Вам также может понравиться

- 0 - 3. Time DepositДокумент19 страниц0 - 3. Time DepositGus CahОценок пока нет

- INTRODUCTION TO BUSINESS Meeting 6Документ33 страницыINTRODUCTION TO BUSINESS Meeting 6Gus CahОценок пока нет

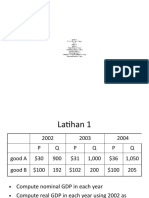

- Latihan Hitung GDPДокумент9 страницLatihan Hitung GDPGus CahОценок пока нет

- Latihan Hitung GDPДокумент9 страницLatihan Hitung GDPGus CahОценок пока нет

- 12c Tradeoff Inflation UnemploymentДокумент6 страниц12c Tradeoff Inflation UnemploymentGus CahОценок пока нет

- 12c Tradeoff Inflation UnemploymentДокумент6 страниц12c Tradeoff Inflation UnemploymentGus CahОценок пока нет

- 09a Production GrowthДокумент8 страниц09a Production GrowthGus CahОценок пока нет

- 02a Market ForcesДокумент10 страниц02a Market ForcesGus CahОценок пока нет

- Economy. - .: Ten Principles of EconomicsДокумент7 страницEconomy. - .: Ten Principles of EconomicsGus CahОценок пока нет

- Between Monopoly and Perfect Competition: OligopolyДокумент7 страницBetween Monopoly and Perfect Competition: OligopolyGus CahОценок пока нет

- 03a Supply Demand GovДокумент6 страниц03a Supply Demand GovGus CahОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Moral IssuesДокумент34 страницыMoral IssuesDaryll Jade PoscabloОценок пока нет

- Psar Techspec Autologicsoftwaretechspecfor Psarvehicles en PF v2.0Документ183 страницыPsar Techspec Autologicsoftwaretechspecfor Psarvehicles en PF v2.0PhatОценок пока нет

- FM Solved ProblemsДокумент28 страницFM Solved ProblemsElisten DabreoОценок пока нет

- Project Execution and Control: Lunar International College July, 2021Документ35 страницProject Execution and Control: Lunar International College July, 2021getahun tesfayeОценок пока нет

- Lesson 12: Parallel Transformers and Autotransformers: Learning ObjectivesДокумент13 страницLesson 12: Parallel Transformers and Autotransformers: Learning ObjectivesRookie Thursday OrquiaОценок пока нет

- Towards Improvement of The Rights and Duties of Mutawalli and Nazir in The Management And..Документ17 страницTowards Improvement of The Rights and Duties of Mutawalli and Nazir in The Management And..Mutqinah SshiОценок пока нет

- Incorporation of Industrial Wastes As Raw Materials in Brick's Formulation (Wiemes-Brasil-2016)Документ9 страницIncorporation of Industrial Wastes As Raw Materials in Brick's Formulation (Wiemes-Brasil-2016)juan diazОценок пока нет

- Toyota PDFДокумент3 страницыToyota PDFPushp ToshniwalОценок пока нет

- DAR Vol1-2013Документ744 страницыDAR Vol1-2013chitransh2002Оценок пока нет

- Topic 7Документ18 страницTopic 7Anonymous 0fCNL9T0Оценок пока нет

- Full Download Test Bank For Managerial Decision Modeling With Spreadsheets 3rd Edition by Balakrishnan PDF Full ChapterДокумент36 страницFull Download Test Bank For Managerial Decision Modeling With Spreadsheets 3rd Edition by Balakrishnan PDF Full Chapterhospital.epical.x6uu100% (20)

- Arbitrage Calculator 3Документ4 страницыArbitrage Calculator 3Eduardo MontanhaОценок пока нет

- Doctrine of Indoor ManagementДокумент4 страницыDoctrine of Indoor ManagementRavi KtОценок пока нет

- Ec8691 MPMC Question BankДокумент41 страницаEc8691 MPMC Question BankManimegalaiОценок пока нет

- Writing NuocRut Ver02Документ118 страницWriting NuocRut Ver02thuy linhОценок пока нет

- DQI and Use Mentors JDДокумент2 страницыDQI and Use Mentors JDLunaltОценок пока нет

- Smart Phone Usage Among College Going StudentsДокумент9 страницSmart Phone Usage Among College Going StudentsAkxzОценок пока нет

- Thermister O Levels Typical QuestionДокумент4 страницыThermister O Levels Typical QuestionMohammad Irfan YousufОценок пока нет

- Lululemon Sample Case AnalysisДокумент49 страницLululemon Sample Case AnalysisMai Ngoc PhamОценок пока нет

- 1.doosan D1146Документ1 страница1.doosan D1146Md. ShohelОценок пока нет

- NEBOSH IGC IG1 Course NotesДокумент165 страницNEBOSH IGC IG1 Course NotesShagufta Mallick100% (13)

- Installation Instructions: LRM1070, LRM1080Документ2 страницыInstallation Instructions: LRM1070, LRM1080Stefan JovanovicОценок пока нет

- Assignment 2Документ4 страницыAssignment 2LaDonna WhiteОценок пока нет

- The Properties of Chopped Basalt Fibre Reinforced Self-CompactingДокумент8 страницThe Properties of Chopped Basalt Fibre Reinforced Self-CompactingEjaz RahimiОценок пока нет

- Solar Electrical Safety Presentation 1PDFДокумент34 страницыSolar Electrical Safety Presentation 1PDFblueboyОценок пока нет

- Crisostomo Vs Courts of Appeal G.R. No. 138334 August 25, 2003Документ5 страницCrisostomo Vs Courts of Appeal G.R. No. 138334 August 25, 2003RGIQОценок пока нет

- 1st Activity in EthicsДокумент2 страницы1st Activity in EthicsAleiah Jane Valencia AlverioОценок пока нет

- 7 Hive NotesДокумент36 страниц7 Hive NotesSandeep BoyinaОценок пока нет

- LC1D40008B7: Product Data SheetДокумент4 страницыLC1D40008B7: Product Data SheetLê Duy MinhОценок пока нет

- 02 IG4K TechnologiesДокумент47 страниц02 IG4K TechnologiesM Tanvir AnwarОценок пока нет