Вам также может понравиться

- F M AДокумент11 страницF M AAjay SahooОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Mean Devition and Co-EfficiantДокумент18 страницMean Devition and Co-EfficiantAjay SahooОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Accounting For LIPSAДокумент20 страницAccounting For LIPSAAjay Sahoo100% (1)

- Accounting Final AccountsДокумент20 страницAccounting Final AccountsAjay SahooОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Accounting For APARAJITAДокумент18 страницAccounting For APARAJITAAjay SahooОценок пока нет

- Accounting For JULLYДокумент20 страницAccounting For JULLYAjay SahooОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- F M AДокумент11 страницF M AAjay SahooОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- 14 Principles of Management of Henri FayolДокумент11 страниц14 Principles of Management of Henri FayolAjay Sahoo100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Costing Machine Hour RateДокумент27 страницCosting Machine Hour RateAjay SahooОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Introduction To PackagingДокумент12 страницIntroduction To PackagingAjay SahooОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Accounting Final AccountsДокумент18 страницAccounting Final AccountsAjay Sahoo100% (3)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Costing 8Документ12 страницCosting 8Ajay SahooОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- PackagingДокумент32 страницыPackagingAjay SahooОценок пока нет

- B S MДокумент10 страницB S MAjay Sahoo100% (1)

- Akter (2017)Документ7 страницAkter (2017)Eko PriyojadmikoОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Church Minute Nsample PDFДокумент6 страницChurch Minute Nsample PDFRueben RajОценок пока нет

- Detail P&LДокумент2 страницыDetail P&LPuteh BeseryОценок пока нет

- UK-060 (Bank and Cash Management)Документ13 страницUK-060 (Bank and Cash Management)Ashok KumarОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- BAR Training Services Booking FormДокумент2 страницыBAR Training Services Booking FormBritish Association of RemoversОценок пока нет

- The Payment System in LesothoДокумент10 страницThe Payment System in LesothoWishfulDownloadingОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Money Creation: Base, Also Known As High-Powered MoneyДокумент11 страницMoney Creation: Base, Also Known As High-Powered MoneyAbhishekSinghОценок пока нет

- Y-Z¡ I L-Z¡ Weavb (Evbv Bi M Î) : Y-E Env II WBQGДокумент4 страницыY-Z¡ I L-Z¡ Weavb (Evbv Bi M Î) : Y-E Env II WBQGNovelОценок пока нет

- Washington Mutual (WMI) - Motion of Shareholder William Duke To Allow Certain Documents and InformationДокумент148 страницWashington Mutual (WMI) - Motion of Shareholder William Duke To Allow Certain Documents and InformationmeischerОценок пока нет

- Brokerregulation 01mar18Документ79 страницBrokerregulation 01mar18Tosheef Allen KropenskiОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Skrill Automated Payments Interface GuideДокумент34 страницыSkrill Automated Payments Interface GuidetikerinfoОценок пока нет

- BOIUPIДокумент231 страницаBOIUPIchauhan0124urwanОценок пока нет

- Comparative Analysis of Different Insurance ProductsДокумент53 страницыComparative Analysis of Different Insurance Productsgsaraogi85% (39)

- Bank of Maharashtra ProjectДокумент43 страницыBank of Maharashtra ProjectNikhil BavaskarОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- PWC Global Fintech Report 2019 PDFДокумент29 страницPWC Global Fintech Report 2019 PDFAjith AjithОценок пока нет

- Houston Workshop D.authcheckdamДокумент32 страницыHouston Workshop D.authcheckdamAnonymous xifNvNОценок пока нет

- Sample Statement of Account For Travel AgencyДокумент3 страницыSample Statement of Account For Travel AgencyKJ S Bee100% (1)

- Digest of Edillon v. Manila Bankers Life Insurance Corp. (G.R. No. 34200)Документ1 страницаDigest of Edillon v. Manila Bankers Life Insurance Corp. (G.R. No. 34200)Rafael PangilinanОценок пока нет

- Your Payment ReceiptДокумент1 страницаYour Payment ReceiptRajat ReddyОценок пока нет

- Legal Tender LetterДокумент2 страницыLegal Tender LetterMoeB42488% (17)

- Kotak To HDFCДокумент91 страницаKotak To HDFCPRAKASHОценок пока нет

- Arb Attendance SheetДокумент6 страницArb Attendance SheetApril NОценок пока нет

- CH 03Документ44 страницыCH 03Mary A FreemonОценок пока нет

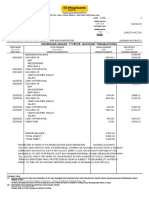

- Sadaqat Limited.: Commercial Invoice/Customer InvoiceДокумент6 страницSadaqat Limited.: Commercial Invoice/Customer InvoiceFurqan0% (1)

- Turtle Diagram of Cash Flow PDFДокумент1 страницаTurtle Diagram of Cash Flow PDFherikОценок пока нет

- Ibs Merlimau 1 30/06/20Документ1 страницаIbs Merlimau 1 30/06/20Fakhrurr HamdanОценок пока нет

- Research Report On Electronic Banking E-Banking ManagementДокумент5 страницResearch Report On Electronic Banking E-Banking ManagementshivkmrchauhanОценок пока нет

- O2C P2P Accounting Entries With India LocalizationДокумент2 страницыO2C P2P Accounting Entries With India LocalizationK.c. NayakОценок пока нет

- Prevention of Money Laundering ACT, 2002Документ22 страницыPrevention of Money Laundering ACT, 2002Anrick AhmedОценок пока нет

- Habib Bank LimitedДокумент16 страницHabib Bank Limitedhasanqureshi3949100% (2)