Вам также может понравиться

- ISO 9001:2015 Internal Audits Made Easy: Tools, Techniques, and Step-by-Step Guidelines for Successful Internal AuditsОт EverandISO 9001:2015 Internal Audits Made Easy: Tools, Techniques, and Step-by-Step Guidelines for Successful Internal AuditsОценок пока нет

- Internal Audit EngagementДокумент9 страницInternal Audit EngagementMohamad Nizam IsmailОценок пока нет

- Audit Engagement Strategy (Driving Audit Value, Vol. III): The Best Practice Strategy Guide for Maximising the Added Value of the Internal Audit EngagementsОт EverandAudit Engagement Strategy (Driving Audit Value, Vol. III): The Best Practice Strategy Guide for Maximising the Added Value of the Internal Audit EngagementsОценок пока нет

- Module 1 For PrE 1 - Auditing and Assurance PrinciplesДокумент21 страницаModule 1 For PrE 1 - Auditing and Assurance PrinciplesCJ GranadaОценок пока нет

- The Audit Management Playbook 1611249376Документ44 страницыThe Audit Management Playbook 1611249376ahmed raouf100% (2)

- Internal Audit Good PracticeДокумент29 страницInternal Audit Good PracticerasmaheeОценок пока нет

- PPT 04Документ37 страницPPT 04Diaz Hesron Deo SimorangkirОценок пока нет

- AuditДокумент34 страницыAuditRashwanth Tc100% (7)

- Internal Audit FrameworkДокумент11 страницInternal Audit FrameworkJoe MashinyaОценок пока нет

- Communicating Audit Results and InsightsДокумент28 страницCommunicating Audit Results and Insightsdonna escotoОценок пока нет

- 1.2 Scope and Purpose of The ManualДокумент6 страниц1.2 Scope and Purpose of The ManualIbrahim AqeelОценок пока нет

- 2017-1170 QAL-Insights To Quality Q4-FINALДокумент2 страницы2017-1170 QAL-Insights To Quality Q4-FINALMerta WiramaОценок пока нет

- Module 1 For Acctg 3119 - Auditing and Assurance PrinciplesДокумент21 страницаModule 1 For Acctg 3119 - Auditing and Assurance PrinciplesJamille Causing AgsamosamОценок пока нет

- Path To QualityДокумент10 страницPath To QualitysjmpakОценок пока нет

- 8a LLDC Annual Internal Audit Report 2017-18 - FinalДокумент10 страниц8a LLDC Annual Internal Audit Report 2017-18 - FinalhanifahОценок пока нет

- Ringkasan CHAPTER 6 8 9 10 12 SOAДокумент29 страницRingkasan CHAPTER 6 8 9 10 12 SOAlely2014100% (2)

- IPPF Practice Guide. MeasurINg INterNal Audit Effectiveness and EfficiencyДокумент19 страницIPPF Practice Guide. MeasurINg INterNal Audit Effectiveness and EfficiencyFazlihaq Durrani100% (1)

- Implementation Guide 2201: Standard 2201 - Planning ConsiderationsДокумент5 страницImplementation Guide 2201: Standard 2201 - Planning ConsiderationsSyed HasanОценок пока нет

- The Significance of Auditing in Project Management: Bhavani Roopa PriyankaДокумент9 страницThe Significance of Auditing in Project Management: Bhavani Roopa PriyankaIshwarОценок пока нет

- Solutions Manual: 1st EditionДокумент18 страницSolutions Manual: 1st EditionJunior WaqairasariОценок пока нет

- Chapter One On ScreenДокумент60 страницChapter One On Screenadane24Оценок пока нет

- Week 11 Report: Presented By: Aileen M. Manangan Joebert S. RoderosДокумент27 страницWeek 11 Report: Presented By: Aileen M. Manangan Joebert S. RoderosKim SeokjinОценок пока нет

