Вам также может понравиться

- Chapter 1 Audit of Cash and Cash EquivalentsДокумент127 страницChapter 1 Audit of Cash and Cash EquivalentsAgatha de Castro81% (21)

- IR1 CashcashEquivДокумент4 страницыIR1 CashcashEquivMadielyn Santarin MirandaОценок пока нет

- Auditing and Assurance Principles Pre TestДокумент9 страницAuditing and Assurance Principles Pre TestKryzzel Anne JonОценок пока нет

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionОт EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionОценок пока нет

- Agamata Answer KeyДокумент5 страницAgamata Answer KeyBromanineОценок пока нет

- Technical AnalysisДокумент34 страницыTechnical AnalysisBromanine100% (1)

- Ielts Reading Actual Tests With Suggested Answers Oct 2021 JДокумент508 страницIelts Reading Actual Tests With Suggested Answers Oct 2021 JHarpreet Singh JohalОценок пока нет

- ACCTG102 MidtermQ1.5 Cash Make Up ExamДокумент6 страницACCTG102 MidtermQ1.5 Cash Make Up ExamBarrylou Manayan100% (1)

- Audit of CashДокумент9 страницAudit of CashRizzel SubaОценок пока нет

- Long Quiz 1 Acc 205Документ6 страницLong Quiz 1 Acc 205Philip LarozaОценок пока нет

- AUD02 - 05 Audit of Cash and Cash EquivalentsДокумент3 страницыAUD02 - 05 Audit of Cash and Cash EquivalentsMark BajacanОценок пока нет

- Audit of Cash (Printable Handout)Документ6 страницAudit of Cash (Printable Handout)katrinailagan3131Оценок пока нет

- Quiz 3 Cash Bank Recon Past Exam CompressДокумент8 страницQuiz 3 Cash Bank Recon Past Exam CompressAubrey Shaiyne OfianaОценок пока нет

- AUDITING - PRELIM - For PrintingДокумент4 страницыAUDITING - PRELIM - For PrintingAndreiu Mark EsmeleОценок пока нет

- Special Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Документ4 страницыSpecial Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Ma Yra YmataОценок пока нет

- PrAE 304 Auditing and Assurance - MidtermsДокумент6 страницPrAE 304 Auditing and Assurance - MidtermsJeryl AlfantaОценок пока нет

- 1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashДокумент7 страниц1st Activity Cash and Cash Equivalents Bank Reconciliation Proof of CashSheidee ValienteОценок пока нет

- ExtAud 3 Midterm Exam W AnswersДокумент12 страницExtAud 3 Midterm Exam W AnswersJANET ILLESESОценок пока нет

- Bank Reconciliation (IA)Документ7 страницBank Reconciliation (IA)rufamaegarcia07Оценок пока нет

- Audit of Cash PDFДокумент11 страницAudit of Cash PDFShaira UntalanОценок пока нет

- Refresher Course: Audit of Cash and Cash EquivalentsДокумент4 страницыRefresher Course: Audit of Cash and Cash EquivalentsFery Ann100% (1)

- Auditing Problems Roque 2023-2024Документ385 страницAuditing Problems Roque 2023-2024Roisu De KuriОценок пока нет

- Substantive Testing For Cash and Cash EquivalentДокумент20 страницSubstantive Testing For Cash and Cash EquivalentPaul Anthony AspuriaОценок пока нет

- 03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyДокумент4 страницы03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyNye NyeОценок пока нет

- E-Handout On Audit of Cash and Cash EquivalentsДокумент12 страницE-Handout On Audit of Cash and Cash EquivalentsAsnifah AlinorОценок пока нет

- Quiz 1Документ11 страницQuiz 1Sam VeraОценок пока нет

- Audit of Cash and Cash Equivalent Problem 1 (Adapted)Документ6 страницAudit of Cash and Cash Equivalent Problem 1 (Adapted)Robelyn Asuna LegaraОценок пока нет

- Ap Tip Preweek 2017Документ58 страницAp Tip Preweek 2017Jay-L Tan100% (1)

