Вам также может понравиться

- Guidote v. BorjaДокумент1 страницаGuidote v. Borjatemporiari100% (2)

- PO YENG CHEO and GuidoteДокумент7 страницPO YENG CHEO and GuidoteGorgeousEОценок пока нет

- Guidote Vs BorjaДокумент2 страницыGuidote Vs BorjaRealKD30100% (1)

- Guidote v. BorjaДокумент5 страницGuidote v. BorjaTogz MapeОценок пока нет

- Maximo V. Romana Borja 53 Phil 900 FactsДокумент1 страницаMaximo V. Romana Borja 53 Phil 900 FactsjanelizОценок пока нет

- Guidote - v. - Borja20210511-12-1rmbhДокумент5 страницGuidote - v. - Borja20210511-12-1rmbhRay MaysОценок пока нет

- Guidote v. Borja (Surviving Parters Are TRUSTEES of Deceased's Legal Reps Liquidation Is ENTRUSTED by LAW To SURVIVING PARTNERS)Документ5 страницGuidote v. Borja (Surviving Parters Are TRUSTEES of Deceased's Legal Reps Liquidation Is ENTRUSTED by LAW To SURVIVING PARTNERS)kjhenyo2185020% (1)

- Guidote vs. Borja - 53 Phil 900 - G.R. No. L-28920 - October 24, 1928Документ4 страницыGuidote vs. Borja - 53 Phil 900 - G.R. No. L-28920 - October 24, 1928Ma AleОценок пока нет

- Guidote vs. BorjaДокумент6 страницGuidote vs. BorjaHyacinthОценок пока нет

- PAT - 71 Guidote V BorjaДокумент2 страницыPAT - 71 Guidote V BorjaAndrea TiuОценок пока нет

- Partnership Dec 17Документ90 страницPartnership Dec 17Jo LazanasОценок пока нет

- G.R. No. 2484 Fortis v. HermanosДокумент4 страницыG.R. No. 2484 Fortis v. HermanosAngie Doreen KhoОценок пока нет

- G.R. No. L-25532 February 28, 1969 Commissioner of Internal RevenueДокумент27 страницG.R. No. L-25532 February 28, 1969 Commissioner of Internal RevenueJasmine JagunapQОценок пока нет

- Partnership Case Digest CompilationДокумент12 страницPartnership Case Digest CompilationTonifranz Sareno50% (4)

- Partnership Dec 17 - DigestДокумент55 страницPartnership Dec 17 - DigestJo LazanasОценок пока нет

- Cases Title IX Partnership General Provisions (1) Art. 1767 1.1 Partnership Defined Evangelista, Et Al vs. CIR Decided 15 October 1957Документ9 страницCases Title IX Partnership General Provisions (1) Art. 1767 1.1 Partnership Defined Evangelista, Et Al vs. CIR Decided 15 October 1957Edward Kenneth Kung100% (1)

- Cir v. Suter 27 Scra 152 (1969)Документ4 страницыCir v. Suter 27 Scra 152 (1969)FranzMordenoОценок пока нет

- Pat General Principles Full Text Copies of CasesДокумент65 страницPat General Principles Full Text Copies of CasesBryan Bab BacongolОценок пока нет

- 134 - Realubit V JasoДокумент2 страницы134 - Realubit V JasoJai HoОценок пока нет

- Driano Buenaventura Y Dezollier vs. Antonio David Y AbelidoДокумент2 страницыDriano Buenaventura Y Dezollier vs. Antonio David Y AbelidoNic NalpenОценок пока нет

- Gipa-Save Ni Ate Sa Ako )Документ85 страницGipa-Save Ni Ate Sa Ako )Joan Szanne PulmonesОценок пока нет

- Fortis Vs Gutierrez Hermanos 6 Phil 100Документ3 страницыFortis Vs Gutierrez Hermanos 6 Phil 100krisninОценок пока нет

- G.R. No 127405Документ2 страницыG.R. No 127405Geraldine TubalОценок пока нет

- 01 Fortis V Gutierrez HermanosДокумент4 страницы01 Fortis V Gutierrez HermanoslawОценок пока нет

- Victor Borge, Sanna Borge, and Danica Enterprises, Inc. v. Commissioner of Internal Revenue, 405 F.2d 673, 2d Cir. (1968)Документ10 страницVictor Borge, Sanna Borge, and Danica Enterprises, Inc. v. Commissioner of Internal Revenue, 405 F.2d 673, 2d Cir. (1968)Scribd Government DocsОценок пока нет