- Audit Liquid Measurement (Class 7050)Документ4 страницыAudit Liquid Measurement (Class 7050)yoyokpurwantoОценок пока нет

- 3 Audit PlanningДокумент15 страниц3 Audit Planningarc chanukaОценок пока нет

- Hse PlanДокумент13 страницHse PlanbaraaОценок пока нет

- IFRC Framework For EvaluationДокумент21 страницаIFRC Framework For EvaluationAbraham LebezaОценок пока нет

- Basicinternalauditing 1255043287052 Phpapp02Документ25 страницBasicinternalauditing 1255043287052 Phpapp02Liew Chee KiongОценок пока нет

- ADAA - Internal Audit ManualДокумент166 страницADAA - Internal Audit Manualkumaraperumal100% (1)

- IG 2000 Managing The Internal Audit ActivityДокумент5 страницIG 2000 Managing The Internal Audit ActivitygdegirolamoОценок пока нет

- How To Plan An Audit EngagementДокумент14 страницHow To Plan An Audit EngagementMarcela100% (1)

- Background and Purpose of The Guide: (Ia Cop)Документ32 страницыBackground and Purpose of The Guide: (Ia Cop)JasmineОценок пока нет

- CIA - Wiley & Vallabhaneni Part 2Документ80 страницCIA - Wiley & Vallabhaneni Part 2Kay Cee TangalinОценок пока нет

- OM and CourseMaterial of CertificateProgramme On Internal AuditДокумент404 страницыOM and CourseMaterial of CertificateProgramme On Internal AuditMRL AccountsОценок пока нет

- Week 13 Report: Presented By: Aileen M. Manangan Joebert S. RoderosДокумент24 страницыWeek 13 Report: Presented By: Aileen M. Manangan Joebert S. RoderosKim SeokjinОценок пока нет

- Review Handbook 2023Документ96 страницReview Handbook 2023sujung.hurОценок пока нет

- How To Plan An Audit Engagement IIA UKДокумент14 страницHow To Plan An Audit Engagement IIA UKJohn NashОценок пока нет

- BSI Internal Audit TipsДокумент12 страницBSI Internal Audit TipsAdrian AustinОценок пока нет

- Framework of Quality Assurance 18 PDFДокумент54 страницыFramework of Quality Assurance 18 PDFWafaa Safaei Tolami100% (1)

- Quality Assessment Manual Chapter 1 PDFДокумент8 страницQuality Assessment Manual Chapter 1 PDFAlbertus Yani100% (1)

- Internal Audit Work PlanДокумент23 страницыInternal Audit Work PlanHoang NguyenОценок пока нет

- Lecture 5 - Main Audit Concepts and Planning The AuditДокумент49 страницLecture 5 - Main Audit Concepts and Planning The AuditĐỗ LinhОценок пока нет

- AuditingДокумент18 страницAuditingonyrulanamОценок пока нет

- Execute A Risk AssessmentДокумент2 страницыExecute A Risk AssessmentRhea SimoneОценок пока нет

- MU1 Module 1 PowerpointДокумент36 страницMU1 Module 1 PowerpointCGASTUFF100% (1)

- Risk Based Internal Auditing: Chartered Institute of Internal AuditorsДокумент3 страницыRisk Based Internal Auditing: Chartered Institute of Internal AuditorsPujito KusworoОценок пока нет

- Insightstoqualityq 22022Документ1 страницаInsightstoqualityq 22022HazelLibanОценок пока нет

- Eaq Audit Risk Assessment ToolДокумент25 страницEaq Audit Risk Assessment ToolBaljeet SinghОценок пока нет

- Auditing 2 - Kelompok 12Документ21 страницаAuditing 2 - Kelompok 12Nabila Aprilia100% (1)

- AuditBoard Audit Management Playbook WPДокумент46 страницAuditBoard Audit Management Playbook WPvaniaОценок пока нет

- How To Plan An Audit EngagementДокумент14 страницHow To Plan An Audit Engagementmoh1122Оценок пока нет

