Вам также может понравиться

- Accounting for investmentsДокумент3 страницыAccounting for investmentsCrissette RoslynОценок пока нет

- PC AccountingДокумент15 страницPC AccountingDianne SantiagoОценок пока нет

- CE On Quasi-ReorganizationДокумент1 страницаCE On Quasi-ReorganizationalyssaОценок пока нет

- Partnership Law Review QuestionsДокумент5 страницPartnership Law Review QuestionsBobby Olavides Sebastian0% (1)

- CHAPTER 11 Without AnswerДокумент3 страницыCHAPTER 11 Without Answerlenaka0% (1)

- Book Value and Earnings Per ShareДокумент3 страницыBook Value and Earnings Per ShareAlejandrea LalataОценок пока нет

- Re & BVДокумент3 страницыRe & BV-100% (1)

- COS 103 - Variable Costing ExercisesДокумент2 страницыCOS 103 - Variable Costing ExercisesAivie Pangilinan100% (1)

- Basic accounting for defined benefit plansДокумент23 страницыBasic accounting for defined benefit plansKristine Diane CABAnASОценок пока нет

- FIN 2 Financial Analysis and Reporting: Lyceum-Northwestern UniversityДокумент7 страницFIN 2 Financial Analysis and Reporting: Lyceum-Northwestern UniversityAmie Jane MirandaОценок пока нет

- Quiz - M1 M2Документ12 страницQuiz - M1 M2Jenz Crisha PazОценок пока нет

- Partnership Dissolution: QuizДокумент5 страницPartnership Dissolution: QuizLee SuarezОценок пока нет

- NOTESДокумент53 страницыNOTESirahQОценок пока нет

- Midterm Exam Palapuz, John Mark Bsac 3a 1Документ6 страницMidterm Exam Palapuz, John Mark Bsac 3a 1John Mark PalapuzОценок пока нет

- Adv2 QUIZ3Документ3 страницыAdv2 QUIZ3husney botawanОценок пока нет

- Naqdown - Final QuestionsДокумент41 страницаNaqdown - Final QuestionssarahbeeОценок пока нет

- ACCTGДокумент13 страницACCTGCabardo Maria RegilynОценок пока нет

- Compound Financial Intruments PDFДокумент2 страницыCompound Financial Intruments PDFCeline Marie Libatique AntonioОценок пока нет

- TaxInd P1Документ25 страницTaxInd P1Rael RaelОценок пока нет

- Mostafa Fouda98Документ9 страницMostafa Fouda98deepak1818Оценок пока нет

- Chapter 10 AIS Seatwork Finals Questions PDFДокумент4 страницыChapter 10 AIS Seatwork Finals Questions PDFdesblahОценок пока нет

- First Exam Review WithSolutionДокумент6 страницFirst Exam Review WithSolutionLexter Dave C EstoqueОценок пока нет

- Lemons Problems Arise in Capital Markets WhenДокумент1 страницаLemons Problems Arise in Capital Markets WhenDipak MondalОценок пока нет

- BLR 211 Sacrifice AnswerДокумент19 страницBLR 211 Sacrifice AnswerSherri BonquinОценок пока нет

- UCP: CVP Analysis and ExercisesДокумент10 страницUCP: CVP Analysis and ExercisesDin Rose GonzalesОценок пока нет

- Quiz Week 8 Akm 2Документ6 страницQuiz Week 8 Akm 2Tiara Eva TresnaОценок пока нет

- BA 118.1 SME Exercise Set 5Документ1 страницаBA 118.1 SME Exercise Set 5Ian De DiosОценок пока нет

- 2nd Examination For DistributionДокумент8 страниц2nd Examination For DistributionShibaInu DogeОценок пока нет

- PARTNERSHIP CHARACTERISTICS AND TERMSДокумент74 страницыPARTNERSHIP CHARACTERISTICS AND TERMSLhowellaAquinoОценок пока нет

- Partnership Formation and Operations Exercises and Problems1,670,000518,0001,152,0001,792,000256,000160,000198,000(16,000)(120,000)2,270,000Документ21 страницаPartnership Formation and Operations Exercises and Problems1,670,000518,0001,152,0001,792,000256,000160,000198,000(16,000)(120,000)2,270,000Jayson Villena Malimata100% (2)