- Fortis vs. HermanosДокумент5 страницFortis vs. HermanosSheila RosetteОценок пока нет

- Law Case DigestedДокумент6 страницLaw Case DigestedLouneth DavidОценок пока нет

- G.R. No. 178782 September 21, 2011 JOSEFINA P. REALUBIT, Petitioner, PROSENCIO D. JASO and EDEN G. JASO, RespondentsДокумент5 страницG.R. No. 178782 September 21, 2011 JOSEFINA P. REALUBIT, Petitioner, PROSENCIO D. JASO and EDEN G. JASO, RespondentsNiehr RheinОценок пока нет

- MAXIMO GUIDOTE vs. ROMANA BORJA 53 PHIL 900 - DigestДокумент1 страницаMAXIMO GUIDOTE vs. ROMANA BORJA 53 PHIL 900 - DigestMichelle LimОценок пока нет

- 1 Fortis vs. Gutierrez HermanosДокумент2 страницы1 Fortis vs. Gutierrez HermanosBluei FaustoОценок пока нет

- De La Rosa Vs Go-Cotay - and - Villareal Vs RamirezДокумент2 страницыDe La Rosa Vs Go-Cotay - and - Villareal Vs RamirezHannah DeskyОценок пока нет

- Partnership Full Text IIДокумент39 страницPartnership Full Text IIMJ CemsОценок пока нет

- Evangelista & Co. vs. SantosДокумент5 страницEvangelista & Co. vs. SantosGracelyn QuigaoОценок пока нет

- Goquiolay Vs SycipДокумент3 страницыGoquiolay Vs SycipPJAОценок пока нет

- Pat Cases 01Документ48 страницPat Cases 01Maria Margaret MacasaetОценок пока нет

- ATP 4 Sancho To MoranДокумент23 страницыATP 4 Sancho To MoranPammyОценок пока нет

- CIR Vs SuterДокумент3 страницыCIR Vs SuterKim Lorenzo CalatravaОценок пока нет

- Realubit Vs JasoДокумент2 страницыRealubit Vs Jasokimberly_lorenzo_3Оценок пока нет

- Case DigestДокумент3 страницыCase DigestRedentor TemanilОценок пока нет

- G.R. No. 3745, October 26, 1907Документ2 страницыG.R. No. 3745, October 26, 1907masterfollowОценок пока нет

- Case DigestДокумент23 страницыCase DigestAphrobit Clo0% (2)

- PAT - 40 Garrido V AsencioДокумент1 страницаPAT - 40 Garrido V AsencioAndrea TiuОценок пока нет

- PAT - 40 Garrido V AsencioДокумент1 страницаPAT - 40 Garrido V AsencioAndrea TiuОценок пока нет

- Bus Org Cases 3 5 6 13Документ5 страницBus Org Cases 3 5 6 13Ana AdolfoОценок пока нет

- CasesДокумент16 страницCasesAliah CyrilОценок пока нет

- PAT DigestДокумент7 страницPAT Digestjames oliverОценок пока нет

- G.R. No. L-25532-CIR vs. SuterДокумент3 страницыG.R. No. L-25532-CIR vs. SuterJoffrey UrianОценок пока нет

- Full TXT Part2Документ203 страницыFull TXT Part2AshAngeLОценок пока нет

- Pat - Fortis Vs GutierrezДокумент2 страницыPat - Fortis Vs GutierrezLorenaОценок пока нет

- Stagg, Mather & Hough v. Sol Luis Descartes, Secretary of The Treasury of Puerto Rico, 244 F.2d 578, 1st Cir. (1957)Документ9 страницStagg, Mather & Hough v. Sol Luis Descartes, Secretary of The Treasury of Puerto Rico, 244 F.2d 578, 1st Cir. (1957)Scribd Government DocsОценок пока нет

- Partnership Dgest 2Документ4 страницыPartnership Dgest 2Maria LigayaОценок пока нет

- Sancho Vs LizaragaДокумент3 страницыSancho Vs LizaragajessapuerinОценок пока нет

- 1st SetДокумент254 страницы1st SetCzara DyОценок пока нет

- PAT Digests 1st SetДокумент109 страницPAT Digests 1st SetIrene CastroОценок пока нет

