

- FAFДокумент8 страницFAFShaminiОценок пока нет

- GROUP 1 TAX INCENTIVES (HOTEL & TOURISM) EditedДокумент20 страницGROUP 1 TAX INCENTIVES (HOTEL & TOURISM) Editedmeera yusufОценок пока нет

- Answer Tax317 Scheme July 2022Документ10 страницAnswer Tax317 Scheme July 2022Kirei RoseОценок пока нет

- Capital Allowance 2220Документ58 страницCapital Allowance 2220YanPing AngОценок пока нет

- Tax Q&A - Income From Investment and Other SourcesДокумент3 страницыTax Q&A - Income From Investment and Other SourcesHadifliОценок пока нет

- Questions Level 2 Series 2006 3Документ4 страницыQuestions Level 2 Series 2006 3Ppii FfrtrОценок пока нет

- Solutions Manual: Elements of CostsДокумент6 страницSolutions Manual: Elements of CostsNed Neddy NeddieОценок пока нет

- Tutorial 3 MFRS111 Construction ContractДокумент9 страницTutorial 3 MFRS111 Construction Contractnatasha thaiОценок пока нет

- Topic 1: Cost-Volume-Profit (CVP) Analysis Exercise 1: BKAM3023 Management Accounting IIДокумент4 страницыTopic 1: Cost-Volume-Profit (CVP) Analysis Exercise 1: BKAM3023 Management Accounting IINur WahidaОценок пока нет

- Question Bank Paper: Cost Accounting McqsДокумент8 страницQuestion Bank Paper: Cost Accounting McqsNikhilОценок пока нет

- Mini Case 4-Investment Property (Student) - A192Документ2 страницыMini Case 4-Investment Property (Student) - A192Chee Mei JeeОценок пока нет

- Chapter 22 Partnership Changes Q1 Wilson, Keppel and BettyДокумент2 страницыChapter 22 Partnership Changes Q1 Wilson, Keppel and Bettymelody shayanwakoОценок пока нет

- Solution Tax667 - Dec 2016Документ7 страницSolution Tax667 - Dec 2016Zahiratul QamarinaОценок пока нет

- Relevant CostДокумент19 страницRelevant CostWanIzyanОценок пока нет

- Solution Maf 635 Dec 2014Документ8 страницSolution Maf 635 Dec 2014anis izzatiОценок пока нет

- Guidelines International Human Resource ManagementДокумент5 страницGuidelines International Human Resource ManagementMohd FadzlyОценок пока нет

- Acc 116 - Chap 1Документ12 страницAcc 116 - Chap 1Azlie ArzimiОценок пока нет

- Tax 3 RevisionДокумент10 страницTax 3 RevisionSoon Mei QiОценок пока нет

- Role Play 20204 - Fin242Документ2 страницыRole Play 20204 - Fin242Muhd Arreif Mohd AzzarainОценок пока нет

- Bmac5203 Accounting For Business Decision Making Rosehamidi KamaruddinДокумент24 страницыBmac5203 Accounting For Business Decision Making Rosehamidi KamaruddinKateryna TernovaОценок пока нет

- 4.4 Solution Maf653 - Jan 2018Документ7 страниц4.4 Solution Maf653 - Jan 2018Arfah Hanum II0% (1)

- Aud589 Dec2019Документ6 страницAud589 Dec2019LANGITBIRU0% (1)

- Tutorial 3Документ6 страницTutorial 3Mastura Abd Hamid100% (1)

- Lesson 9 Problems of Transfer Pricing Practical ExerciseДокумент6 страницLesson 9 Problems of Transfer Pricing Practical ExerciseMadhu kumarОценок пока нет

- FAR270 - FEB 2022 SolutionДокумент8 страницFAR270 - FEB 2022 SolutionNur Fatin AmirahОценок пока нет

- Tutorial 2 Capital Allowances - Q&AДокумент8 страницTutorial 2 Capital Allowances - Q&AKamal JabriОценок пока нет

- A222-Bkar1013 - Chapter 2 - Exercise: Bella Fashion Center Trail Balance November 30, 2015Документ1 страницаA222-Bkar1013 - Chapter 2 - Exercise: Bella Fashion Center Trail Balance November 30, 2015Adelene NengОценок пока нет

- Tutorial 3 MFRS 116 QДокумент15 страницTutorial 3 MFRS 116 QN FrzanahОценок пока нет

- Test Aud 689 - Apr 2018Документ3 страницыTest Aud 689 - Apr 2018Nur Dina AbsbОценок пока нет

- Solution Far610 - Jan 2018Документ10 страницSolution Far610 - Jan 2018E-cHa PineappleОценок пока нет

