Вам также может понравиться

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionОт EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionОценок пока нет

- Economic Indicators for East Asia: Input–Output TablesОт EverandEconomic Indicators for East Asia: Input–Output TablesОценок пока нет

- GDP growth plunges to 5% lowest in 25 quartersДокумент2 страницыGDP growth plunges to 5% lowest in 25 quartersSanjoySahaОценок пока нет

- Pakistan's Economic Crisis Eased in FY2009 But Inflation and Growth Remained ProblemsДокумент6 страницPakistan's Economic Crisis Eased in FY2009 But Inflation and Growth Remained Problemskiran-mahmood-6943Оценок пока нет

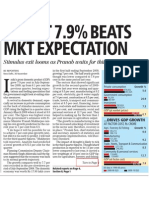

- GDP at 7.9%Документ1 страницаGDP at 7.9%soumyaranjan_d3393Оценок пока нет

- GDP For 1st QuarterДокумент5 страницGDP For 1st QuarterUmesh MatkarОценок пока нет

- KBSV - Macro Outlook 2Q - 2019Документ16 страницKBSV - Macro Outlook 2Q - 2019LinhОценок пока нет

- Industry and Infrastructure: Rends in Ndustrial EctorДокумент45 страницIndustry and Infrastructure: Rends in Ndustrial EctorRajeev DudiОценок пока нет

- India International Trade Investment Website June 2022Документ18 страницIndia International Trade Investment Website June 2022vinay jodОценок пока нет

- Fibank Albania Annual Report 2019 083685f7fdДокумент141 страницаFibank Albania Annual Report 2019 083685f7fdKarolina MusagalliuОценок пока нет

- Country Economic Forecasts - VietnamДокумент7 страницCountry Economic Forecasts - Vietnamthanhphong17vnОценок пока нет

- Data - File Warehousing Space Absorption Grows 60 in January June 2015 Report 1441006412Документ14 страницData - File Warehousing Space Absorption Grows 60 in January June 2015 Report 1441006412Shivangi KumarОценок пока нет

- Dgp2023 Ceat LimitedДокумент34 страницыDgp2023 Ceat Limited24812Оценок пока нет

- 40 Bangladesh CiplaДокумент9 страниц40 Bangladesh CiplaPartho MukherjeeОценок пока нет

- Qb23q3 en Ch2Документ5 страницQb23q3 en Ch2milvibesupplyОценок пока нет

- Monthly Bulletin July 2023 EnglishДокумент13 страницMonthly Bulletin July 2023 EnglishNirmal MenonОценок пока нет

- PC Insurance Trends 2019Документ28 страницPC Insurance Trends 2019Kabuiku Ngelesi AndréОценок пока нет

- Comprehensive Report On Indian Metal Cutting Machine Tool Industry - 2019Документ73 страницыComprehensive Report On Indian Metal Cutting Machine Tool Industry - 2019Dr-Prashanth GowdaОценок пока нет

- US Private Sector Productivity Increased 3.2% in 2021Документ12 страницUS Private Sector Productivity Increased 3.2% in 2021Preeti KalkalОценок пока нет

- Tracing_The_Business_Cycle_Of_India_Since_The_Pandemic _Документ15 страницTracing_The_Business_Cycle_Of_India_Since_The_Pandemic _sappyyadav1297Оценок пока нет

- Q4 Fy21 GDPДокумент7 страницQ4 Fy21 GDPsksaha1976Оценок пока нет

- 03 IAG 1H23 Financial ResultsДокумент6 страниц03 IAG 1H23 Financial ResultsMarvin SwaminathanОценок пока нет

- 2018 CippДокумент2 страницы2018 Cippva.manikanОценок пока нет

- State of Pakistan EconomyДокумент8 страницState of Pakistan EconomyMuhammad KashifОценок пока нет

- SocGen - On Our Minds (China) 12152021Документ9 страницSocGen - On Our Minds (China) 12152021irvinkuanОценок пока нет

- Jobless GrowthДокумент13 страницJobless GrowthApurva JhaОценок пока нет

- Wipro LTD: Profitable Growth Focus of New CEOДокумент11 страницWipro LTD: Profitable Growth Focus of New CEOPramod KulkarniОценок пока нет

- The Connect Q1 2020Документ35 страницThe Connect Q1 2020Vipin SОценок пока нет

- Budget Analysis: 2009-2010Документ11 страницBudget Analysis: 2009-2010Waseem IshfaqОценок пока нет

- State of The Economy and Prospects: CivilsexpertДокумент20 страницState of The Economy and Prospects: CivilsexpertThavaseelan KarunanidhyОценок пока нет

- WPP - 2022 Q3 Results - Presentation - FINALДокумент26 страницWPP - 2022 Q3 Results - Presentation - FINALpete meyerОценок пока нет

