Вам также может понравиться

- Payroll - OutsourcingДокумент14 страницPayroll - OutsourcingRenato CostaОценок пока нет

- MAS Loan Application FormДокумент2 страницыMAS Loan Application FormSoowhysoo Twoonel100% (3)

- CA Foundation Accounting SolutionsДокумент117 страницCA Foundation Accounting SolutionsAkash AjayОценок пока нет

- Basel III: An Evaluation of New Banking RegulationsДокумент22 страницыBasel III: An Evaluation of New Banking RegulationsMegha BepariОценок пока нет

- GR Nos. 116124 25Документ2 страницыGR Nos. 116124 25Karen Gina DupraОценок пока нет

- French Business Dictionary: The Business Terms of France and CanadaОт EverandFrench Business Dictionary: The Business Terms of France and CanadaОценок пока нет

- PROBLEM 1 RESA Anna Corp. Uses The Direct Method To Prepare Its Statement of Cash Flows. Anna Corp.'s TrialДокумент16 страницPROBLEM 1 RESA Anna Corp. Uses The Direct Method To Prepare Its Statement of Cash Flows. Anna Corp.'s TrialJomar Villena100% (2)

- Nego Case2012Документ11 страницNego Case2012Jo-Al GealonОценок пока нет

- Financial Accounting AssignentДокумент8 страницFinancial Accounting AssignentHitesh LodayaОценок пока нет

- Answer Key of Rectification of Errors 2Документ3 страницыAnswer Key of Rectification of Errors 2menekyakiaОценок пока нет

- Class 11 Accounts SP 2 Answer KeyДокумент18 страницClass 11 Accounts SP 2 Answer KeyUdyamGОценок пока нет

- CFN 9305 Accounts Suggested Answers PDFДокумент4 страницыCFN 9305 Accounts Suggested Answers PDFDivya PunjabiОценок пока нет

- © The Institute of Chartered Accountants of IndiaДокумент12 страниц© The Institute of Chartered Accountants of IndiaOcto ManОценок пока нет

- Ans - 21.11.23 CA-foun. MTP Accounts Dec. 23Документ10 страницAns - 21.11.23 CA-foun. MTP Accounts Dec. 23RohitОценок пока нет

- Sample Paper: Maximum Marks 4Документ13 страницSample Paper: Maximum Marks 4PurvaОценок пока нет

- Admission of A Parnter - Work Sheet No - 2Документ7 страницAdmission of A Parnter - Work Sheet No - 2BLUE SKY GAMINGОценок пока нет

- CBSE Accountancy 12th Term 2 CH 3Документ5 страницCBSE Accountancy 12th Term 2 CH 3AadasОценок пока нет

- Ca-Foundation-Ppa - KP 28.10.23Документ6 страницCa-Foundation-Ppa - KP 28.10.23koteshdarshanala82Оценок пока нет

- Model Test Paper-5Документ26 страницModel Test Paper-5Lavagreat The greatОценок пока нет

- CA Foundation Accounts A MTP 2 June 2023Документ12 страницCA Foundation Accounts A MTP 2 June 2023Vranda RastogiОценок пока нет

- Hsslive Xii Acc 3 Admission of A Partner KeyДокумент8 страницHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadОценок пока нет

- Semester IДокумент5 страницSemester IAnonymous 1ClGHbiT0JОценок пока нет

- Rectification of Errors: Accountancy - II 1Документ3 страницыRectification of Errors: Accountancy - II 1M JEEVARATHNAM NAIDUОценок пока нет

- Test Paper 5 AnswersДокумент11 страницTest Paper 5 Answersshivampandit8235Оценок пока нет

- Financial Accounting: Assignment 3: Journal of Spade Company S.no Particulars Amount (DR.) Amount (CR.)Документ3 страницыFinancial Accounting: Assignment 3: Journal of Spade Company S.no Particulars Amount (DR.) Amount (CR.)ishaniОценок пока нет

- 67519bos54256 FND P1aДокумент11 страниц67519bos54256 FND P1aSurinder MohanОценок пока нет

- Accounting For Decision MakingДокумент15 страницAccounting For Decision MakingbrammaasОценок пока нет

- 3525 25113 Textbooksolution PDFДокумент40 страниц3525 25113 Textbooksolution PDFTushar Gupta100% (1)

- Class Work Journal EntryДокумент16 страницClass Work Journal EntryRishabh ChawlaОценок пока нет

- Marking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesДокумент9 страницMarking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesKunwar PalОценок пока нет

- MTP 15 28 Answers 1703566022Документ11 страницMTP 15 28 Answers 1703566022nilesh.nkj1325Оценок пока нет