- Pat DigestsДокумент10 страницPat DigestsAnonymous Exek9bОценок пока нет

- 42-ATP-Sunga-Chan v. Lamberto ChuaДокумент2 страницы42-ATP-Sunga-Chan v. Lamberto ChuaJoesil Dianne SempronОценок пока нет

- Sunga Vs ChuaДокумент2 страницыSunga Vs ChuaOke Haruno100% (1)

- Forming The Partnership DIgestsДокумент2 страницыForming The Partnership DIgestsmelaniem_1Оценок пока нет

- Maximo Guidote V. Romana BorjaДокумент12 страницMaximo Guidote V. Romana BorjaJyrus CimatuОценок пока нет

- Civ 2 Notes - Start To ComplianceДокумент26 страницCiv 2 Notes - Start To ComplianceMitchayОценок пока нет

- Remedial Law NotesДокумент5 страницRemedial Law NotesMitchayОценок пока нет

- Modes - DiscussionДокумент15 страницModes - DiscussionMitchayОценок пока нет

- Course Outline in CIVIL LAW REVIEW 2 May 26 2021Документ22 страницыCourse Outline in CIVIL LAW REVIEW 2 May 26 2021MitchayОценок пока нет

- Civ 2Документ103 страницыCiv 2MitchayОценок пока нет

- Ejercito vs. OrientalДокумент3 страницыEjercito vs. OrientalMitchayОценок пока нет

- Notes On Prac 1Документ14 страницNotes On Prac 1MitchayОценок пока нет

- Sources of ObligationsДокумент35 страницSources of ObligationsMitchayОценок пока нет

- Liga CaseДокумент6 страницLiga CaseMitchayОценок пока нет

- Giving Legal Advice To Children in Conflict With LawДокумент5 страницGiving Legal Advice To Children in Conflict With LawMitchayОценок пока нет

- Villaroel vs. EstradaДокумент9 страницVillaroel vs. EstradaMitchayОценок пока нет

- Annual Income Tax Return: Republic of The Philippines Department of Finance Bureau of Internal RevenueДокумент2 страницыAnnual Income Tax Return: Republic of The Philippines Department of Finance Bureau of Internal RevenueDCОценок пока нет

- Obligations - in GeneralДокумент7 страницObligations - in GeneralMitchayОценок пока нет

- Giving Legal Advice On Cases of Annulment"Документ6 страницGiving Legal Advice On Cases of Annulment"MitchayОценок пока нет

- Villaroel vs. EstradaДокумент9 страницVillaroel vs. EstradaMitchayОценок пока нет

- Rule 16Документ1 страницаRule 16MitchayОценок пока нет

- Judicial AffidavitДокумент4 страницыJudicial AffidavitMitchayОценок пока нет

- Tagapan Cicl PDFДокумент255 страницTagapan Cicl PDFMasacal Suhaib MosaОценок пока нет

- Legal Counseling NotesДокумент1 страницаLegal Counseling NotesMitchayОценок пока нет

- Giving Legal Advice To Children in Conflict With LawДокумент5 страницGiving Legal Advice To Children in Conflict With LawMitchayОценок пока нет

- Obligations - in GeneralДокумент7 страницObligations - in GeneralMitchayОценок пока нет

- Njpe Corpo Notes PDFДокумент126 страницNjpe Corpo Notes PDFBrenPeñarandaОценок пока нет

- MIDTERMSДокумент2 страницыMIDTERMSMitchayОценок пока нет

- Rule 16Документ1 страницаRule 16MitchayОценок пока нет

- Sources of ObligationsДокумент8 страницSources of ObligationsMitchayОценок пока нет

- 2019-Golden Notes-Civil Law PDFДокумент710 страниц2019-Golden Notes-Civil Law PDFErika Angela Galceran95% (21)

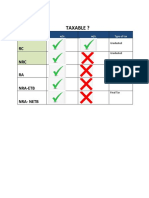

- Taxable ?: RC NRC RAДокумент4 страницыTaxable ?: RC NRC RAMitchayОценок пока нет

- Quiz#1 Partnership 1. True or FalseДокумент3 страницыQuiz#1 Partnership 1. True or FalseMitchayОценок пока нет

- Recit QuestionsДокумент1 страницаRecit QuestionsMitchayОценок пока нет

- Partnership QuestionsДокумент2 страницыPartnership QuestionsMitchayОценок пока нет