- Viet Nam Market Pulse - Shared by WorldLine Technology-1Документ21 страницаViet Nam Market Pulse - Shared by WorldLine Technology-1CHIÊM HÀОценок пока нет

- Philippine Economic Updates May 2023Документ2 страницыPhilippine Economic Updates May 2023regina.bumatayОценок пока нет

- Market Review - March 2024 (Yearly Update)Документ9 страницMarket Review - March 2024 (Yearly Update)Akshay ChaudhryОценок пока нет

- CDB Economic Brief 2018 - Saint LuciaДокумент6 страницCDB Economic Brief 2018 - Saint LuciaJesse PembertonОценок пока нет

- Echap01 Vol2 PDFДокумент35 страницEchap01 Vol2 PDFPASUPULA JAGADEESHОценок пока нет

- Manufacturing and MiningДокумент20 страницManufacturing and MiningShehroz ShyziОценок пока нет

- Covid-19 Advent and Impact Assessment: Annex-IIIДокумент8 страницCovid-19 Advent and Impact Assessment: Annex-IIIAsaad AreebОценок пока нет

- Singapore EconomyДокумент11 страницSingapore EconomyK60 Nguyễn Thúy HoàОценок пока нет

- India's Economic Growth Surges to 11.2% in Q1 Despite Slowdown RisksДокумент2 страницыIndia's Economic Growth Surges to 11.2% in Q1 Despite Slowdown Risksshailesh_4Оценок пока нет

- India Economic Update June 23 2010Документ25 страницIndia Economic Update June 23 2010Ning Ning Intan PermataОценок пока нет

- Ok Macro IndiaДокумент22 страницыOk Macro IndiaSaurabh JadhavОценок пока нет

- Jurnal INTERNASIONAL 2Документ8 страницJurnal INTERNASIONAL 2joonner rambeОценок пока нет

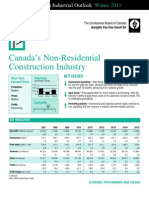

- Canada's Non-Residential Construction Industry: Key IssuesДокумент10 страницCanada's Non-Residential Construction Industry: Key IssuesSteve LadurantayeОценок пока нет

- Public Finances: Table 4.1: Stimulus Packages (Est.) Country USD (Billions)Документ15 страницPublic Finances: Table 4.1: Stimulus Packages (Est.) Country USD (Billions)Usman YousafОценок пока нет

- France 2019 OECD Economic Survey OverviewДокумент66 страницFrance 2019 OECD Economic Survey OverviewAntónio J. CorreiaОценок пока нет

- Economic Outlook: 1.1 OverviewДокумент12 страницEconomic Outlook: 1.1 OverviewMuhammad AbrarОценок пока нет

- The Stories Numbers Tell: Understanding Key Economic IndicatorsДокумент22 страницыThe Stories Numbers Tell: Understanding Key Economic IndicatorsreiiОценок пока нет

- Thesun 2009-05-28 Page16 Economy Contracts by 6Документ1 страницаThesun 2009-05-28 Page16 Economy Contracts by 6Impulsive collectorОценок пока нет

- Ambuja Cement: Volume Push Drives Topline Maintain HOLDДокумент9 страницAmbuja Cement: Volume Push Drives Topline Maintain HOLDanjugaduОценок пока нет

- Management: Discussion and AnalysisДокумент20 страницManagement: Discussion and AnalysisSiva MohanОценок пока нет

- Impact of COVID-19 on the Economy Hinges on Private InvestmentДокумент9 страницImpact of COVID-19 on the Economy Hinges on Private InvestmentTavish SettОценок пока нет

- National Output Income ExpenДокумент40 страницNational Output Income ExpenImanthi AnuradhaОценок пока нет

- Roland Berger Automotive ResearchДокумент20 страницRoland Berger Automotive ResearchHiifjxjОценок пока нет

- Budget 2018-19: Highlights & CommentsДокумент72 страницыBudget 2018-19: Highlights & CommentsShahidОценок пока нет

- CY Draft Budgetary Plan 2019Документ40 страницCY Draft Budgetary Plan 2019attikourisОценок пока нет

- Consumer - Outlook - 3jan22 - JM FinancialДокумент14 страницConsumer - Outlook - 3jan22 - JM FinancialBinoy JariwalaОценок пока нет

- India: Economy Treading On Thin IceДокумент12 страницIndia: Economy Treading On Thin IceTodkarSachinОценок пока нет

- Gatere: Delhi NCR Office MarketДокумент13 страницGatere: Delhi NCR Office MarketPrateek MathurОценок пока нет

- India - Country OverviewДокумент2 страницыIndia - Country OverviewVivekanandОценок пока нет

- RTLSДокумент8 страницRTLSprincy.kumar8568Оценок пока нет

- Selling The Wheel SummaryДокумент10 страницSelling The Wheel Summaryprincy.kumar8568Оценок пока нет

