Вам также может понравиться

- 13 Investment in Equity SecuritiesДокумент146 страниц13 Investment in Equity SecuritiesDan Di100% (1)

- Third Week - Dsadfor PrintingДокумент14 страницThird Week - Dsadfor Printingyukiro rineva0% (2)

- FAR - RQ - Investment in AssociatesДокумент2 страницыFAR - RQ - Investment in AssociatesKriane Kei50% (2)

- Ch08 Property, Plant & EquipmentДокумент6 страницCh08 Property, Plant & EquipmentralphalonzoОценок пока нет

- Investment in Equity SecuritiesДокумент11 страницInvestment in Equity SecuritiesnikОценок пока нет

- Investment in AssociateДокумент2 страницыInvestment in AssociateChiChi0% (1)

- Exercise - Part 2Документ5 страницExercise - Part 2lois martinОценок пока нет

- Cel 1 Prac 1 Answer KeyДокумент15 страницCel 1 Prac 1 Answer KeyNJ MondigoОценок пока нет

- Investments in Debt and Equity SecuritiesДокумент41 страницаInvestments in Debt and Equity SecuritiesMonica Monica0% (1)

- Equity YyyДокумент33 страницыEquity YyyJude SantosОценок пока нет

- Chapter 14Документ8 страницChapter 14einnajeniale75% (4)

- Shareholders' EquityДокумент9 страницShareholders' EquityLeah Hope CedroОценок пока нет

- Test BankДокумент136 страницTest BankLouise100% (1)

- This Study Resource Was: Accounting For BondsДокумент4 страницыThis Study Resource Was: Accounting For BondsSeunghyun ParkОценок пока нет

- Financial Asset at Amortized CostДокумент14 страницFinancial Asset at Amortized CostLorenzo Diaz DipadОценок пока нет

- Revaluation: To The Treatment of Revaluation SurplusДокумент16 страницRevaluation: To The Treatment of Revaluation SurplusTurks100% (1)

- 2016 Vol 1 CH 8 Answers - Fin Acc SolManДокумент7 страниц2016 Vol 1 CH 8 Answers - Fin Acc SolManPamela Cruz100% (1)

- 8th PICPA National Accounting Quiz ShowdownДокумент28 страниц8th PICPA National Accounting Quiz Showdownrcaa04Оценок пока нет

- This Study Resource Was: Invesment in Equity Securities UploadedДокумент4 страницыThis Study Resource Was: Invesment in Equity Securities UploadedmerryОценок пока нет

- Quiz Week 8 Akm 2Документ6 страницQuiz Week 8 Akm 2Tiara Eva TresnaОценок пока нет

- Far Eastern University - Makati: Discussion ProblemsДокумент2 страницыFar Eastern University - Makati: Discussion ProblemsMarielle SidayonОценок пока нет

- I-Theories: Intangibles & Other AssetsДокумент19 страницI-Theories: Intangibles & Other Assetsaccounting filesОценок пока нет

- Accounting 106 SeatworkДокумент2 страницыAccounting 106 SeatworkLaizashi Carin50% (2)

- Global CompanyДокумент1 страницаGlobal Companydagohoy kennethОценок пока нет

- 1911 Investments Investment in Associate and Bond InvestmentДокумент13 страниц1911 Investments Investment in Associate and Bond InvestmentCykee Hanna Quizo LumongsodОценок пока нет

- FAR.2922 - Investments in Equity InstrumentsДокумент5 страницFAR.2922 - Investments in Equity InstrumentsBea San JoseОценок пока нет

- 162 020Документ5 страниц162 020Angelli LamiqueОценок пока нет

- Qualifying Examination: Financial Accounting 2Документ11 страницQualifying Examination: Financial Accounting 2Patricia ByunОценок пока нет

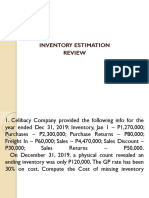

- B. Inventory EstimationДокумент6 страницB. Inventory EstimationAce TevesОценок пока нет

- Problems 3 PRELIM TASK FINALДокумент4 страницыProblems 3 PRELIM TASK FINALJohn Francis RosasОценок пока нет

- Far Review - Notes and Receivable AssessmentДокумент6 страницFar Review - Notes and Receivable AssessmentLuisa Janelle BoquirenОценок пока нет

- First QuizДокумент4 страницыFirst QuizArn HicoОценок пока нет

- Module 13 Present ValueДокумент10 страницModule 13 Present ValueChristine Elaine LamanОценок пока нет

- Retained EarningsДокумент76 страницRetained EarningsKristine DoydoraОценок пока нет

- Comprehensive Topics HandoutsДокумент16 страницComprehensive Topics HandoutsGrace CorpoОценок пока нет

- Compound Financial Instruments and Note PayableДокумент4 страницыCompound Financial Instruments and Note PayablePaula Rodalyn MateoОценок пока нет

- Financial Accounting and ReportingДокумент3 страницыFinancial Accounting and ReportingJAPОценок пока нет

