Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- 11 Steps of Automation ProjectДокумент12 страниц11 Steps of Automation Projecteng_xenon100% (1)

- E3D Training File PDFДокумент595 страницE3D Training File PDFWisdom Patrick Enang100% (6)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Summary of Collections and Remittances - BTДокумент13 страницSummary of Collections and Remittances - BTSt. Veronica Learning Center100% (1)

- Fabm2 Module 4Документ8 страницFabm2 Module 4Rea Mariz Jordan67% (3)

- Technical Manual 1Документ118 страницTechnical Manual 1Homero Silva100% (14)

- Clark S Positioning in Radiography 12th EditionДокумент532 страницыClark S Positioning in Radiography 12th EditionWisdom Patrick Enang95% (63)

- Consti2Digest - Juan Luna Subdivisio, Inc. Vs M. Sarmiento, Et Al, GR L-3538, (28 May 1952Документ3 страницыConsti2Digest - Juan Luna Subdivisio, Inc. Vs M. Sarmiento, Et Al, GR L-3538, (28 May 1952Lu CasОценок пока нет

- Fabm2 Q1Документ149 страницFabm2 Q1Gladys Angela Valdemoro100% (2)

- Income Tax Study MaterialДокумент303 страницыIncome Tax Study MaterialAbith Mathew77% (217)

- Sample Bussiness Plan For EntruprenerДокумент21 страницаSample Bussiness Plan For EntruprenerRavi BotveОценок пока нет

- Rent - Lease Agreement - Format 1Документ3 страницыRent - Lease Agreement - Format 1Priminox (info)100% (1)

- Introduction To Project ManagementДокумент31 страницаIntroduction To Project ManagementWisdom Patrick Enang100% (1)

- Mas-03: Absorption & Variable CostingДокумент4 страницыMas-03: Absorption & Variable CostingClint AbenojaОценок пока нет

- Dosing Pumps, Measurement & Control and Disinfection SystemsДокумент16 страницDosing Pumps, Measurement & Control and Disinfection SystemsjoseОценок пока нет

- Transfer ReportДокумент107 страницTransfer ReportWisdom Patrick EnangОценок пока нет

- Predictive Cruise Control in Hybrid Electric VehiclesДокумент11 страницPredictive Cruise Control in Hybrid Electric VehiclesWisdom Patrick EnangОценок пока нет

- Bank Card Wireless SkemmingДокумент1 страницаBank Card Wireless SkemmingWisdom Patrick EnangОценок пока нет

- Business Plan GuideДокумент4 страницыBusiness Plan GuideWisdom Patrick EnangОценок пока нет

- Modelling and Control of An Aftermarket HEV ModelДокумент22 страницыModelling and Control of An Aftermarket HEV ModelWisdom Patrick EnangОценок пока нет

- RM Discussion Board 2 - Wisdom Enang (S1727327)Документ3 страницыRM Discussion Board 2 - Wisdom Enang (S1727327)Wisdom Patrick EnangОценок пока нет

- Role of The PM (2018)Документ38 страницRole of The PM (2018)Wisdom Patrick EnangОценок пока нет

- Tom Gilb - The Evolutionary Project Managers HandbookДокумент72 страницыTom Gilb - The Evolutionary Project Managers HandbookHannibal100% (1)

- Transfer ReportДокумент107 страницTransfer ReportWisdom Patrick EnangОценок пока нет

- Preaching The Gospel Ver433Документ376 страницPreaching The Gospel Ver433Wisdom Patrick Enang100% (1)

- Creep of Metals 2009Документ35 страницCreep of Metals 2009Wisdom Patrick EnangОценок пока нет

- Impact of Biodieel On Catalyst PerformanceДокумент90 страницImpact of Biodieel On Catalyst PerformanceWisdom Patrick EnangОценок пока нет

- Sprockets - RenoldsДокумент72 страницыSprockets - RenoldsWisdom Patrick EnangОценок пока нет

- Sample Business PlanДокумент35 страницSample Business PlanWisdom Patrick EnangОценок пока нет

- Regenerative Braking AlgorithmДокумент7 страницRegenerative Braking AlgorithmWisdom Patrick EnangОценок пока нет

