Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Blue and White Project Proposal - PresentationДокумент18 страницBlue and White Project Proposal - PresentationMohamed RadwanОценок пока нет

- Account List PT Adi JayaДокумент1 страницаAccount List PT Adi JayaLutfiyah Achmad AlkaffОценок пока нет

- Cs Ins 05 2021Документ2 страницыCs Ins 05 2021Sri CharanОценок пока нет

- Manual Instructions For Union Budget 2023-2024Документ13 страницManual Instructions For Union Budget 2023-2024Vivek Raj100% (1)

- Solved Phyllis Sued Martin S Estate and Won A 65 000 SettlementДокумент1 страницаSolved Phyllis Sued Martin S Estate and Won A 65 000 SettlementAnbu jaromiaОценок пока нет

- FBR Tax FilingДокумент48 страницFBR Tax FilingMuhammad Waqas Hanif100% (1)

- Chapter 13-B: Special Allowable Itemized Deduction & NET Operating Loss Carry OverДокумент66 страницChapter 13-B: Special Allowable Itemized Deduction & NET Operating Loss Carry OverPrincessaxxxОценок пока нет

- Math 11 ABM Business Math Q2 Week 3Документ18 страницMath 11 ABM Business Math Q2 Week 3Flordilyn DichonОценок пока нет

- Atty. Cardona Tax 1 Syllabus RevДокумент12 страницAtty. Cardona Tax 1 Syllabus RevnayhrbОценок пока нет

- Revenue Growth AnalysisДокумент5 страницRevenue Growth Analysisyarsuthit279Оценок пока нет

- Monthly Expenses: Rent Food Tuition Books Entertainment Car Payment Gas MiscellaneousДокумент3 страницыMonthly Expenses: Rent Food Tuition Books Entertainment Car Payment Gas MiscellaneousMuqiew HanisОценок пока нет

- Akshay - Dev@vedanta - Co.in F16Документ10 страницAkshay - Dev@vedanta - Co.in F16Akshay DevОценок пока нет

- Billing Address: Tax InvoiceДокумент1 страницаBilling Address: Tax InvoicePratheeksha ShettyОценок пока нет

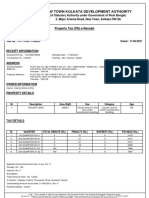

- New Town Kolkata Development Authority: Property Tax (PD) E-ReceiptДокумент2 страницыNew Town Kolkata Development Authority: Property Tax (PD) E-ReceiptSSK DEVELOPERSОценок пока нет

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 409150350210720 Assessment Year: 2020-21Документ7 страницItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 409150350210720 Assessment Year: 2020-21Vasanth Kumar AllaОценок пока нет

- Payslip Jan 2023Документ1 страницаPayslip Jan 2023Palanivelan KamarajОценок пока нет

- ING Bank v. CIR (2015)Документ50 страницING Bank v. CIR (2015)Rain CoОценок пока нет

- GST NotesДокумент14 страницGST NotesPremajohnОценок пока нет

- CFAB Accounting Chapter 13. Statement of Cash FlowsДокумент27 страницCFAB Accounting Chapter 13. Statement of Cash FlowsHuy NguyenОценок пока нет

- Dave and Diane Starr of New Orleans Louisiana Both ofДокумент1 страницаDave and Diane Starr of New Orleans Louisiana Both oftrilocksp SinghОценок пока нет

- TAX - LEAD BATCH 3 - Preweek 2Документ13 страницTAX - LEAD BATCH 3 - Preweek 2Josiah ZeusОценок пока нет

- Nahiyan PDFДокумент1 страницаNahiyan PDFAfzal MahmudОценок пока нет

- City University of PasayДокумент19 страницCity University of PasayFroilan G. AgatepОценок пока нет

- Tax Invoice: SEN/CBE/0007 9-Jul-2022 100% Adv PaymentДокумент1 страницаTax Invoice: SEN/CBE/0007 9-Jul-2022 100% Adv PaymentMPM SENTHILОценок пока нет

- Accounting For Income Tax Valix StudentДокумент4 страницыAccounting For Income Tax Valix Studentvee viajeroОценок пока нет

- VP NG9XKB5Z InvoicesДокумент2 страницыVP NG9XKB5Z InvoicesKhushin LakharaОценок пока нет

- Boat InvoiceДокумент1 страницаBoat Invoiceakm100% (1)

- TEST PAPER-1 House PropertyДокумент2 страницыTEST PAPER-1 House PropertyBharatbhusan RoutОценок пока нет

- Individual PAYG Payment Summary Schedule 2021Документ2 страницыIndividual PAYG Payment Summary Schedule 2021uly01 cubillaОценок пока нет

- October InvoiceДокумент2 страницыOctober Invoicesubhenduchatterjee94Оценок пока нет