- SWOT AnalysisДокумент6 страницSWOT AnalysisSSPK_92Оценок пока нет

- S SSB29 - Alternator Cables PM: WARNING: This Equipment Contains Hazardous VoltagesДокумент3 страницыS SSB29 - Alternator Cables PM: WARNING: This Equipment Contains Hazardous VoltagesMohan PreethОценок пока нет

- Nasoya FoodsДокумент2 страницыNasoya Foodsanamta100% (1)

- Andrews C145385 Shareholders DebriefДокумент9 страницAndrews C145385 Shareholders DebriefmrdlbishtОценок пока нет

- VRIOДокумент3 страницыVRIOJane Apple BulanadiОценок пока нет

- Unit 10-Maintain Knowledge of Improvements To Influence Health and Safety Practice ARДокумент9 страницUnit 10-Maintain Knowledge of Improvements To Influence Health and Safety Practice ARAshraf EL WardajiОценок пока нет

- Prepositions Below by in On To of Above at Between From/toДокумент2 страницыPrepositions Below by in On To of Above at Between From/toVille VianОценок пока нет

- Pyro ShieldДокумент6 страницPyro Shieldmunim87Оценок пока нет

- MOL Breaker 20 TonДокумент1 страницаMOL Breaker 20 Tonaprel jakОценок пока нет

- Tank Emission Calculation FormДокумент12 страницTank Emission Calculation FormOmarTraficanteDelacasitosОценок пока нет

- DC0002A Lhires III Assembling Procedure EnglishДокумент17 страницDC0002A Lhires III Assembling Procedure EnglishНикола ЉубичићОценок пока нет

- VoIP Testing With TEMS InvestigationДокумент20 страницVoIP Testing With TEMS Investigationquantum3510Оценок пока нет

- Hoja Tecnica Item 2 DRC-9-04X12-D-H-D UV BK LSZH - F904804Q6B PDFДокумент2 страницыHoja Tecnica Item 2 DRC-9-04X12-D-H-D UV BK LSZH - F904804Q6B PDFMarco Antonio Gutierrez PulchaОценок пока нет

- RWJ Corp Ch19 Dividends and Other PayoutsДокумент28 страницRWJ Corp Ch19 Dividends and Other Payoutsmuhibbuddin noorОценок пока нет

- Fin 3 - Exam1Документ12 страницFin 3 - Exam1DONNA MAE FUENTESОценок пока нет

- จัดตารางสอบกลางภาคภาคต้น53Документ332 страницыจัดตารางสอบกลางภาคภาคต้น53Yuwarath SuktrakoonОценок пока нет

- Perpetual InjunctionsДокумент28 страницPerpetual InjunctionsShubh MahalwarОценок пока нет

- Statable 1Документ350 страницStatable 1Shelly SantiagoОценок пока нет

- Risk and Uncertainty in Estimating and TenderingДокумент16 страницRisk and Uncertainty in Estimating and TenderingHaneefa ChОценок пока нет

- Project 1. RockCrawlingДокумент2 страницыProject 1. RockCrawlingHằng MinhОценок пока нет

- Mix Cases UploadДокумент4 страницыMix Cases UploadLu CasОценок пока нет

- How To Attain Success Through The Strength of The Vibration of NumbersДокумент95 страницHow To Attain Success Through The Strength of The Vibration of NumberszahkulОценок пока нет

- Two 2 Page Quality ManualДокумент2 страницыTwo 2 Page Quality Manualtony sОценок пока нет

- Province of Camarines Sur vs. CAДокумент8 страницProvince of Camarines Sur vs. CACrisDBОценок пока нет

- POM 3.2 Marketing Management IIДокумент37 страницPOM 3.2 Marketing Management IIDhiraj SharmaОценок пока нет

- Finaniial AsceptsДокумент280 страницFinaniial AsceptsKshipra PrakashОценок пока нет

- INTERNATIONAL BUSINESS DYNAMIC (Global Operation MGT)Документ7 страницINTERNATIONAL BUSINESS DYNAMIC (Global Operation MGT)Shashank DurgeОценок пока нет

- Colibri - DEMSU P01 PDFДокумент15 страницColibri - DEMSU P01 PDFRahul Solanki100% (4)

- CPM W1.1Документ19 страницCPM W1.1HARIJITH K SОценок пока нет

- SyllabusДокумент9 страницSyllabusrr_rroyal550Оценок пока нет