- Appendix 1 SNC Annual Report Re-Issue Format AmendmentsДокумент18 страницAppendix 1 SNC Annual Report Re-Issue Format AmendmentsMaureen del RosarioОценок пока нет

- Agile Auditing Book Summary - FNL CRXДокумент13 страницAgile Auditing Book Summary - FNL CRXTrieu NamОценок пока нет

- What Is The Role and Responsibilities of A Iso Iso 45001Документ4 страницыWhat Is The Role and Responsibilities of A Iso Iso 45001Bhagat DeepakОценок пока нет

- Annual Audit Plan: Prepared By: Alvarez, LealynДокумент30 страницAnnual Audit Plan: Prepared By: Alvarez, LealynGerlyn Garcia100% (2)

- Risk-Based Auditing - A Value Add PropositionДокумент4 страницыRisk-Based Auditing - A Value Add PropositionHawkdollar HawkdollarОценок пока нет

- Annual Internal Audit Coverage PlansДокумент8 страницAnnual Internal Audit Coverage PlansAartikaОценок пока нет

- 19 WMPF Audit Plan 201415Документ12 страниц19 WMPF Audit Plan 201415Veena HingarhОценок пока нет

- Internal Audit Guidance Assessing ISO 90Документ13 страницInternal Audit Guidance Assessing ISO 90Srinivas Yanamandra100% (1)

- Internal AuditДокумент39 страницInternal AuditeosmostafaОценок пока нет

- 1 Quality Assessment Manual Chapter 1Документ10 страниц1 Quality Assessment Manual Chapter 1Tono Gitu100% (2)

- Kassar 2014Документ15 страницKassar 2014Dwi WinarniОценок пока нет

- Audit ProcessДокумент15 страницAudit ProcessDwi WinarniОценок пока нет

- Kassar 2014Документ15 страницKassar 2014Dwi WinarniОценок пока нет

- BSC and IA Ziegenfuss2000Документ10 страницBSC and IA Ziegenfuss2000Dwi WinarniОценок пока нет

- Faculty of Economics and Business - Accounting ProgramДокумент4 страницыFaculty of Economics and Business - Accounting ProgramDwi WinarniОценок пока нет

- Journal of Intellectual Capital: Article InformationДокумент36 страницJournal of Intellectual Capital: Article InformationDwi WinarniОценок пока нет

- 1 s2.0 S0959652617324149 MainДокумент19 страниц1 s2.0 S0959652617324149 MainDwi WinarniОценок пока нет

- FE107 Experimental ResultsДокумент11 страницFE107 Experimental ResultsEsapermana RiyanОценок пока нет

- Referencing Using The Documentary-Note (Oxford) System, Deakin UniversityДокумент9 страницReferencing Using The Documentary-Note (Oxford) System, Deakin UniversityjengadjОценок пока нет

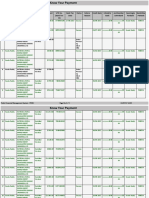

- SR No. Beneficiary Name Scheme Name Purpose Amount Utr No. (Bank TXN Id) Bank TXN Date Status Failure Reason Credit Date Uidasper Bank Acctnumber Asperbank Favoringas Perbank Bankiinas PerbankДокумент3 страницыSR No. Beneficiary Name Scheme Name Purpose Amount Utr No. (Bank TXN Id) Bank TXN Date Status Failure Reason Credit Date Uidasper Bank Acctnumber Asperbank Favoringas Perbank Bankiinas PerbankAnand ReddyОценок пока нет

- CIS Kubernetes Benchmark v1.4.1Документ254 страницыCIS Kubernetes Benchmark v1.4.1Anonymous 4uxmV5Z4oОценок пока нет

- Funambol Whatisnewinv10 June11Документ23 страницыFunambol Whatisnewinv10 June11Eftakhar Chowdhury PallabОценок пока нет

