Вам также может понравиться

- GST An UpdateДокумент43 страницыGST An Updatevinod.sale1Оценок пока нет

- GST LawДокумент44 страницыGST LawAniket YTОценок пока нет

- GST - An Update: (As On 01 July 2018)Документ26 страницGST - An Update: (As On 01 July 2018)Jeyakar PrabakarОценок пока нет

- One Nation One TaxДокумент23 страницыOne Nation One TaxSiddhi Hari Krishna GurramОценок пока нет

- Introduction To GST (Final)Документ22 страницыIntroduction To GST (Final)Amit GuptaОценок пока нет

- On GSTДокумент22 страницыOn GSTKumar SumanОценок пока нет

- G.S.T, 15th Finance Commission & Tax Reform by Nihit KishoreДокумент27 страницG.S.T, 15th Finance Commission & Tax Reform by Nihit KishoreUPSC UDAANОценок пока нет

- 2006 2009 2011 2014 Aug 2016 March 2017 April 2017 May 2017 Sep 2016Документ17 страниц2006 2009 2011 2014 Aug 2016 March 2017 April 2017 May 2017 Sep 2016shashvatОценок пока нет

- Overview and Features of GST: D.P. Nagendra Kumar Director General, GST Intelligence (South)Документ8 страницOverview and Features of GST: D.P. Nagendra Kumar Director General, GST Intelligence (South)ALL YOU NEEDОценок пока нет

- Goods & Services Tax: Basic UnderstandingДокумент22 страницыGoods & Services Tax: Basic UnderstandingMohd Yousuf MasoodОценок пока нет

- Tax Reforms in The Light of GSTДокумент62 страницыTax Reforms in The Light of GSTDarling SelviОценок пока нет

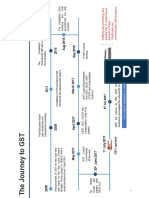

- The Journey To GSTДокумент1 страницаThe Journey To GSTNatSОценок пока нет

- Bos 46137 CP 1Документ36 страницBos 46137 CP 1dharmesh vyasОценок пока нет

- GST IN India - AN: After Studying This Chapter, You Will Be Able ToДокумент42 страницыGST IN India - AN: After Studying This Chapter, You Will Be Able ToPraveen Reddy DevanapalleОценок пока нет

- GST Into1Документ45 страницGST Into1PremОценок пока нет

- Goods and Services TaxДокумент25 страницGoods and Services Taxanuragyadav1611Оценок пока нет

- (DIT) NotesДокумент97 страниц(DIT) NotesArjun SharmaОценок пока нет

- The Reform of Indirect Taxes: by Shivam Roll: 1906581Документ12 страницThe Reform of Indirect Taxes: by Shivam Roll: 1906581Neha agarwalОценок пока нет

- GST 1Документ50 страницGST 1harshini kishore singhОценок пока нет

- Unit-4 Introduction To GSTДокумент15 страницUnit-4 Introduction To GSTSanika DixitОценок пока нет

- GST IN India - AN: Learning OutcomesДокумент1 090 страницGST IN India - AN: Learning OutcomesMayank GargОценок пока нет

- Goods and Service Tax: Unit 2Документ45 страницGoods and Service Tax: Unit 2pradhyumn yadavОценок пока нет

- Introduction To Goods and Services Tax (GST)Документ6 страницIntroduction To Goods and Services Tax (GST)Tax NatureОценок пока нет

- GST - Ready Reckoner - Woorkbook PDFДокумент53 страницыGST - Ready Reckoner - Woorkbook PDFChaitanya NarreddyОценок пока нет

- Introduction To Goods and Services Tax (GST)Документ7 страницIntroduction To Goods and Services Tax (GST)Anjali PawarОценок пока нет

- Indirect Tax 1Документ22 страницыIndirect Tax 1Nmm MitzОценок пока нет

- Implementation of Goods and Services Tax (GST) in IndiaДокумент18 страницImplementation of Goods and Services Tax (GST) in IndiaAkanksha BhattОценок пока нет

- GST NotesДокумент22 страницыGST NotesSARATH BABU.YОценок пока нет

- Indirect Tax and GSTДокумент124 страницыIndirect Tax and GSTPrasanna KumarОценок пока нет

- Taxation Law GST NotesДокумент125 страницTaxation Law GST NotesHasnainОценок пока нет