- Internal Reconstruction Part-IIДокумент13 страницInternal Reconstruction Part-IIINTER SMARTIANSОценок пока нет

- Accounting Principles and PracticesДокумент10 страницAccounting Principles and PracticesGaganpreet KaurОценок пока нет

- Rectifiation of Error With Suspense AccountДокумент3 страницыRectifiation of Error With Suspense AccountSudharshan GОценок пока нет

- Partnership: AdmissionДокумент7 страницPartnership: AdmissionSweta SinghОценок пока нет

- Change in PSR NotesДокумент10 страницChange in PSR Noteskapilbishnoi.10a.svnОценок пока нет

- FA1 Chapter 8 EngДокумент18 страницFA1 Chapter 8 Enghahahaha wahahahhaОценок пока нет

- 06 Correction of Errors (I)Документ9 страниц06 Correction of Errors (I)Babamu Kalmoni JaatoОценок пока нет

- Atm Cafm Practical Revision NotesДокумент95 страницAtm Cafm Practical Revision Notesdroom8521Оценок пока нет

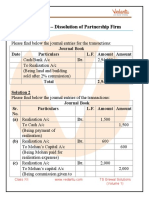

- TS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmДокумент17 страницTS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmMayank Garange100% (1)

- Problems Based On Ledger's Preparation P: Roblem 11Документ28 страницProblems Based On Ledger's Preparation P: Roblem 11Anonymous ameerОценок пока нет

- SQ AcoountaciiДокумент75 страницSQ AcoountaciiAditya bansal100% (1)

- Solution Ultimate Sample Paper 2Документ7 страницSolution Ultimate Sample Paper 2Nitin KumarОценок пока нет

- Admission of A PartnerДокумент21 страницаAdmission of A PartnerHarmohandeep singhОценок пока нет

- Exercisr For ProvisionДокумент6 страницExercisr For ProvisionRojesh BasnetОценок пока нет

- Solutions To Text Book Exercises: Rectification of ErrorsДокумент13 страницSolutions To Text Book Exercises: Rectification of ErrorsM JEEVARATHNAM NAIDUОценок пока нет

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Документ15 страницCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768Оценок пока нет

- Xi See Acc 2021 Set 2 MsДокумент5 страницXi See Acc 2021 Set 2 Mss1672snehil6353Оценок пока нет

- MGT101 12-15Документ62 страницыMGT101 12-15Nasir BashirОценок пока нет

- Marking Scheme 2020Документ5 страницMarking Scheme 2020Joanna GarciaОценок пока нет

- 2 Fundamentals of PartnershipДокумент11 страниц2 Fundamentals of PartnershipKartik JainОценок пока нет

- Solutions of CH - RetirementДокумент5 страницSolutions of CH - RetirementDamanjot SinghОценок пока нет

- PAC (BUSS B 1004) - ZainДокумент10 страницPAC (BUSS B 1004) - Zainnawal zaheerОценок пока нет

- BoardPaper 2019 SolutionsДокумент7 страницBoardPaper 2019 Solutionskartik 011Оценок пока нет

- Paper5 SolutionДокумент20 страницPaper5 SolutionArjun ThawaniОценок пока нет

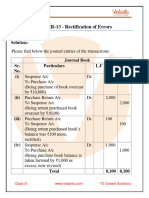

- TS Grewal Solution For Class 11 Accountancy Chapter 13 - Rectification of ErrorsДокумент7 страницTS Grewal Solution For Class 11 Accountancy Chapter 13 - Rectification of ErrorssharoonfaruОценок пока нет

- Zq2.Change in Profit Sharing Ratio of The ExistingДокумент20 страницZq2.Change in Profit Sharing Ratio of The ExistingAaditya SaratheОценок пока нет

- Fa2 Assignment - Ic201248Документ7 страницFa2 Assignment - Ic201248Lavisha GoyalОценок пока нет

- Sujeet Sjuje BktesДокумент13 страницSujeet Sjuje BktesPawan TalrejaОценок пока нет

- Master of Business Administration - MBA Semester 1Документ7 страницMaster of Business Administration - MBA Semester 1Rajesh MishraОценок пока нет

- 2020-BPS - Pre - Board II-Accountancy Answer KeyДокумент16 страниц2020-BPS - Pre - Board II-Accountancy Answer KeyJoshi DrcpОценок пока нет

- Partnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Документ8 страницPartnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Shreyash JhaОценок пока нет

- FA Book ProblemДокумент8 страницFA Book ProblemPhuntru PhiОценок пока нет

- Accountancy 2008Документ23 страницыAccountancy 2008Piyush SrivastavaОценок пока нет