- Auditing Problems: Audit of Cash and Cash Equivalents Problem No. 1Документ21 страницаAuditing Problems: Audit of Cash and Cash Equivalents Problem No. 1ATLASОценок пока нет

- Cash and Cash Equivalent QuizДокумент3 страницыCash and Cash Equivalent QuizApril Rose Sobrevilla DimpoОценок пока нет

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREДокумент12 страницACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaОценок пока нет

- PA QE - CCE HandoutsДокумент6 страницPA QE - CCE HandoutsBenicel Lane M. D. V.Оценок пока нет

- MT2 RevДокумент10 страницMT2 RevK P DewiОценок пока нет

- Ac3a Qe Oct2014 (TQ)Документ15 страницAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusОценок пока нет

- Practice SetДокумент4 страницыPractice SetXena Natividad100% (1)

- AP - Cash, Bank Recon, M2018Документ14 страницAP - Cash, Bank Recon, M2018Leah Hope CedroОценок пока нет

- Audit of Cash and Cash Equivalents: Problem No. 20Документ6 страницAudit of Cash and Cash Equivalents: Problem No. 20Robel MurilloОценок пока нет

- Holy Cross College: B. Cause and EffectДокумент12 страницHoly Cross College: B. Cause and EffectSam VeraОценок пока нет

- Audit Reviewaudit of CashДокумент14 страницAudit Reviewaudit of CashAndy LaluОценок пока нет

- 1st Long Exam (Summer 2022) WITHOUT ANSWERДокумент10 страниц1st Long Exam (Summer 2022) WITHOUT ANSWERDaphnie Kitch CatotalОценок пока нет

- Bank Recon & Proof-Set AДокумент2 страницыBank Recon & Proof-Set AJaypee BignoОценок пока нет

- Audit of Receivables CaseДокумент4 страницыAudit of Receivables CaseJohn Victor Mancilla MonzonОценок пока нет

- Acc 106 Quiz BR and Ar NoakДокумент8 страницAcc 106 Quiz BR and Ar Noakhoneyjoy salapantanОценок пока нет

- Audit of Cash and Cash EquivalentsДокумент4 страницыAudit of Cash and Cash EquivalentsstillwinmsОценок пока нет

- Cash and Cash Equivalents (Problems)Документ9 страницCash and Cash Equivalents (Problems)IAN PADAYOGDOGОценок пока нет

- F CFAS-EXAM - Docx 143874436Документ48 страницF CFAS-EXAM - Docx 143874436Athena AthenaОценок пока нет

- Midterm Examination Suggested AnswersДокумент9 страницMidterm Examination Suggested AnswersJoshua CaraldeОценок пока нет

- Ap Cash Cash Equivalents QuizДокумент8 страницAp Cash Cash Equivalents QuizJenny BernardinoОценок пока нет

- Audit of CashДокумент6 страницAudit of CashMark Lord Morales Bumagat100% (2)

- Reviewees IntaccДокумент6 страницReviewees IntaccMarvic Cabangunay0% (2)

- Cash and Cash Equivalents (Continuation)Документ7 страницCash and Cash Equivalents (Continuation)rufamaegarcia07Оценок пока нет

- AP Module 2 - Audit of Revenue-Receipt CycleДокумент8 страницAP Module 2 - Audit of Revenue-Receipt CycleHannah Jane ToribioОценок пока нет

- Peer Mentoring PostTestДокумент7 страницPeer Mentoring PostTestronnelОценок пока нет

- Questionnaire-Practical Accounting 1 Test I: Answer The FollowingДокумент10 страницQuestionnaire-Practical Accounting 1 Test I: Answer The FollowingKristee PlanesОценок пока нет

- Auditing Problems: First PreboardДокумент8 страницAuditing Problems: First PreboardCarlo AgravanteОценок пока нет

- Sample QuestionsДокумент9 страницSample QuestionsLorena DeofilesОценок пока нет