- GST in IndiaДокумент46 страницGST in IndiaSam RockerОценок пока нет

- Introduction of Goods and Service TaxДокумент12 страницIntroduction of Goods and Service TaxdushyantОценок пока нет

- Study Notes 1Документ10 страницStudy Notes 1Devesh BalodhiОценок пока нет

- GST NotesДокумент47 страницGST NotesChetanya KapoorОценок пока нет

- "Nuances of Indian Taxing Systems": One Day Symposium On TheДокумент20 страниц"Nuances of Indian Taxing Systems": One Day Symposium On TheNasmaОценок пока нет

- GST An IntroductionДокумент4 страницыGST An Introduction9punitagrawalОценок пока нет

- GSTДокумент5 страницGSTAditya KumarОценок пока нет

- Goods and Services Tax - Class 1 - 27 AUGUST 2017: ST NDДокумент5 страницGoods and Services Tax - Class 1 - 27 AUGUST 2017: ST NDNeeraj VОценок пока нет

- GST Definition, Objective, Framework, Action Plan, GST ScopeДокумент8 страницGST Definition, Objective, Framework, Action Plan, GST ScopeKATОценок пока нет

- Unit-1: Introduction and Overview of GST Chapter 1: IntroductionДокумент5 страницUnit-1: Introduction and Overview of GST Chapter 1: IntroductionASHISH LOYAОценок пока нет

- Multi-Stage: Introduction of GSTДокумент4 страницыMulti-Stage: Introduction of GSTHimanshu SinglaОценок пока нет

- Goods and Services Tax (India) : This November Is Wikipedia Asian Month. Join The Contest and Win A Postcard From AsiaДокумент13 страницGoods and Services Tax (India) : This November Is Wikipedia Asian Month. Join The Contest and Win A Postcard From AsiaChander GcОценок пока нет

- Chapter - 1 GST - IntroductionДокумент24 страницыChapter - 1 GST - IntroductionhanumanthaiahgowdaОценок пока нет

- Unit-1: Introduction and Overview of GST Chapter 1: IntroductionДокумент6 страницUnit-1: Introduction and Overview of GST Chapter 1: IntroductionrajneeshkarloopiaОценок пока нет

- Goods and Services Tax Upsc Notes 98Документ5 страницGoods and Services Tax Upsc Notes 98anusreechathoth 1995Оценок пока нет

- Meaning and Introduction of GSTДокумент6 страницMeaning and Introduction of GSTAshish BomzanОценок пока нет

- GST Unit 1Документ23 страницыGST Unit 1hpotter46103Оценок пока нет

- GST ProjectДокумент53 страницыGST Projectafaque khan0% (1)

- PP B Group 4 - GST in LogisticsДокумент7 страницPP B Group 4 - GST in LogisticsSNEHITHA SUNKARAPALLIОценок пока нет

- Taxation Unit-3 and 4Документ38 страницTaxation Unit-3 and 4GITANJALI MISHRAОценок пока нет

- Unit 3 - Indirect Tax Regime - 240324 - 105644Документ53 страницыUnit 3 - Indirect Tax Regime - 240324 - 105644shree varanaОценок пока нет

- GST NotesДокумент18 страницGST NotesNasmaОценок пока нет

- Court MGT ProjectДокумент19 страницCourt MGT ProjectabdullahОценок пока нет

- Basic Concepts and Features of Goods and Service Tax in IndiaДокумент3 страницыBasic Concepts and Features of Goods and Service Tax in Indiamansi nandeОценок пока нет

- Law of Taxation - GST - CapsulsДокумент7 страницLaw of Taxation - GST - Capsulslunavath bittuОценок пока нет

- Assignment Micro EconomicsДокумент28 страницAssignment Micro EconomicsAbdul RehmanОценок пока нет

- Taxation 101 Amendment ActДокумент6 страницTaxation 101 Amendment Actnikitha chowdaryОценок пока нет

- Basics of GST PDFДокумент23 страницыBasics of GST PDFmaxsoniiОценок пока нет

- Unit I GSTДокумент35 страницUnit I GSTPriya DasОценок пока нет

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyОт EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyРейтинг: 5 из 5 звезд5/5 (1)

- Cat Hydo 10wДокумент4 страницыCat Hydo 10wWilbort Encomenderos RuizОценок пока нет

