Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Industrial RelationsДокумент20 страницIndustrial RelationsankitakusОценок пока нет

- Legal Opinion Johnsan Blue Industrial Suspension AmendmentДокумент2 страницыLegal Opinion Johnsan Blue Industrial Suspension AmendmentRudiver Jungco JrОценок пока нет

- Binod RajwarДокумент3 страницыBinod RajwarSHYAMA AUTOMOBILESОценок пока нет

- Naturecare Products: Risk Identification ReportДокумент2 страницыNaturecare Products: Risk Identification Reporte_dmsaveОценок пока нет

- Project Report On Birla Sun LifeДокумент62 страницыProject Report On Birla Sun Lifeeshaneeraj94% (34)

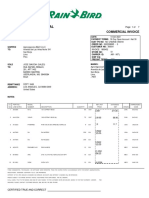

- Rain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Документ7 страницRain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Alejandra JamboОценок пока нет

- Financial Planning & ForecastingДокумент44 страницыFinancial Planning & Forecastingnageshalways503275% (4)

- Bhakti Chavan CV For HR ProfileДокумент3 страницыBhakti Chavan CV For HR ProfileADAT TestОценок пока нет

- 5.1 Productivity Engineering and Management Part 1 - BAGULBAGULДокумент28 страниц5.1 Productivity Engineering and Management Part 1 - BAGULBAGULrobinОценок пока нет

- Accenture Study Guide Certified AdministratorДокумент7 страницAccenture Study Guide Certified AdministratorViv ekОценок пока нет

- WSCMДокумент9 страницWSCMNishant goyalОценок пока нет

- SampleFullPaperforaBusinessPlanProposalLOKAL LOCAДокумент279 страницSampleFullPaperforaBusinessPlanProposalLOKAL LOCANicole SorianoОценок пока нет

- Mahindra Annual Report SummaryДокумент3 страницыMahindra Annual Report Summaryvishakha AGRAWALОценок пока нет

- Chap 009Документ21 страницаChap 009Kedia Rama50% (2)

- Kellog's Rice Krispies Cereal Brand PresentationДокумент16 страницKellog's Rice Krispies Cereal Brand PresentationSanni Fatima100% (3)

- ANILAO BANK (RURAL BANK OF ANILAO (ILOILO) INC - HTMДокумент2 страницыANILAO BANK (RURAL BANK OF ANILAO (ILOILO) INC - HTMJim De VegaОценок пока нет

- New Amazon BPLДокумент19 страницNew Amazon BPLpallraunakОценок пока нет

- Five Forces ModelДокумент6 страницFive Forces Modelakankshashahi1986Оценок пока нет

- Project of T.Y BbaДокумент49 страницProject of T.Y BbaJeet Mehta0% (1)

- Good Morning! Please Download Your Lecture Slides HereДокумент84 страницыGood Morning! Please Download Your Lecture Slides HereCiise Cali HaybeОценок пока нет

- Tradenet Funded Account Review - ($14,000 Buying Power)Документ3 страницыTradenet Funded Account Review - ($14,000 Buying Power)Enrique BlancoОценок пока нет

- 210: Understand How To Communicate With Others Within Building Services EngineeringДокумент3 страницы210: Understand How To Communicate With Others Within Building Services EngineeringGheorghe Ciubotaru50% (4)

- Footwear Industry in NepalДокумент76 страницFootwear Industry in Nepalsubham jaiswalОценок пока нет

- Organisation Study - Project Report For Mba Iii Semester - MG University - Kottayam - KeralaДокумент62 страницыOrganisation Study - Project Report For Mba Iii Semester - MG University - Kottayam - KeralaSasikumar R Nair79% (19)

- Introduction of BRAC Bank's centralized operations during COVIDДокумент4 страницыIntroduction of BRAC Bank's centralized operations during COVIDTarannum TahsinОценок пока нет

- Breakfast is the Most Important Meal: Starting a Pancake House BusinessДокумент28 страницBreakfast is the Most Important Meal: Starting a Pancake House BusinessChristian Lim100% (1)

- Asm1 - Bee - Ha Thi VanДокумент25 страницAsm1 - Bee - Ha Thi VanVân HàОценок пока нет

- Infosys Sourcing & Procurement - Fact Sheet: S2C R2I I2PДокумент2 страницыInfosys Sourcing & Procurement - Fact Sheet: S2C R2I I2PGautam SinghalОценок пока нет

- SITXFIN002 Assignment 1Документ23 страницыSITXFIN002 Assignment 1mishal chОценок пока нет

- Adjudication Order in Respect of M/s. Tulive Developers LTD., Mr. Atul Gupta and Mr. K V Ramana in The Matter of M/s. Tulive Developers Ltd.Документ25 страницAdjudication Order in Respect of M/s. Tulive Developers LTD., Mr. Atul Gupta and Mr. K V Ramana in The Matter of M/s. Tulive Developers Ltd.Shyam SunderОценок пока нет