- FINANCE Group Assignment (28-June-2023)Документ18 страницFINANCE Group Assignment (28-June-2023)Angelyn ChanОценок пока нет

- CIMA Process Costing Sum and AnswersДокумент4 страницыCIMA Process Costing Sum and AnswersLasantha PradeepОценок пока нет

- Solutions Manual: Raw Material and Store OrganizationДокумент5 страницSolutions Manual: Raw Material and Store OrganizationNed Neddy NeddieОценок пока нет

- Chapter 1 - MFRS 116Документ60 страницChapter 1 - MFRS 116Muhammad HazlamiОценок пока нет

- Far270 - Q Test May 2023Документ5 страницFar270 - Q Test May 20232022896776Оценок пока нет

- MINI-CASE 3 Intangible Assets AnswerДокумент5 страницMINI-CASE 3 Intangible Assets Answeryu choongОценок пока нет

- Depreciation (110,500 20%) 21,780 Depreciation (3,660 10%) 366Документ1 страницаDepreciation (110,500 20%) 21,780 Depreciation (3,660 10%) 366Ali MohamedОценок пока нет

- Chapter 3 - Agriculture AllowancesДокумент3 страницыChapter 3 - Agriculture AllowancesNURKHAIRUNNISA100% (2)

- Group Assignment (Problem Based Learning - Set F) : Pma1113 Introducting To Cost & Management AccountingДокумент7 страницGroup Assignment (Problem Based Learning - Set F) : Pma1113 Introducting To Cost & Management AccountingSyamala 29Оценок пока нет

- 64 YanongДокумент25 страниц64 Yanong嘉慧Оценок пока нет

- Planning Function of ManagementДокумент3 страницыPlanning Function of ManagementShah MirОценок пока нет

- 3 - MAF603 - Efficient Market HypothesisДокумент26 страниц3 - MAF603 - Efficient Market HypothesisWan WanОценок пока нет

- June 15 AДокумент8 страницJune 15 ANur Aisyah FaqihahОценок пока нет

- Tutorial 5 Absorption Costing and Marginal Costing Q N A PDFДокумент16 страницTutorial 5 Absorption Costing and Marginal Costing Q N A PDFFatin AdlinaОценок пока нет

- BAC1054 Assigment 1Документ4 страницыBAC1054 Assigment 1N GunasekaramОценок пока нет

- Scanned DocumentsДокумент23 страницыScanned DocumentsTeh Chu LeongОценок пока нет

- Scanned DocumentsДокумент17 страницScanned DocumentsTeh Chu LeongОценок пока нет

- Scanned DocumentsДокумент6 страницScanned DocumentsTeh Chu LeongОценок пока нет

- Characteristics 特征 请列出reptile的2个特征Документ2 страницыCharacteristics 特征 请列出reptile的2个特征Teh Chu LeongОценок пока нет

- CamScanner 09-07-2021 23.11Документ14 страницCamScanner 09-07-2021 23.11Teh Chu LeongОценок пока нет

- Scanned DocumentsДокумент19 страницScanned DocumentsTeh Chu LeongОценок пока нет

- CamScanner 09-09-2021 22.20Документ14 страницCamScanner 09-09-2021 22.20Teh Chu LeongОценок пока нет

- F3 Chapter 9 & 10Документ2 страницыF3 Chapter 9 & 10Teh Chu LeongОценок пока нет

- Vocabulary 词汇 Kosa KataДокумент1 страницаVocabulary 词汇 Kosa KataTeh Chu LeongОценок пока нет

- CamScanner 09-06-2021 22.29Документ14 страницCamScanner 09-06-2021 22.29Teh Chu LeongОценок пока нет

- Geografi Ting. 2 Praktis 2 Peta TopografiДокумент7 страницGeografi Ting. 2 Praktis 2 Peta TopografiTeh Chu LeongОценок пока нет

- Form 3 Chapter 5 ThermochemistryДокумент1 страницаForm 3 Chapter 5 ThermochemistryTeh Chu LeongОценок пока нет

- Science F1C3Документ8 страницScience F1C3Teh Chu LeongОценок пока нет

- CamScanner 09-01-2021 21.45Документ14 страницCamScanner 09-01-2021 21.45Teh Chu LeongОценок пока нет

- Form 1 Chapter 4 ReproductionДокумент7 страницForm 1 Chapter 4 ReproductionTeh Chu LeongОценок пока нет

- Cont Chapter 1Документ2 страницыCont Chapter 1Teh Chu LeongОценок пока нет

- Cont. Chapter 2Документ1 страницаCont. Chapter 2Teh Chu LeongОценок пока нет

- Capitalallowances 1Документ29 страницCapitalallowances 1Teh Chu LeongОценок пока нет

