Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Earn More With An Industry Recognised Bookkeeping Qualification!Документ11 страницEarn More With An Industry Recognised Bookkeeping Qualification!Lilia0% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

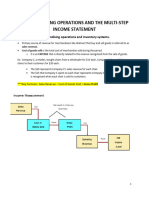

- Multi-Stepped Income Statement DirectionsДокумент4 страницыMulti-Stepped Income Statement DirectionsMary92% (12)

- Ttwo - Equity Research ReportДокумент40 страницTtwo - Equity Research Reportapi-523877663Оценок пока нет

- EStatement PDFДокумент4 страницыEStatement PDFLilia75% (4)

- Statement of Comprehensive IncomeДокумент23 страницыStatement of Comprehensive IncomeAbdulmajed Unda MimbantasОценок пока нет

- Working Capital Simulation - Managing Growth - Sunflower Nutraceuticals Harvard Case StudyДокумент4 страницыWorking Capital Simulation - Managing Growth - Sunflower Nutraceuticals Harvard Case Studyalka murarka67% (3)

- SAP FICO Vs SAP S4 HANA FINANCEДокумент34 страницыSAP FICO Vs SAP S4 HANA FINANCEsmart srini100% (2)

- Art. 11 2017 Redobandire PDFДокумент2 194 страницыArt. 11 2017 Redobandire PDFLilia100% (1)

- CB 56Документ4 страницыCB 56LiliaОценок пока нет

- Purchases Register Form PDFДокумент1 страницаPurchases Register Form PDFLiliaОценок пока нет

- Purchase Order Form Template PDFДокумент1 страницаPurchase Order Form Template PDFLiliaОценок пока нет

- ACCOUNTS RECEIVABLES FORM Business Name: - Date: - Customer Name Balance OwingДокумент1 страницаACCOUNTS RECEIVABLES FORM Business Name: - Date: - Customer Name Balance OwingLiliaОценок пока нет

- CA La RestaurantДокумент41 страницаCA La RestaurantLiliaОценок пока нет

- Aliona Vesca CVДокумент2 страницыAliona Vesca CVLiliaОценок пока нет

- SEM 6 - 10 - BCom - HONS - COMMERCE - DSE 61A - FINANCIAL REPORTING AND FINANCIAL STATEMENT ANALYSIS - 10297Документ5 страницSEM 6 - 10 - BCom - HONS - COMMERCE - DSE 61A - FINANCIAL REPORTING AND FINANCIAL STATEMENT ANALYSIS - 10297Aaysha AgrawalОценок пока нет

- Accounting ErrorssДокумент5 страницAccounting ErrorssJuvilynОценок пока нет

- Revision No AnswerДокумент12 страницRevision No AnswerQuang Nguyễn ThếОценок пока нет

- Financial Accounting AssignmentДокумент23 страницыFinancial Accounting Assignmentyared0% (1)

- Multiple Choice Answers and Solutions: Franchise Accounting 177Документ11 страницMultiple Choice Answers and Solutions: Franchise Accounting 177Mazikeen DeckerОценок пока нет

- Report On Schedule VI - Part 1 & 2Документ75 страницReport On Schedule VI - Part 1 & 2md1586Оценок пока нет

- Accounting For Training Merchandising BusinessДокумент109 страницAccounting For Training Merchandising BusinessIsa NgОценок пока нет

- Sample Question Paper-Ii Accountancy Class Xii Maximum Marks: 80 Time Allowed: 3 Hrs. General InstructionsДокумент38 страницSample Question Paper-Ii Accountancy Class Xii Maximum Marks: 80 Time Allowed: 3 Hrs. General Instructionsmohit pandeyОценок пока нет

- Unity University College School of Distance and Continuing Education Worksheet For Advanced Accounting I (Acct 401)Документ4 страницыUnity University College School of Distance and Continuing Education Worksheet For Advanced Accounting I (Acct 401)Sisay Tesfaye100% (2)

- Hapter: Need For Cost AccountingДокумент28 страницHapter: Need For Cost AccountingAhamed WajidОценок пока нет

- Chapter 2 Business Management and Accounting Basics - 2Документ88 страницChapter 2 Business Management and Accounting Basics - 2Kirththi PriyaОценок пока нет

- Forest City Tennis Club Pro Shop and BarДокумент18 страницForest City Tennis Club Pro Shop and BarShubham JhaОценок пока нет

- Report On Common Size StatementДокумент12 страницReport On Common Size StatementMahi Salman Thawer0% (1)

- CFAP 1 AAFR Summer 2017Документ10 страницCFAP 1 AAFR Summer 2017Aqib SheikhОценок пока нет

- Chapter 5 SummaryДокумент10 страницChapter 5 Summarymyhan20144Оценок пока нет

- Solved at The Beginning of 2015 Mansen PLC Acquired Equipment CostingДокумент1 страницаSolved at The Beginning of 2015 Mansen PLC Acquired Equipment CostingDoreenОценок пока нет

- Nama: Rina Elizabeth Ritonga NIM: 2001677595 Tugas Personal Ke - (1) Minggu 2Документ6 страницNama: Rina Elizabeth Ritonga NIM: 2001677595 Tugas Personal Ke - (1) Minggu 2GKB CGIC PALEMBANGОценок пока нет

- PDF 14 Pengantar AkunДокумент58 страницPDF 14 Pengantar AkunPeony Risha Mulyadi PutriОценок пока нет

- Ca Inter Accounting Full Test 1 Nov 2022 Unschedule Solution 1658223005Документ40 страницCa Inter Accounting Full Test 1 Nov 2022 Unschedule Solution 1658223005Shashank SikarwarОценок пока нет

- Ma. Acctng.Документ7 страницMa. Acctng.Kaname KuranОценок пока нет

- Tree Melaty Silaban (1610631030282) FixДокумент40 страницTree Melaty Silaban (1610631030282) Fixafnugraini100% (1)

- FAR04 01.4 Interim ReportingДокумент9 страницFAR04 01.4 Interim Reportingnicole bancoroОценок пока нет

- Angang 2013 2hДокумент231 страницаAngang 2013 2hHenry So E DiarkoОценок пока нет

- ch04 SolДокумент16 страницch04 SolJohn Nigz PayeeОценок пока нет

- Far ReviewerДокумент4 страницыFar Reviewerjessamae gundanОценок пока нет