- Demand For MoneyДокумент1 страницаDemand For Moneyprincy.kumar8568Оценок пока нет

- Haigh's ChocolatesДокумент1 страницаHaigh's Chocolatesprincy.kumar8568Оценок пока нет

- 471 Review Confectionery in RussiaДокумент32 страницы471 Review Confectionery in Russiaprincy.kumar8568Оценок пока нет

- Student Entrepreneurship: Leading Tomorrow's GrowthДокумент3 страницыStudent Entrepreneurship: Leading Tomorrow's Growthprincy.kumar8568Оценок пока нет

- Haigh's ChocolatesДокумент1 страницаHaigh's Chocolatesprincy.kumar8568Оценок пока нет

- Financial ManagementДокумент201 страницаFinancial Managementprashanth kОценок пока нет

- NelpДокумент27 страницNelpkhandelwalnakulОценок пока нет

- Name: Section: Date: Score: Long Exam On Non-Profit Organization and Business CombinationДокумент2 страницыName: Section: Date: Score: Long Exam On Non-Profit Organization and Business CombinationLiezelОценок пока нет

- Suzlon Energy Call TranscriptДокумент19 страницSuzlon Energy Call TranscriptKishor TilokaniОценок пока нет

- DISSERTATION RE NikhilДокумент37 страницDISSERTATION RE NikhilNikhil Ranjan50% (2)

- New Microsoft Word DocumentДокумент10 страницNew Microsoft Word DocumentMukit-Ul Hasan PromitОценок пока нет

- Course Revision: Corporate Finance 1Документ4 страницыCourse Revision: Corporate Finance 1Foisal Ahmed MirzaОценок пока нет

- Shirkah, Musharkah and Types of Shirkah: Introduct IonДокумент5 страницShirkah, Musharkah and Types of Shirkah: Introduct Ionabsiddique11Оценок пока нет

- Dissertation Main - Risk Management in BanksДокумент87 страницDissertation Main - Risk Management in Banksjesenku100% (1)

- The General Structure of the Patrimony in the New Civil CodeДокумент12 страницThe General Structure of the Patrimony in the New Civil CodeVasile SoltanОценок пока нет

- 03 Cash Flow Balance SheetsДокумент16 страниц03 Cash Flow Balance SheetsPavan Kumar MylavaramОценок пока нет

- Damodaran On RiskДокумент106 страницDamodaran On Riskgioro_mi100% (1)

- Mathematics of Finance Revision 1Документ31 страницаMathematics of Finance Revision 1Firyal Yulda100% (1)

- Module 1 ExamДокумент22 страницыModule 1 ExamRoger Chivas100% (1)

- MGM 3101 Case StudyДокумент8 страницMGM 3101 Case StudyNurul Ashikin ZulkefliОценок пока нет

- The Cost of Capital Components and WACCДокумент1 страницаThe Cost of Capital Components and WACCMariam TariqОценок пока нет

- Inland Revenue Board Malaysia: Employee Share Scheme BenefitДокумент35 страницInland Revenue Board Malaysia: Employee Share Scheme Benefit123dddОценок пока нет

- Super Investors of IndiaДокумент71 страницаSuper Investors of IndiasameerОценок пока нет

- ch12 BaruДокумент28 страницch12 BaruIrvan Syafiq NurhabibieОценок пока нет

- PresentationДокумент12 страницPresentationJoachim Dip GomesОценок пока нет

- Little Black Book of Options Secrets AbДокумент12 страницLittle Black Book of Options Secrets AbRaju.KonduruОценок пока нет

- Financial Statement Analysis of BHELДокумент18 страницFinancial Statement Analysis of BHELRatna Prashanth KОценок пока нет

- Cox-Ross-Rubenstein Binomial OptionДокумент4 страницыCox-Ross-Rubenstein Binomial Optionhotmail13Оценок пока нет

- PDF File JournalДокумент5 страницPDF File Journalritesh rachnalifestyleОценок пока нет

- Market TablesДокумент18 страницMarket TablesallegreОценок пока нет

- Financial Accounting: 16Th EditionДокумент31 страницаFinancial Accounting: 16Th EditionZooni FatimaОценок пока нет

- Diocaneeeeeee HSBC Bank PLC WordДокумент1 страницаDiocaneeeeeee HSBC Bank PLC Wordmvrht100% (1)

- Chapter 8Документ24 страницыChapter 8Cynthia AdiantiОценок пока нет

- Mokoagouw, Angie Lisy (Advance Problem Chapter 1)Документ14 страницMokoagouw, Angie Lisy (Advance Problem Chapter 1)AngieОценок пока нет

- List of Investment BanksДокумент10 страницList of Investment BanksSKNYUYОценок пока нет