- Multiple Choice: Choose The Best Answer Among The Choices. Write Your Answers in CAPITAL Letters. (2 Points Per Requirement)Документ3 страницыMultiple Choice: Choose The Best Answer Among The Choices. Write Your Answers in CAPITAL Letters. (2 Points Per Requirement)Kimmy ShawwyОценок пока нет

- Estate Tax Test BankДокумент38 страницEstate Tax Test BankMario LuigiОценок пока нет

- MAS Handout CH4 DiffCostAnaДокумент2 страницыMAS Handout CH4 DiffCostAnaAbigail TumabaoОценок пока нет

- Chapter 10 PAS 28 INVESTMENT IN ASSOCIATESДокумент2 страницыChapter 10 PAS 28 INVESTMENT IN ASSOCIATESgabriel ramosОценок пока нет

- Act 20-Ap 04 PpeДокумент7 страницAct 20-Ap 04 PpeJomar VillenaОценок пока нет

- Threats To Compliance With The Fundamental PrinciplesДокумент5 страницThreats To Compliance With The Fundamental PrinciplesAbigail SubaОценок пока нет

- Comprehensive Oakwood Inc Is A Public Enterprise Whose Shares AreДокумент1 страницаComprehensive Oakwood Inc Is A Public Enterprise Whose Shares AreTaimur TechnologistОценок пока нет

- SRGGДокумент31 страницаSRGGPinky LongalongОценок пока нет

- Maine Media WorkshopДокумент2 страницыMaine Media WorkshopBOB MARLOWОценок пока нет

- IA2 05 - Handout - 1 PDFДокумент14 страницIA2 05 - Handout - 1 PDFMelchie RepospoloОценок пока нет

- COSTДокумент6 страницCOSTJO SH UAОценок пока нет

- Book Value Per Share Basic Earnings PerДокумент61 страницаBook Value Per Share Basic Earnings Perayagomez100% (1)

- Obligation ObligationДокумент40 страницObligation ObligationRose Bacalso100% (1)

- Our Lady of Fatima UniversityДокумент3 страницыOur Lady of Fatima UniversityJasmine Nouvel Soriaga CruzОценок пока нет

- Practical Accounting Problems SolutionsДокумент11 страницPractical Accounting Problems SolutionsjustjadeОценок пока нет

- QUIZ1PRAC1Документ23 страницыQUIZ1PRAC1Marinel Felipe0% (1)

- Corporation QuizДокумент13 страницCorporation Quizjano_art21Оценок пока нет

- MAS 09 - Quantitative TechniquesДокумент6 страницMAS 09 - Quantitative TechniquesClint Abenoja0% (1)

- Final Practice ExamДокумент15 страницFinal Practice ExamRaymond KeyesОценок пока нет

- Comprehensive QuizДокумент4 страницыComprehensive QuizBea LadaoОценок пока нет

- Valix 2 Chapt 24 25 PDFДокумент20 страницValix 2 Chapt 24 25 PDFivyaguasarnaldo4everОценок пока нет

- Activity Considered Recitation.Документ5 страницActivity Considered Recitation.francis dungcaОценок пока нет

- Pre-Test 11Документ2 страницыPre-Test 11BLACKPINKLisaRoseJisooJennieОценок пока нет

- Pre-Test 12 Solutions and ExplanationsДокумент2 страницыPre-Test 12 Solutions and ExplanationsBLACKPINKLisaRoseJisooJennieОценок пока нет

- ACCExpanded Opportunity Part 1Документ4 страницыACCExpanded Opportunity Part 1Hilarie JeanОценок пока нет

- Compre23 FARДокумент12 страницCompre23 FARchristinemariet.ramirezОценок пока нет

- Ap 9201-2 SheДокумент5 страницAp 9201-2 SheShefannie PaynanteОценок пока нет

- Handout For Acca106/Fmcc212 Final Exam Review Tutor's NotesДокумент12 страницHandout For Acca106/Fmcc212 Final Exam Review Tutor's NotesShaine AndreaОценок пока нет

- ExtAud 3 Quiz 5 Wo AnswersДокумент8 страницExtAud 3 Quiz 5 Wo AnswersJANET ILLESESОценок пока нет

