Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- General Electric Management AnalysisДокумент20 страницGeneral Electric Management AnalysisNehal NabilОценок пока нет

- 2009-12-13 035229 ShelbyДокумент1 страница2009-12-13 035229 Shelbydineshmech225Оценок пока нет

- QA Lecture 1Документ34 страницыQA Lecture 1Ahmed HusseinОценок пока нет

- Change Management and ResistanceДокумент5 страницChange Management and ResistanceNehal NabilОценок пока нет

- Chapter 6 - Anchoring BiasДокумент18 страницChapter 6 - Anchoring BiasNehal NabilОценок пока нет

- Date: Monday 19/5/2015: Strategic Management Year 2015 Final ExamДокумент6 страницDate: Monday 19/5/2015: Strategic Management Year 2015 Final ExamNehal NabilОценок пока нет

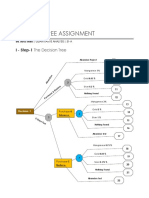

- Decision Tree Assignment: Supervised By: Dr. Adel Sakr Introduced By: Nehal Nabil Abd AlzaherДокумент3 страницыDecision Tree Assignment: Supervised By: Dr. Adel Sakr Introduced By: Nehal Nabil Abd AlzaherNehal NabilОценок пока нет

- Mid Term Problem 1 & 2-1 - 54877 PDFДокумент2 страницыMid Term Problem 1 & 2-1 - 54877 PDFNehal NabilОценок пока нет

- Addressing CompetitiveДокумент17 страницAddressing CompetitiveNehal Nabil100% (1)

- NotesДокумент1 страницаNotesNehal NabilОценок пока нет

- Decision Tree Assignment QAДокумент5 страницDecision Tree Assignment QANehal NabilОценок пока нет

- What Are The Main Steps of Quantitative Analysis?Документ9 страницWhat Are The Main Steps of Quantitative Analysis?Nehal NabilОценок пока нет

- Mid Term Problem 1 & 2-1-54877Документ2 страницыMid Term Problem 1 & 2-1-54877Nehal NabilОценок пока нет

- AccountingДокумент20 страницAccountingNehal NabilОценок пока нет

- The Case For Enterprise-Ready Virtual Private CloudsДокумент5 страницThe Case For Enterprise-Ready Virtual Private CloudsNehal NabilОценок пока нет

- Time Value of Money TablesДокумент12 страницTime Value of Money TablesHananAhmedОценок пока нет

- Specialized Training Program in Big Data AnalyticsДокумент3 страницыSpecialized Training Program in Big Data AnalyticsNehal NabilОценок пока нет

- Project: E-Guard Professor Dr. Ahmed FouadДокумент23 страницыProject: E-Guard Professor Dr. Ahmed FouadNehal NabilОценок пока нет

- 14 Financial Statement Analysis: Chapter SummaryДокумент12 страниц14 Financial Statement Analysis: Chapter SummaryGeoffrey Rainier CartagenaОценок пока нет

- 10 Cases Accounting - Answered-1 PDFДокумент10 страниц10 Cases Accounting - Answered-1 PDFNehal NabilОценок пока нет

- Academic Writing - Assessment SchemeДокумент2 страницыAcademic Writing - Assessment SchemeNehal NabilОценок пока нет

- Business Research Method Question and AnswersДокумент15 страницBusiness Research Method Question and AnswersNehal NabilОценок пока нет

- Academic Writing - Complete OutlineДокумент3 страницыAcademic Writing - Complete OutlineNehal NabilОценок пока нет

- Business Research Method Question and AnswersДокумент16 страницBusiness Research Method Question and AnswersEthiria Cera Faith73% (11)

- Nahavandi Leadership6 Tif Ch05Документ16 страницNahavandi Leadership6 Tif Ch05Antony Gamal100% (8)

- 01 - Project ManagementДокумент12 страниц01 - Project ManagementNehal NabilОценок пока нет

- Chapter1-Carter Cleaning Centers PDFДокумент4 страницыChapter1-Carter Cleaning Centers PDFNehal NabilОценок пока нет

