Вам также может понравиться

- Editha M. Donoso: Personal InformationДокумент2 страницыEditha M. Donoso: Personal InformationArianeMaeT.RicaboОценок пока нет

- Assignment 2Документ675 страницAssignment 2ArianeMaeT.RicaboОценок пока нет

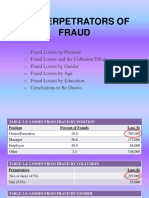

- The Perpetrators of FraudДокумент20 страницThe Perpetrators of FraudArianeMaeT.RicaboОценок пока нет

- Name: Enumeration. 11-12. Benefits of Quality Management ControlДокумент1 страницаName: Enumeration. 11-12. Benefits of Quality Management ControlArianeMaeT.RicaboОценок пока нет

- BA328quiz ArianeДокумент1 страницаBA328quiz ArianeArianeMaeT.RicaboОценок пока нет

- The Perpetrators of FraudДокумент20 страницThe Perpetrators of FraudArianeMaeT.RicaboОценок пока нет

- List of ISO Standards PDFДокумент20 страницList of ISO Standards PDFKristal Newton80% (5)

- ILLUSTRATIONSДокумент2 страницыILLUSTRATIONSArianeMaeT.RicaboОценок пока нет

- Acctg 211Документ2 страницыAcctg 211LumongtadJoanMaeОценок пока нет

- BA328quiz ArianeДокумент1 страницаBA328quiz ArianeArianeMaeT.RicaboОценок пока нет

- Number Messages Handbook 2019Документ25 страницNumber Messages Handbook 2019ArianeMaeT.Ricabo100% (1)

- Modifiers of Human ActsДокумент2 страницыModifiers of Human ActsJe Rah MaligdongОценок пока нет

- Optimize Process Analysis for Improved EfficiencyДокумент33 страницыOptimize Process Analysis for Improved EfficiencyArianeMaeT.RicaboОценок пока нет

- Name: Enumeration. 11-12. Benefits of Quality Management ControlДокумент1 страницаName: Enumeration. 11-12. Benefits of Quality Management ControlArianeMaeT.RicaboОценок пока нет

- IllustrationsДокумент2 страницыIllustrationsArianeMaeT.RicaboОценок пока нет

- Chapter 10 Question ReviewДокумент11 страницChapter 10 Question ReviewHípPôОценок пока нет

- 8 Secrets of The Truly Rich-Bo SanchezДокумент213 страниц8 Secrets of The Truly Rich-Bo Sanchezundefined_lilai100% (13)

- 8 Secrets of The Truly Rich-Bo SanchezДокумент213 страниц8 Secrets of The Truly Rich-Bo Sanchezundefined_lilai100% (13)

- 29 - Liabilities - TheoryДокумент5 страниц29 - Liabilities - Theoryjaymark canayaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- RoBA MultiplierДокумент3 страницыRoBA Multipliersai krishna boyapati100% (1)

- 21-01-01 Ericsson v. Samsung EDTX New ComplaintДокумент22 страницы21-01-01 Ericsson v. Samsung EDTX New ComplaintFlorian Mueller100% (1)

- How To Calculate Invoice ERV in Actual Cost Transactions ViewДокумент2 страницыHow To Calculate Invoice ERV in Actual Cost Transactions ViewMuhammad TabraniОценок пока нет

- Assg Normalization QuestionДокумент3 страницыAssg Normalization QuestionRuby LeeОценок пока нет

- Lmu-800™ Hardware and Installation Guide: Calamp Proprietary & ConfidentialДокумент43 страницыLmu-800™ Hardware and Installation Guide: Calamp Proprietary & ConfidentialEDVANDROОценок пока нет

- Syllabus - Data Mining Solution With WekaДокумент5 страницSyllabus - Data Mining Solution With WekaJaya WijayaОценок пока нет

- Installation - Manual KX-TVM 200Документ248 страницInstallation - Manual KX-TVM 200SERVICE CENTER PABX 085289388205Оценок пока нет

- MT 9 I7Документ49 страницMT 9 I7Michel MüllerОценок пока нет

- Flowchart of NCR Via AconexДокумент1 страницаFlowchart of NCR Via AconexCristian GiurgeaОценок пока нет

- R-PLS Path Modeling ExampleДокумент8 страницR-PLS Path Modeling ExamplemagargieОценок пока нет

- JaiДокумент2 страницыJaijayanthimathesОценок пока нет

- NX CAD The Pinnacle of Computer Aided DesignДокумент3 страницыNX CAD The Pinnacle of Computer Aided DesignLijithОценок пока нет

- CS 301 Algorithms Course SyllabusДокумент3 страницыCS 301 Algorithms Course SyllabusAhmad TaqiyuddinОценок пока нет

- Lab 9-The C# Station ADO - Net TutorialДокумент11 страницLab 9-The C# Station ADO - Net TutorialHector Felipe Calla MamaniОценок пока нет

- Narrative Report ICTДокумент2 страницыNarrative Report ICTPhil LajomОценок пока нет

- ECE 391 Exam 1, Spring 2016 SolutionsДокумент18 страницECE 391 Exam 1, Spring 2016 SolutionsJesse ChenОценок пока нет

- 10.1007@978 981 15 7984 4Документ666 страниц10.1007@978 981 15 7984 4บักนัด ผู้วิ่งจะสลายไขมันОценок пока нет

- Rapid Problem Resolution (RPR) ExplainedДокумент12 страницRapid Problem Resolution (RPR) Explainedaks1995Оценок пока нет

- Fitness Center 1 Cs Practical For Class 12Документ13 страницFitness Center 1 Cs Practical For Class 12aeeeelvishbhaiiОценок пока нет

- Login - Ufone Technical Department - Login Creation - Access - Form - HammadДокумент1 страницаLogin - Ufone Technical Department - Login Creation - Access - Form - HammadhammadОценок пока нет

- Resume RedditДокумент1 страницаResume Redditr3s2o8Оценок пока нет

- Job Description - Product Delivery ManagerДокумент1 страницаJob Description - Product Delivery ManagerYoshua GaloenkОценок пока нет

- Bootloading The TMS320VC5402 in HPI Mode: Scott Tater DSP Applications - Semiconductor GroupДокумент11 страницBootloading The TMS320VC5402 in HPI Mode: Scott Tater DSP Applications - Semiconductor GroupGigi IonОценок пока нет

- APM - 9.5 Cross Enterprise Integration GuideДокумент194 страницыAPM - 9.5 Cross Enterprise Integration Guideggen_mail.ruОценок пока нет

- Chapter 8: Central Processing Unit: Cpe 252: Computer Organization 1Документ30 страницChapter 8: Central Processing Unit: Cpe 252: Computer Organization 1Tanvi SharmaОценок пока нет

- Fastcase User GuideДокумент9 страницFastcase User Guideapi-1281913Оценок пока нет

- BIM Execution Plan (PDFDrive)Документ276 страницBIM Execution Plan (PDFDrive)BranZzZzZ100% (1)

- 01 NI Course Unit 7Документ9 страниц01 NI Course Unit 7Eric Suva BacunawaОценок пока нет

- PC Technical Reference Aug81Документ396 страницPC Technical Reference Aug81kgrhoadsОценок пока нет