- Employment Income - Derivation, Exemptions, Types and DeductionsДокумент57 страницEmployment Income - Derivation, Exemptions, Types and DeductionsTeh Chu Leong100% (1)

- Chapter 4 PolygonДокумент1 страницаChapter 4 PolygonTeh Chu LeongОценок пока нет

- Topic 2 Resident Status For IndividualДокумент23 страницыTopic 2 Resident Status For IndividualTeh Chu LeongОценок пока нет

- Capitalallowances 2Документ13 страницCapitalallowances 2Teh Chu LeongОценок пока нет

- Chapter 3 Algebraic FormulaeДокумент1 страницаChapter 3 Algebraic FormulaeTeh Chu LeongОценок пока нет

- 34 PERCUBAAN SAINS PT3 + S JWP (MINDA BH) PDFДокумент8 страниц34 PERCUBAAN SAINS PT3 + S JWP (MINDA BH) PDFTeh Chu LeongОценок пока нет

- Strategic Management ProcessДокумент18 страницStrategic Management ProcessNo Mi ViОценок пока нет

- Section A/ Bahagian A (20 Marks/Markah) : TingkatanДокумент18 страницSection A/ Bahagian A (20 Marks/Markah) : TingkatanSong Sing LikОценок пока нет

- Pages From Dr. Shamsuddin L. Taya, Prof Madya Dr. Ariffin S.M. Omar & Prof Madya Dr. Veit Jan Nicol Stark 02Документ2 страницыPages From Dr. Shamsuddin L. Taya, Prof Madya Dr. Ariffin S.M. Omar & Prof Madya Dr. Veit Jan Nicol Stark 02Teh Chu LeongОценок пока нет

- Hidden Firestation Pix PDFДокумент2 страницыHidden Firestation Pix PDFWhy ZuuОценок пока нет

- Rencana Bisnis Art Box Creative and Coworking SpaceДокумент2 страницыRencana Bisnis Art Box Creative and Coworking SpacesupadiОценок пока нет

- Infograpify PowerPointДокумент12 страницInfograpify PowerPointShahan ShakeelОценок пока нет

- IA GuidelinesДокумент23 страницыIA GuidelinesNguyen Vu DuyОценок пока нет

- Ici India Limited: Buy Back of SharesДокумент11 страницIci India Limited: Buy Back of SharesyatinОценок пока нет

- MoaДокумент5 страницMoaRaghvirОценок пока нет

- Sip ReportДокумент66 страницSip ReportOmkar ParabОценок пока нет

- Management QuizzДокумент41 страницаManagement QuizzAakash BhatiaОценок пока нет

- Individual Assignment 26june 2017Документ6 страницIndividual Assignment 26june 2017Eileen OngОценок пока нет

- Industrial Development in Nepal (Final)Документ4 страницыIndustrial Development in Nepal (Final)susmritiОценок пока нет

- Tcs BpsoverviewДокумент25 страницTcs BpsoverviewArockia RajОценок пока нет

- MaricoДокумент23 страницыMaricopompresntОценок пока нет

- Od 226140783550530000Документ2 страницыOd 226140783550530000ayushi pandeyОценок пока нет

- Risk Assesment FormatДокумент2 страницыRisk Assesment FormatThumbanОценок пока нет

- IPL BouncerДокумент31 страницаIPL BouncerNCS FreeОценок пока нет

- Share Khan LimitedДокумент96 страницShare Khan LimitedMayur PrajapatiОценок пока нет

- Unit 4 URBAN PLANING AND URBAN RENEWALДокумент32 страницыUnit 4 URBAN PLANING AND URBAN RENEWALVARSHINIОценок пока нет

- Holyoke Firefighter Arbitration RulingДокумент39 страницHolyoke Firefighter Arbitration RulingTodd AvilaОценок пока нет

- Safa Edited4Документ17 страницSafa Edited4Stoic_SpartanОценок пока нет

- Notice: Self-Regulatory Organizations Proposed Rule Changes: LG&E Energy Corp. Et Al.Документ2 страницыNotice: Self-Regulatory Organizations Proposed Rule Changes: LG&E Energy Corp. Et Al.Justia.comОценок пока нет

- Quotation of Nile MiningДокумент7 страницQuotation of Nile MiningOscarОценок пока нет

- Formula SheetДокумент2 страницыFormula SheetsaiОценок пока нет

- K2.Inc Is Now BruvitiДокумент2 страницыK2.Inc Is Now BruvitiPR.comОценок пока нет

- Presented By: Namrata Singh Samiksha Sahej Grover Sonal MidhaДокумент35 страницPresented By: Namrata Singh Samiksha Sahej Grover Sonal MidhaYatin ChopraОценок пока нет

- Portfolio October To December 2011Документ89 страницPortfolio October To December 2011rishad30Оценок пока нет