- Chapter 1Документ8 страницChapter 1Nehal NabilОценок пока нет

- Consider The Following Network: (P6) (Times Are in Weeks)Документ1 страницаConsider The Following Network: (P6) (Times Are in Weeks)Nehal NabilОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Note6.1 Mathematics of Finance (1) Compound Interests PDFДокумент23 страницыNote6.1 Mathematics of Finance (1) Compound Interests PDF李华夏Оценок пока нет

- FIN F311 - Derivative and Risk Management (2) - CMSДокумент6 страницFIN F311 - Derivative and Risk Management (2) - CMSSaksham GoyalОценок пока нет

- Jnu Answer KeyДокумент15 страницJnu Answer Keykshitij singh rathore0% (1)

- IFM Question Bank Solved FinalДокумент34 страницыIFM Question Bank Solved FinalRavindra BabuОценок пока нет

- Derivatives: Forward ContractsДокумент4 страницыDerivatives: Forward ContractsSAITEJA DASARIОценок пока нет

- Ema Ge Berk CF 2GE SG 22Документ15 страницEma Ge Berk CF 2GE SG 22080395Оценок пока нет

- Topic 3 For Students International ParityДокумент71 страницаTopic 3 For Students International Paritywanimtiaz9150Оценок пока нет

- Vodafone Group PLC H1 Report (2011)Документ42 страницыVodafone Group PLC H1 Report (2011)RCR Wireless News IndiaОценок пока нет

- Fma401v Tutorial101Документ40 страницFma401v Tutorial101darl1Оценок пока нет

- SwapsДокумент60 страницSwapsHarpreet AujlaОценок пока нет

- LBS FD AssignmentДокумент3 страницыLBS FD AssignmentSarah CarterОценок пока нет

- C4 Final Assignment v2Документ43 страницыC4 Final Assignment v2Lan Chau100% (1)

- Barney Smca6 PPT 06Документ20 страницBarney Smca6 PPT 06HagarMahmoudОценок пока нет

- Understanding Fixed Income Risk & ReturnДокумент26 страницUnderstanding Fixed Income Risk & ReturnAnurag MishraОценок пока нет

- Cashflows PDFДокумент40 страницCashflows PDFABHISHEK RAJОценок пока нет

- Ifm Primer Part OneДокумент13 страницIfm Primer Part OnefinervaОценок пока нет

- TMV Practice Questions SolutionsДокумент20 страницTMV Practice Questions SolutionsSnehОценок пока нет

- Masterunit 3 FRMДокумент99 страницMasterunit 3 FRMChham Chha Virak VccОценок пока нет

- Time Value of MoneyДокумент42 страницыTime Value of MoneyCatalan MelodyОценок пока нет

- Dec 2002 - Qns Mod BДокумент14 страницDec 2002 - Qns Mod BHubbak Khan100% (1)

- NRI BankingДокумент62 страницыNRI Bankingहर्ष मोहन100% (1)

- EC102 Exam 2009Документ25 страницEC102 Exam 2009ac2718Оценок пока нет

- Keynes and NKEДокумент33 страницыKeynes and NKESamuel Seyi OmoleyeОценок пока нет

- HuewwwДокумент20 страницHuewwwWex Senin AlcantaraОценок пока нет

- Volume 4 Derivatives IRRM & RMДокумент168 страницVolume 4 Derivatives IRRM & RMTejas jogadeОценок пока нет

- Journal of International Economics: Atsushi Inoue, Barbara RossiДокумент29 страницJournal of International Economics: Atsushi Inoue, Barbara Rossinam phanОценок пока нет

- Risk and Return: Past and PrologueДокумент58 страницRisk and Return: Past and Prologueshubham singhОценок пока нет

- Chapter 5: Risk and ReturnДокумент31 страницаChapter 5: Risk and ReturnEyobedОценок пока нет

- R55 Understanding Fixed-Income Risk and Return Q BankДокумент20 страницR55 Understanding Fixed-Income Risk and Return Q BankAhmedОценок пока нет

- The Three Basic Macroeconomics RelationshipДокумент5 страницThe Three Basic Macroeconomics RelationshipNicole Echanes0% (1)