- CBSE Class XI Accountancy - Rectification of ErrorДокумент3 страницыCBSE Class XI Accountancy - Rectification of ErrorYash GuptaОценок пока нет

- Performance of Contract PDFДокумент18 страницPerformance of Contract PDFPrabhakar DashОценок пока нет

- Nagraj ComicsДокумент26 страницNagraj ComicsPrabhakar DashОценок пока нет

- CA Foundation Eco & BCK + Key-7-14Документ8 страницCA Foundation Eco & BCK + Key-7-14Prabhakar DashОценок пока нет

- Unit 2: Basic Problems of An Economy and Role of Price MechanismДокумент14 страницUnit 2: Basic Problems of An Economy and Role of Price MechanismPrabhakar DashОценок пока нет

- Unit 2: Basic Problems of An Economy and Role of Price MechanismДокумент14 страницUnit 2: Basic Problems of An Economy and Role of Price MechanismPrabhakar DashОценок пока нет

- Organizations Facilitating Business PDFДокумент24 страницыOrganizations Facilitating Business PDFPrabhakar DashОценок пока нет

- Mark Scheme - SERIES 2-2015 Results - ASE3003 Level 3Документ12 страницMark Scheme - SERIES 2-2015 Results - ASE3003 Level 3Aung Zaw Htwe0% (1)

- Sudima Spells Subtle Class: Hum, Tum & Humm FMДокумент32 страницыSudima Spells Subtle Class: Hum, Tum & Humm FMIndian WeekenderОценок пока нет

- 4TPD Tentative Costs - Cashew Processing UnitДокумент2 страницы4TPD Tentative Costs - Cashew Processing UnitNitish ShahОценок пока нет

- FCNR (B) LoansДокумент12 страницFCNR (B) LoansGeorgeОценок пока нет

- F4zwe 2013 Jun AДокумент19 страницF4zwe 2013 Jun AJoel GwenereОценок пока нет

- Report On Home Loan Process in Different Financial Institutions of NepalДокумент31 страницаReport On Home Loan Process in Different Financial Institutions of NepalDipesh PandeyОценок пока нет

- Asset RefundДокумент4 страницыAsset RefundKamal GuptaОценок пока нет

- VRDCCДокумент5 страницVRDCCJansi RaniОценок пока нет

- FM Skill Based Questions - 2Документ2 страницыFM Skill Based Questions - 2rohitcshettyОценок пока нет

- Financial Markets and InstrumentДокумент30 страницFinancial Markets and InstrumentAbdul Fattaah Bakhsh 1837065Оценок пока нет

- Fair Practice CodeДокумент9 страницFair Practice CodekrishnaОценок пока нет

- Industrial Court 2016 22Документ9 страницIndustrial Court 2016 22Juma KavesuОценок пока нет

- Trends and Determinants of Investment - UNCTAD 1998Документ445 страницTrends and Determinants of Investment - UNCTAD 1998Bui Thu HaОценок пока нет

- Project On KFCДокумент24 страницыProject On KFCAk Abhi KhannaОценок пока нет

- FTG Irs Form 990 2005Документ17 страницFTG Irs Form 990 2005L. A. PatersonОценок пока нет

- Account Statement: Please Detach and Return This Portion Together With Your PaymentsДокумент1 страницаAccount Statement: Please Detach and Return This Portion Together With Your Paymentsalotfya2236Оценок пока нет

- Internship Report On Customer Satisfaction and General Operations of Rupali BankДокумент43 страницыInternship Report On Customer Satisfaction and General Operations of Rupali BankjaiontyОценок пока нет

- Leac202 DebenturesДокумент75 страницLeac202 DebenturesMidhunidharОценок пока нет

- Zarai Taraqiati Bank LimitedДокумент22 страницыZarai Taraqiati Bank LimitedHawkBravo786100% (10)

- Leasing and Asset Finance: Fourth EditionДокумент1 страницаLeasing and Asset Finance: Fourth Editionahong100Оценок пока нет

- Sip Report On Income Tax Planning With Respect To Individual AssesseeДокумент26 страницSip Report On Income Tax Planning With Respect To Individual AssesseeAlok SinghОценок пока нет

- CKH Industrial Development v. CA (1997)Документ6 страницCKH Industrial Development v. CA (1997)Fides DamascoОценок пока нет

- Chap 007Документ27 страницChap 007Xeniya Morozova Kurmayeva100% (6)

- News - Bulletin: Best in BelenДокумент22 страницыNews - Bulletin: Best in BelenVCNews-BulletinОценок пока нет