- Crown Screw Product GuideДокумент2 страницыCrown Screw Product GuideWisdom Patrick EnangОценок пока нет

- 03-SNR Bearing LifeДокумент34 страницы03-SNR Bearing LifeWisdom Patrick EnangОценок пока нет

- Project Management - Best Practices in WorkflowДокумент10 страницProject Management - Best Practices in WorkflowSami KakarОценок пока нет

- Modern Project Management - Successfully Integrating ProjectДокумент306 страницModern Project Management - Successfully Integrating Projectbazten100% (4)

- TechnicalДокумент117 страницTechnicalWisdom Patrick Enang100% (1)

- 40 - Section 9 of The Indian Income Tax ActДокумент18 страниц40 - Section 9 of The Indian Income Tax ActDhirendra SinghОценок пока нет

- United Tractors (UNTR IJ) : Regional Morning NotesДокумент5 страницUnited Tractors (UNTR IJ) : Regional Morning NotesAmirul AriffОценок пока нет

- Tata & Corus: Presented By:-Ankur Keshari Ashish Lal Priyanka Jain Ritu Gautam Presented To: - Ms. Parul NagarДокумент25 страницTata & Corus: Presented By:-Ankur Keshari Ashish Lal Priyanka Jain Ritu Gautam Presented To: - Ms. Parul Nagarnikzz_jainОценок пока нет

- Chapter 5 New11 - Block Hirt BookДокумент14 страницChapter 5 New11 - Block Hirt BookRamishaОценок пока нет

- Graduate Business School Faculty of Business ManagementДокумент17 страницGraduate Business School Faculty of Business ManagementSyahril NizamОценок пока нет

- Mabe CompanyДокумент16 страницMabe CompanyJijo Francis100% (1)

- CR-July-Aug-2022Документ6 страницCR-July-Aug-2022banglauserОценок пока нет

- 060469RR - Business Organizations - AssignmentsДокумент5 страниц060469RR - Business Organizations - AssignmentsG JhaОценок пока нет

- Objectives of SezДокумент48 страницObjectives of Sezasandilya100% (1)

- Eapp ReportДокумент26 страницEapp ReportRuth OlavereОценок пока нет

- All Types of Cost Incurred For That Product. Detailed Description of Each Type of Cost. Cost Sheet For Per Unit As Well As For 100 UnitsДокумент2 страницыAll Types of Cost Incurred For That Product. Detailed Description of Each Type of Cost. Cost Sheet For Per Unit As Well As For 100 UnitsakashniranjaneОценок пока нет

- P&A - Local Taxation of PEZAДокумент2 страницыP&A - Local Taxation of PEZACkey ArОценок пока нет

- PFRS 14 - Regulatory Deferral AccountsДокумент16 страницPFRS 14 - Regulatory Deferral Accountsdaniel coroniaОценок пока нет

- IBM According To Warren Buffett's Annual Letters To ShareholdersДокумент15 страницIBM According To Warren Buffett's Annual Letters To Shareholdersvahss_11Оценок пока нет

- RCMP Investment Presentation: NAP NДокумент27 страницRCMP Investment Presentation: NAP NInter 4DMОценок пока нет

- BDM of 12.10.2015 - Buyback Program, Sell Up and PayoutДокумент5 страницBDM of 12.10.2015 - Buyback Program, Sell Up and PayoutBVMF_RIОценок пока нет

- Aecon - Project IДокумент39 страницAecon - Project IRaji MohanОценок пока нет

- Coursera - IESE Foundations of Management SpecializationДокумент2 страницыCoursera - IESE Foundations of Management SpecializationEnrique EgeaОценок пока нет

- Basic Overview of Financial Statements: Income Statement Balance Sheet Cash Flow StatementДокумент10 страницBasic Overview of Financial Statements: Income Statement Balance Sheet Cash Flow StatementRutuja KunkulolОценок пока нет

- Annual Report 2017 PDFДокумент216 страницAnnual Report 2017 PDFemmanuelОценок пока нет

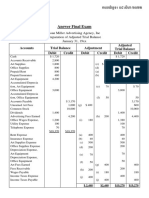

- Answer Final Exam (POA)Документ2 страницыAnswer Final Exam (POA)Phâk Tèr ÑgОценок пока нет