- Operating Manual: Wheel Loader L538 - 432 From 13100Документ284 страницыOperating Manual: Wheel Loader L538 - 432 From 13100Jacques Van Niekerk80% (5)

- 2460 3660 FM Canadian CertificateДокумент2 страницы2460 3660 FM Canadian Certificateluis hernandezОценок пока нет

- Hyb 96 MhuaДокумент13 страницHyb 96 Mhuaأبو زينب المهندسОценок пока нет

- Introduction To ICT EthicsДокумент8 страницIntroduction To ICT EthicsJohn Niño FilipinoОценок пока нет

- IT Audit Exercise 2Документ1 страницаIT Audit Exercise 2wirdinaОценок пока нет

- Prime Vision Security Solutions - Company ProfileДокумент11 страницPrime Vision Security Solutions - Company ProfileAbdul QayyumОценок пока нет

- Prospectus 2019 20 PDFДокумент76 страницProspectus 2019 20 PDFDhruv goyalОценок пока нет

- EM Console Slowness and Stuck Thread IssueДокумент10 страницEM Console Slowness and Stuck Thread IssueAbdul JabbarОценок пока нет

- Sample FLAT FILE FOR SAPДокумент6 страницSample FLAT FILE FOR SAPMahadevan KrishnanОценок пока нет

- Reading and Writing Writing An EmailДокумент1 страницаReading and Writing Writing An EmailferfonsegonОценок пока нет

- 5400 Replace BBU BlockДокумент15 страниц5400 Replace BBU BlockAhmed HaggarОценок пока нет

- Influence of Nano - Sized Powder Content On Physical Properties of Waste Acid Refractory BrickДокумент19 страницInfluence of Nano - Sized Powder Content On Physical Properties of Waste Acid Refractory BrickamnajamОценок пока нет

- Experimental Study On Partial Replacement of Sand With Sugarcane Bagasse Ash in ConcreteДокумент3 страницыExperimental Study On Partial Replacement of Sand With Sugarcane Bagasse Ash in ConcreteRadix CitizenОценок пока нет

- CSS ExercisesДокумент8 страницCSS ExercisesWarnnie MusahОценок пока нет

- ابراج STCДокумент5 страницابراج STCMohamed F. AbdullahОценок пока нет

- Improving Lives of South Sudanese Communities Through Water and Sanitation: The Story of Salva DutДокумент1 страницаImproving Lives of South Sudanese Communities Through Water and Sanitation: The Story of Salva DutUNICEF South SudanОценок пока нет

- Acti 9 & Compact NSX/NS: Short Form Selection Chart - 2011Документ1 страницаActi 9 & Compact NSX/NS: Short Form Selection Chart - 2011Pierre-Jac VenterОценок пока нет

- Cable Sheath Voltage Limiters PresentationДокумент8 страницCable Sheath Voltage Limiters PresentationRaden ArmanadiОценок пока нет

- Foot Step Power Generation Using Piezoelectric MaterialДокумент3 страницыFoot Step Power Generation Using Piezoelectric MaterialYogeshОценок пока нет

- Adly 50 RS Parts ListДокумент50 страницAdly 50 RS Parts ListZsibrita GyörgyОценок пока нет

- Harry BerryДокумент2 страницыHarry BerryLuisОценок пока нет

- Buku Program Kopo 18Документ20 страницBuku Program Kopo 18Mieza Binti YusoffОценок пока нет

- Print Master ProjectДокумент62 страницыPrint Master ProjectVipin PouloseОценок пока нет

- Man Pa-4000Документ18 страницMan Pa-4000JOEY76BYОценок пока нет

- Antonio Stradivari, Cello, Cremona, 1726, The 'Comte de Saveuse' - TarisioДокумент1 страницаAntonio Stradivari, Cello, Cremona, 1726, The 'Comte de Saveuse' - TarisioUrko LarrañagaОценок пока нет