- p1 IaДокумент1 страницаp1 IaLeika Gay Soriano OlarteОценок пока нет

- Derivatives Qs PDFДокумент5 страницDerivatives Qs PDFLara Camille CelestialОценок пока нет

- CH 14Документ44 страницыCH 14NghiaBuiQuang100% (3)

- FAR - Biological Assets and Agricultural ProduceДокумент2 страницыFAR - Biological Assets and Agricultural ProduceMariella Catacutan67% (3)

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Документ3 страницы(Use The Below Problem To Answers The Succeeding Four (4) Questions.)Janine LerumОценок пока нет

- Module 3 InvestmentДокумент12 страницModule 3 InvestmentKim JisooОценок пока нет

- 9.2 Investment in AssociateДокумент6 страниц9.2 Investment in AssociateJorufel PapasinОценок пока нет

- Pisodira PDFДокумент46 страницPisodira PDFjhouvanОценок пока нет

- Cag QuestionsДокумент24 страницыCag QuestionsJason Dave VidadОценок пока нет

- Debt Securities ReviewerДокумент30 страницDebt Securities Reviewerjhie boterОценок пока нет

- Chapter 21 - Shareholder's EquityДокумент45 страницChapter 21 - Shareholder's EquityJeong malyow0% (1)

- Equity Retained Earnings 2Документ2 страницыEquity Retained Earnings 2Marked ReverseОценок пока нет

- Direct Financing Lease Bafacr4x OnlineglimpsenujpiaДокумент4 страницыDirect Financing Lease Bafacr4x OnlineglimpsenujpiaAga Mathew MayugaОценок пока нет

- Wasting AssetsДокумент4 страницыWasting AssetsjomelОценок пока нет

- 3 Revaluation SurplusДокумент1 страница3 Revaluation SurplusNeighvestОценок пока нет

- QuizДокумент2 страницыQuizAlyssa CamposОценок пока нет

- Mahusay Acc227 Module 4Документ4 страницыMahusay Acc227 Module 4Jeth MahusayОценок пока нет

- Illustrative Problem - Sales Type Lease With Residual ValueДокумент2 страницыIllustrative Problem - Sales Type Lease With Residual ValueQueen ValleОценок пока нет

- Saint Joseph College of Sindangan Incorporated College of AccountancyДокумент18 страницSaint Joseph College of Sindangan Incorporated College of AccountancyRendall Craig Refugio0% (1)

- Chapter 13 Appendix CДокумент30 страницChapter 13 Appendix Cfoxstupidfox100% (1)

- 313738Документ90 страниц313738louis04Оценок пока нет

- Ncrcup FarДокумент13 страницNcrcup FarKenneth RobledoОценок пока нет

- 01 Investment in Equity Securities - V2 With AnswersДокумент17 страниц01 Investment in Equity Securities - V2 With AnswersJEFFERSON CUTE71% (7)

- Biological AssetsДокумент21 страницаBiological AssetsdfsdfdsfОценок пока нет

- Investment in Debt Securities 2Документ4 страницыInvestment in Debt Securities 2dfsdfdsf100% (1)

- Investments in Debt SecuritiesДокумент19 страницInvestments in Debt SecuritiesdfsdfdsfОценок пока нет

- Fin Act Rev ArДокумент10 страницFin Act Rev ArdfsdfdsfОценок пока нет

- Investments in Debt SecuritiesДокумент19 страницInvestments in Debt SecuritiesdfsdfdsfОценок пока нет

- Intermediate Accounting, Part 1Документ7 страницIntermediate Accounting, Part 1dfsdfdsfОценок пока нет

- 20,000 Prepaid Rent 100,000 Rent ExpenseДокумент3 страницы20,000 Prepaid Rent 100,000 Rent ExpensedfsdfdsfОценок пока нет

- Multiple Linear RegressionДокумент26 страницMultiple Linear RegressionMarlene G Padigos100% (2)

- DBA Daily StatusДокумент9 страницDBA Daily StatuspankajОценок пока нет

- Critical Review For Cooperative LearningДокумент3 страницыCritical Review For Cooperative LearninginaОценок пока нет

- Administrator's Guide: SeriesДокумент64 страницыAdministrator's Guide: SeriesSunny SaahilОценок пока нет

- Database Programming With SQL Section 2 QuizДокумент6 страницDatabase Programming With SQL Section 2 QuizJosé Obeniel LópezОценок пока нет

- Right Hand Man LyricsДокумент11 страницRight Hand Man LyricsSteph CollierОценок пока нет

- 2,3,5 Aqidah Dan QHДокумент5 страниц2,3,5 Aqidah Dan QHBang PaingОценок пока нет

- Thesis Statement VampiresДокумент6 страницThesis Statement Vampireslaurasmithdesmoines100% (2)

- Bagon-Taas Adventist Youth ConstitutionДокумент11 страницBagon-Taas Adventist Youth ConstitutionJoseph Joshua A. PaLaparОценок пока нет

- Summar Training Report HRTC TRAINING REPORTДокумент43 страницыSummar Training Report HRTC TRAINING REPORTPankaj ChauhanОценок пока нет