- Module 16 Share-Based PaymentДокумент8 страницModule 16 Share-Based PaymentryanОценок пока нет

- Finance Chapter 3 Questions and Answers Questions Answer RemarksДокумент2 страницыFinance Chapter 3 Questions and Answers Questions Answer RemarksJane T.Оценок пока нет

- Case StudyДокумент5 страницCase StudyJane T.Оценок пока нет

- Commercial Banks: Assets, Fees & Industry TrendsДокумент7 страницCommercial Banks: Assets, Fees & Industry TrendsLevi Emmanuel Veloso BravoОценок пока нет

- PersuasivetextslanguagefeaturesДокумент8 страницPersuasivetextslanguagefeaturesTroy Quinto De GuzmanОценок пока нет

- PackingДокумент1 страницаPackingJane T.Оценок пока нет

- Managing financial risks and credit risk amid the pandemicДокумент1 страницаManaging financial risks and credit risk amid the pandemicJane T.Оценок пока нет

- Financial Institution Risks Management of Risks How Affected by The PandemicДокумент1 страницаFinancial Institution Risks Management of Risks How Affected by The PandemicJane T.Оценок пока нет

- What Is Succession?Документ4 страницыWhat Is Succession?Jane T.Оценок пока нет

- Debt Ratio WordДокумент1 страницаDebt Ratio WordJane T.Оценок пока нет

- Taxation Issues and Benefits of E-Commerce in the PhilippinesДокумент1 страницаTaxation Issues and Benefits of E-Commerce in the PhilippinesJane T.Оценок пока нет

- Financial Institution Risks Management of Risks How Affected by The PandemicДокумент1 страницаFinancial Institution Risks Management of Risks How Affected by The PandemicJane T.Оценок пока нет

- Process Narrative - SOX Project / IT Fixed Assets: PurposeДокумент6 страницProcess Narrative - SOX Project / IT Fixed Assets: PurposeZlatilОценок пока нет

- Mortgage FirmsДокумент1 страницаMortgage FirmsJane T.Оценок пока нет

- Financial Institution Risks Management of Risks How Affected by The Pandemic Credit Union and Finance Company Liquidity RiskДокумент1 страницаFinancial Institution Risks Management of Risks How Affected by The Pandemic Credit Union and Finance Company Liquidity RiskJane T.Оценок пока нет

- ResearchДокумент1 страницаResearchJane T.Оценок пока нет

- Usc Mission-VisionДокумент2 страницыUsc Mission-VisionJane T.Оценок пока нет

- Pink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtДокумент1 страницаPink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtJane T.Оценок пока нет

- Promoting Mental HealthДокумент79 страницPromoting Mental HealthJane T.Оценок пока нет

- Bylaws Non StockДокумент3 страницыBylaws Non StockJane T.Оценок пока нет

- Pink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtДокумент1 страницаPink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtJane T.Оценок пока нет

- Bylaws Non StockДокумент3 страницыBylaws Non StockJane T.Оценок пока нет

- JSM Red Entertainment ArticlesДокумент3 страницыJSM Red Entertainment ArticlesJane T.Оценок пока нет

- Pink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtДокумент1 страницаPink and Red Grid Fashion Influencer Nostalgia Youtube Channel ArtJane T.Оценок пока нет

- WorksheetДокумент1 страницаWorksheetJane T.Оценок пока нет

- RecommendationДокумент13 страницRecommendationJane T.Оценок пока нет

- Purchasing and Receiving Procedure SummaryДокумент1 страницаPurchasing and Receiving Procedure SummaryJane T.Оценок пока нет

- Cash Disbursements Procedure ApДокумент1 страницаCash Disbursements Procedure ApJane T.Оценок пока нет

- Purchasing and Receiving Procedure SummaryДокумент1 страницаPurchasing and Receiving Procedure SummaryJane T.Оценок пока нет

- 20140118053700Документ3 страницы20140118053700Jalal GogginsОценок пока нет

- Process Lists Fico MM SD PP PM CsДокумент20 страницProcess Lists Fico MM SD PP PM CsSubhash Reddy100% (4)