- Cpar 2Документ11 страницCpar 2Ana MarieОценок пока нет

- Bookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingОт EverandBookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingРейтинг: 4 из 5 звезд4/5 (2)

- 21St Century Computer Solutions: A Manual Accounting SimulationОт Everand21St Century Computer Solutions: A Manual Accounting SimulationОценок пока нет

- AK Mock BA 118.1 2nd LEДокумент6 страницAK Mock BA 118.1 2nd LEBromanineОценок пока нет

- Partners (Because TAC TCC PAC (New)Документ5 страницPartners (Because TAC TCC PAC (New)BromanineОценок пока нет

- AK Mock BA 99.2 1st LEДокумент4 страницыAK Mock BA 99.2 1st LEBromanineОценок пока нет

- AK Mock BA 141 1st LEДокумент2 страницыAK Mock BA 141 1st LEBromanineОценок пока нет

- 5ea7fb0c57f53 SEC Form 17A Dec2019Документ222 страницы5ea7fb0c57f53 SEC Form 17A Dec2019BromanineОценок пока нет

- Revised CPALE Syllabus - EditableДокумент19 страницRevised CPALE Syllabus - EditableBromanineОценок пока нет

- Mock Board Answer KeyДокумент2 страницыMock Board Answer KeyBromanineОценок пока нет

- PRTC Oct2019 1st PB Answer Key PDFДокумент2 страницыPRTC Oct2019 1st PB Answer Key PDFBromanineОценок пока нет

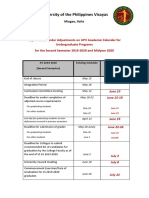

- University of The Philippines VisayasДокумент2 страницыUniversity of The Philippines VisayasBromanineОценок пока нет

- Abatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"Документ1 страницаAbatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"BromanineОценок пока нет

- (Pfrs/Ifrs 16) LeasesДокумент11 страниц(Pfrs/Ifrs 16) LeasesBromanineОценок пока нет

- 6th Practice Qs 99.2Документ3 страницы6th Practice Qs 99.2BromanineОценок пока нет

- Single Entry and Error CorrectionДокумент2 страницыSingle Entry and Error CorrectionBromanine0% (1)

- Hyperinflation and Current CostДокумент3 страницыHyperinflation and Current CostBromanineОценок пока нет

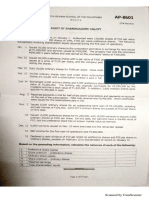

- AP 8603 - Audit of Property, Plant and EquipmentДокумент6 страницAP 8603 - Audit of Property, Plant and EquipmentBromanineОценок пока нет

- AP 8601 - Audit of Shareholders' EquityДокумент8 страницAP 8601 - Audit of Shareholders' EquityBromanineОценок пока нет

- Sec Reportorial RequirementsДокумент2 страницыSec Reportorial RequirementsBromanineОценок пока нет

- Opening BalancesДокумент37 страницOpening BalancesBromanineОценок пока нет

- Test Iii Cultural Social and Political OrganizationДокумент2 страницыTest Iii Cultural Social and Political OrganizationTin NatayОценок пока нет

- Bagi CHAPT 7 TUGAS INGGRIS W - YAHIEN PUTRIДокумент4 страницыBagi CHAPT 7 TUGAS INGGRIS W - YAHIEN PUTRIYahien PutriОценок пока нет

- Potassium Permanganate CARUSOL CarusCoДокумент9 страницPotassium Permanganate CARUSOL CarusColiebofreakОценок пока нет

- Grand Chapter Mentor ProgramДокумент13 страницGrand Chapter Mentor ProgramJulius Wright100% (1)

- Fluid Mechanics HydraulicsДокумент420 страницFluid Mechanics Hydraulicsanonymousdi3noОценок пока нет

- NEW Sample ISAT Questions RevisedДокумент14 страницNEW Sample ISAT Questions RevisedHa HoangОценок пока нет