- Hydrogen Peroxide DripДокумент13 страницHydrogen Peroxide DripAya100% (1)

- Lets Install Cisco ISEДокумент8 страницLets Install Cisco ISESimon GarciaОценок пока нет

- Grade 3Документ4 страницыGrade 3Shai HusseinОценок пока нет

- S - BlockДокумент21 страницаS - BlockRakshit Gupta100% (2)

- Bab 3 - Soal-Soal No. 4 SD 10Документ4 страницыBab 3 - Soal-Soal No. 4 SD 10Vanni LimОценок пока нет

- From Jest To Earnest by Roe, Edward Payson, 1838-1888Документ277 страницFrom Jest To Earnest by Roe, Edward Payson, 1838-1888Gutenberg.org100% (1)

- Prime White Cement vs. Iac Assigned CaseДокумент6 страницPrime White Cement vs. Iac Assigned CaseStephanie Reyes GoОценок пока нет

- Music 20 Century: What You Need To Know?Документ8 страницMusic 20 Century: What You Need To Know?Reinrick MejicoОценок пока нет

- Ad1 MCQДокумент11 страницAd1 MCQYashwanth Srinivasa100% (1)

- Average Waves in Unprotected Waters by Anne Tyler - Summary PDFДокумент1 страницаAverage Waves in Unprotected Waters by Anne Tyler - Summary PDFRK PADHI0% (1)

- Working Capital Management-FinalДокумент70 страницWorking Capital Management-FinalharmitkОценок пока нет

- (Music of The African Diaspora) Robin D. Moore-Music and Revolution - Cultural Change in Socialist Cuba (Music of The African Diaspora) - University of California Press (2006) PDFДокумент367 страниц(Music of The African Diaspora) Robin D. Moore-Music and Revolution - Cultural Change in Socialist Cuba (Music of The African Diaspora) - University of California Press (2006) PDFGabrielОценок пока нет

- Concrete Design Using PROKONДокумент114 страницConcrete Design Using PROKONHesham Mohamed100% (2)

- Physics - TRIAL S1, STPM 2022 - CoverДокумент1 страницаPhysics - TRIAL S1, STPM 2022 - CoverbenОценок пока нет

- Invitation 2023Документ10 страницInvitation 2023Joanna Marie Cruz FelipeОценок пока нет

- SBE13 CH 18Документ74 страницыSBE13 CH 18Shad ThiệnОценок пока нет

- Marcelo H Del PilarДокумент8 страницMarcelo H Del PilarLee Antonino AtienzaОценок пока нет

- Cruz-Arevalo v. Layosa DigestДокумент2 страницыCruz-Arevalo v. Layosa DigestPatricia Ann RueloОценок пока нет

- AdvacДокумент13 страницAdvacAmie Jane MirandaОценок пока нет

- Anti-Epileptic Drugs: - Classification of SeizuresДокумент31 страницаAnti-Epileptic Drugs: - Classification of SeizuresgopscharanОценок пока нет

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNОт Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNРейтинг: 4.5 из 5 звезд4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaОт EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaРейтинг: 3.5 из 5 звезд3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthОт EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthРейтинг: 4 из 5 звезд4/5 (20)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaОт EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaРейтинг: 4.5 из 5 звезд4.5/5 (14)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОт EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОценок пока нет

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursОт EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursРейтинг: 5 из 5 звезд5/5 (13)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisОт EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisРейтинг: 5 из 5 звезд5/5 (6)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingОт EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingРейтинг: 4.5 из 5 звезд4.5/5 (17)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successОт EverandReady, Set, Growth hack:: A beginners guide to growth hacking successРейтинг: 4.5 из 5 звезд4.5/5 (93)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamОт EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamОценок пока нет

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОт EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialРейтинг: 4.5 из 5 звезд4.5/5 (32)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyОт EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyРейтинг: 3 из 5 звезд3/5 (1)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsОт EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsОценок пока нет

- Creating Shareholder Value: A Guide For Managers And InvestorsОт EverandCreating Shareholder Value: A Guide For Managers And InvestorsРейтинг: 4.5 из 5 звезд4.5/5 (8)

- Product-Led Growth: How to Build a Product That Sells ItselfОт EverandProduct-Led Growth: How to Build a Product That Sells ItselfРейтинг: 5 из 5 звезд5/5 (1)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressОт EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressОценок пока нет

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondОт EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondОценок пока нет

- Mind over Money: The Psychology of Money and How to Use It BetterОт EverandMind over Money: The Psychology of Money and How to Use It BetterРейтинг: 4 из 5 звезд4/5 (24)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsОт EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsРейтинг: 4.5 из 5 звезд4.5/5 (21)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)От EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Рейтинг: 4.5 из 5 звезд4.5/5 (4)

- Applied Corporate Finance. What is a Company worth?От EverandApplied Corporate Finance. What is a Company worth?Рейтинг: 3 из 5 звезд3/5 (2)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorОт EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorОценок пока нет

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursОт EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursРейтинг: 4.5 из 5 звезд4.5/5 (8)