- Input Tax Credit: Understanding the Core Concept of GSTДокумент14 страницInput Tax Credit: Understanding the Core Concept of GSTratna supriyaОценок пока нет

- 30 Transactions With Their Journal EntriesДокумент9 страниц30 Transactions With Their Journal EntriesPrashant BhardwajОценок пока нет

- CrossBorder PaymentsДокумент378 страницCrossBorder PaymentsDewa AsmaraОценок пока нет

- Deed of TrustДокумент19 страницDeed of Trustshakhawat_cОценок пока нет

- Accy111 CVP Questions and AnswersДокумент32 страницыAccy111 CVP Questions and AnswersGurkiran KaurОценок пока нет

- 04 - Cost Accounting by Usry (Part2)Документ3 страницы04 - Cost Accounting by Usry (Part2)AkiОценок пока нет

- Chap 002Документ73 страницыChap 002Tony TaiОценок пока нет

- Account Past Questions Compilation (2009june - 2020 Dec.)Документ246 страницAccount Past Questions Compilation (2009june - 2020 Dec.)Prashant Sagar Gautam100% (2)

- Introduction to Single Entity AccountsДокумент38 страницIntroduction to Single Entity Accountsshrish gupta100% (1)

- Lcci Book Keeping 2008Документ6 страницLcci Book Keeping 2008Jill Priya KeshyapОценок пока нет

- Hire Purchase and Instalment Sale Transactions: Learning ObjectivesДокумент52 страницыHire Purchase and Instalment Sale Transactions: Learning ObjectivesEswari GkОценок пока нет

- Accounts Ques Nov06Документ48 страницAccounts Ques Nov06api-3825774Оценок пока нет

- Chapter 7 CorpoДокумент3 страницыChapter 7 CorpoCesar LegaspiОценок пока нет

- RoundingДокумент65 страницRoundingSourav Kumar100% (1)

- Certified Hospitality Accountant Executive (CHAE) Review Hitec Baltimore, MD June 25, 2012Документ53 страницыCertified Hospitality Accountant Executive (CHAE) Review Hitec Baltimore, MD June 25, 2012nowfazОценок пока нет

- Measuring Business Income AdjustmentsДокумент34 страницыMeasuring Business Income AdjustmentsFaiza ShahОценок пока нет

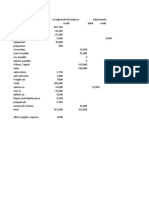

- Maliksi Accounting Services Financial StatementsДокумент8 страницMaliksi Accounting Services Financial StatementsJohn Carldel VivoОценок пока нет

- Disburement Voucher: Division of City SchoolsДокумент4 страницыDisburement Voucher: Division of City SchoolsLiling SirenОценок пока нет

- Prepayments LiabilitesДокумент1 страницаPrepayments LiabilitesKrishele G. GotejerОценок пока нет

- Useful SAP Financial ReportsДокумент2 страницыUseful SAP Financial ReportsfaiqalikhanОценок пока нет

- Cfi Accounting EbookДокумент66 страницCfi Accounting Ebookmanjit13121990Оценок пока нет

- Ipaubaya Computers Manufactures and Sells Pagers and Radio Paging Systems Which Include A 180 Day WaДокумент12 страницIpaubaya Computers Manufactures and Sells Pagers and Radio Paging Systems Which Include A 180 Day WaYukiОценок пока нет

- Tarkington Freight Service Provides Delivery of Merchandise To Retail GroceryДокумент2 страницыTarkington Freight Service Provides Delivery of Merchandise To Retail GroceryTaimur TechnologistОценок пока нет

- AGIS Questions and AnswersДокумент5 страницAGIS Questions and AnswersHimanshu MadanОценок пока нет

- Prelim Exam - AccountingДокумент7 страницPrelim Exam - AccountingAntonia JessaОценок пока нет

- Mba Bdu Concurrent AssignmentДокумент22 страницыMba Bdu Concurrent AssignmentDivniLhlОценок пока нет

- R14 - UG - Retail Murabaha PDFДокумент62 страницыR14 - UG - Retail Murabaha PDFSathya KumarОценок пока нет

- Quiz - Midterm ExaminationДокумент21 страницаQuiz - Midterm Examinationangel caoОценок пока нет