Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- OMB Circular A-133 Compliance Supplement 2009Документ1 049 страницOMB Circular A-133 Compliance Supplement 2009Beverly Tran100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Due Diligence and Potential LiabilitiesДокумент42 страницыDue Diligence and Potential LiabilitiesUPPARAANJANEYULUОценок пока нет

- Framework of Financial Statement AuditДокумент56 страницFramework of Financial Statement AuditHanna Bayot100% (1)

- Auditing McqsДокумент27 страницAuditing McqsGhulam Abbas100% (5)

- Business Administration Project Topics and MaterialsДокумент47 страницBusiness Administration Project Topics and MaterialsProject Championz100% (1)

- Auditing final preboard since 1977Документ7 страницAuditing final preboard since 1977Floriza Cuevas Ragudo100% (1)

- Rofo 2018 ArДокумент18 страницRofo 2018 ArNate TobikОценок пока нет

- Auditing Theory - 2Документ11 страницAuditing Theory - 2Kageyama HinataОценок пока нет

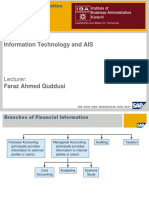

- Role of AISДокумент20 страницRole of AISFaraz Ahmed QuddusiОценок пока нет

- Senior Internal Auditor Job DescriptionДокумент1 страницаSenior Internal Auditor Job DescriptionozlemОценок пока нет

- Management Functions & Leadership StylesДокумент80 страницManagement Functions & Leadership StylesAkshitha KulalОценок пока нет

- COSCO FrameworkДокумент70 страницCOSCO Frameworkbarakkat72Оценок пока нет

- Auditing ReviewerДокумент8 страницAuditing ReviewerSeanaОценок пока нет

- 03 G3 Annexure B - OR Self Assessment TemplateДокумент8 страниц03 G3 Annexure B - OR Self Assessment TemplateTejendrasinh GohilОценок пока нет

- ACCAДокумент6 страницACCA1099 DevanshОценок пока нет

- Internal Control System and Financial Performance in Financial Institutions in Rwanda: A Case of I & M Bank LTD RwandaДокумент14 страницInternal Control System and Financial Performance in Financial Institutions in Rwanda: A Case of I & M Bank LTD Rwandanazif hamdaniОценок пока нет

- Cic ReflectionДокумент3 страницыCic ReflectionRenz Mari AcuñaОценок пока нет

- Implementing Good Corporate GovernanceДокумент91 страницаImplementing Good Corporate GovernanceSalman Kabir AbidОценок пока нет

- Danaharta Annual Report 2000Документ136 страницDanaharta Annual Report 2000az1972100% (2)

- Course Catalog: January - December 2019Документ68 страницCourse Catalog: January - December 2019islamelshahatОценок пока нет

- No 7Документ19 страницNo 7marthinaОценок пока нет

- Overview of Insurance Industry of BanglaДокумент20 страницOverview of Insurance Industry of BanglamR. sLimОценок пока нет

- Module 5 Aud SpecializedДокумент7 страницModule 5 Aud SpecializedAnonymityОценок пока нет

- Directors Report As Per Section 134 (3) - 31122021Документ4 страницыDirectors Report As Per Section 134 (3) - 31122021SHIKHA SHARMAОценок пока нет

- Internal Controls in A CIS EnvironmentДокумент18 страницInternal Controls in A CIS EnvironmenthasanuОценок пока нет

- Maybank Integrated AR 2023 - Part 2Документ123 страницыMaybank Integrated AR 2023 - Part 2yennielimclОценок пока нет

- Auditing Theory - Key Concepts and Financial Statement AssertionsДокумент11 страницAuditing Theory - Key Concepts and Financial Statement AssertionsJeric TorionОценок пока нет

- Solomon Kebede and Wondwosen, AbrehamДокумент15 страницSolomon Kebede and Wondwosen, AbrehamSolomon Kebede MenzaОценок пока нет

- ESL Steel Limited Annual Report 2020-21 HighlightsДокумент83 страницыESL Steel Limited Annual Report 2020-21 HighlightsPiyush Ashokchand ChopdaОценок пока нет

- Jindal Saw-AR-2017-18-NET PDFДокумент274 страницыJindal Saw-AR-2017-18-NET PDFshahavОценок пока нет