- TTPQДокумент2 страницыTTPQchrystal85Оценок пока нет

- Lifeline® Specialty: Fire Resistant QFCI Cable: Fire Resistant, Flame Retardant Halogen-Free Loose Tube - QFCI/O/RM-JMДокумент2 страницыLifeline® Specialty: Fire Resistant QFCI Cable: Fire Resistant, Flame Retardant Halogen-Free Loose Tube - QFCI/O/RM-JMkevinwz1989Оценок пока нет

- Lindenberg-Anlagen GMBH: Stromerzeugungs-Und Pumpenanlagen SchaltanlagenДокумент10 страницLindenberg-Anlagen GMBH: Stromerzeugungs-Und Pumpenanlagen SchaltanlagenБогдан Кендзер100% (1)

- A - Persuasive TextДокумент15 страницA - Persuasive TextMA. MERCELITA LABUYOОценок пока нет

- PropertycasesforfinalsДокумент40 страницPropertycasesforfinalsRyan Christian LuposОценок пока нет

- Pea RubricДокумент4 страницыPea Rubricapi-297637167Оценок пока нет

- Final Test General English TM 2021Документ2 страницыFinal Test General English TM 2021Nenden FernandesОценок пока нет

- Simplified Electronic Design of The Function : ARMTH Start & Stop SystemДокумент6 страницSimplified Electronic Design of The Function : ARMTH Start & Stop SystembadrОценок пока нет

- The Rise of Political Fact CheckingДокумент17 страницThe Rise of Political Fact CheckingGlennKesslerWPОценок пока нет

- Micro TeachingДокумент3 страницыMicro Teachingapi-273530753Оценок пока нет

- 4Q 4 Embedded SystemsДокумент3 страницы4Q 4 Embedded SystemsJoyce HechanovaОценок пока нет

- Community Service Learning IdeasДокумент4 страницыCommunity Service Learning IdeasMuneeb ZafarОценок пока нет

- Holophane Denver Elite Bollard - Spec Sheet - AUG2022Документ3 страницыHolophane Denver Elite Bollard - Spec Sheet - AUG2022anamarieОценок пока нет

- Catalogue 2021Документ12 страницCatalogue 2021vatsala36743Оценок пока нет

- Positive Accounting TheoryДокумент47 страницPositive Accounting TheoryAshraf Uz ZamanОценок пока нет

- 44) Year 4 Preposition of TimeДокумент1 страница44) Year 4 Preposition of TimeMUHAMMAD NAIM BIN RAMLI KPM-GuruОценок пока нет

- Spice Processing UnitДокумент3 страницыSpice Processing UnitKSHETRIMAYUM MONIKA DEVIОценок пока нет

- Science Technology and SocietyДокумент46 страницScience Technology and SocietyCharles Elquime GalaponОценок пока нет

- Hankinson - Location Branding - A Study of The Branding Practices of 12 English CitiesДокумент16 страницHankinson - Location Branding - A Study of The Branding Practices of 12 English CitiesNatalia Ney100% (1)

- Semiotics Study of Movie ShrekДокумент15 страницSemiotics Study of Movie Shreky2pinku100% (1)

- Manalili v. CA PDFДокумент3 страницыManalili v. CA PDFKJPL_1987100% (1)

- Post Cold WarДокумент70 страницPost Cold WarZainab WaqarОценок пока нет

- Mohak Meaning in Urdu - Google SearchДокумент1 страницаMohak Meaning in Urdu - Google SearchShaheryar AsgharОценок пока нет

- Quiz 07Документ15 страницQuiz 07Ije Love100% (1)

- Grope Assignment 1Документ5 страницGrope Assignment 1SELAM AОценок пока нет

- Military - British Army - Clothing & Badges of RankДокумент47 страницMilitary - British Army - Clothing & Badges of RankThe 18th Century Material Culture Resource Center94% (16)

- Lecture 4 PDFДокумент9 страницLecture 4 PDFVarun SinghalОценок пока нет

- Eradication, Control and Monitoring Programmes To Contain Animal DiseasesДокумент52 страницыEradication, Control and Monitoring Programmes To Contain Animal DiseasesMegersaОценок пока нет

- Iluminadores y DipolosДокумент9 страницIluminadores y DipolosRamonОценок пока нет