- Test Bank Bank For Advanced Accounting 1 E by Bline 382235889 Test Bank Bank For Advanced Accounting 1 E by BlineДокумент31 страницаTest Bank Bank For Advanced Accounting 1 E by Bline 382235889 Test Bank Bank For Advanced Accounting 1 E by BlineDe GuzmanОценок пока нет

- Module 11 Activity Based CostingДокумент13 страницModule 11 Activity Based CostingMarjorie NepomucenoОценок пока нет

- Periodicity Review SL KeyДокумент4 страницыPeriodicity Review SL KeyYeyoung ParkОценок пока нет

- Project in Precal: Mary Joyce MolinesДокумент11 страницProject in Precal: Mary Joyce MolinesJaja KeykОценок пока нет

- Store Docket - Wood PeckerДокумент89 страницStore Docket - Wood PeckerRakesh KumarОценок пока нет

- High School Department PAASCU Accredited Academic Year 2017 - 2018Документ6 страницHigh School Department PAASCU Accredited Academic Year 2017 - 2018Kevin T. OnaroОценок пока нет

- 12.3 What Is The Nomenclature System For CFCS/HCFCS/HFCS? (Chemistry)Документ3 страницы12.3 What Is The Nomenclature System For CFCS/HCFCS/HFCS? (Chemistry)Riska IndriyaniОценок пока нет

- MINDSET 1 EXERCISES TEST 1 Pendientes 1º Bach VOCABULARY AND GRAMMARДокумент7 страницMINDSET 1 EXERCISES TEST 1 Pendientes 1º Bach VOCABULARY AND GRAMMARanaОценок пока нет

- Pemisah ZirconДокумент10 страницPemisah ZirconLorie Banka100% (1)

- Zoology LAB Scheme of Work 2023 Hsslive HSSДокумент7 страницZoology LAB Scheme of Work 2023 Hsslive HSSspookyvibee666Оценок пока нет

- Design of A Low Cost Hydrostatic Bearing: Anthony Raymond WongДокумент77 страницDesign of A Low Cost Hydrostatic Bearing: Anthony Raymond WongRogelio DiazОценок пока нет

- Decs vs. San DiegoДокумент7 страницDecs vs. San Diegochini17100% (2)

- TPT 510 Topic 3 - Warehouse in Relief OperationДокумент41 страницаTPT 510 Topic 3 - Warehouse in Relief OperationDR ABDUL KHABIR RAHMATОценок пока нет

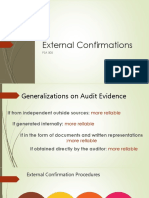

- Auditing BasicsДокумент197 страницAuditing BasicsMajanja AsheryОценок пока нет

- Membrane and TransportДокумент25 страницMembrane and TransportHafsa JalisiОценок пока нет

- REM630 Broch 756825 LRENdДокумент6 страницREM630 Broch 756825 LRENdsihamuОценок пока нет

- Ddec VДокумент30 страницDdec Vllama100% (1)

- Best S and Nocella, III (Eds.) - Igniting A Revolution - Voices in Defense of The Earth PDFДокумент455 страницBest S and Nocella, III (Eds.) - Igniting A Revolution - Voices in Defense of The Earth PDFRune Skjold LarsenОценок пока нет

- A B&C - List of Residents - VKRWA 12Документ10 страницA B&C - List of Residents - VKRWA 12blr.visheshОценок пока нет

- Differentiating Language Difference and Language Disorder - Information For Teachers Working With English Language Learners in The Schools PDFДокумент23 страницыDifferentiating Language Difference and Language Disorder - Information For Teachers Working With English Language Learners in The Schools PDFIqra HassanОценок пока нет

- PICUДокумент107 страницPICUsarikaОценок пока нет

- Kimberly Jimenez Resume 10Документ2 страницыKimberly Jimenez Resume 10kimberlymjОценок пока нет

- VRF-SLB013-EN - 0805115 - Catalogo Ingles 2015 PDFДокумент50 страницVRF-SLB013-EN - 0805115 - Catalogo Ingles 2015 PDFJhon Lewis PinoОценок пока нет