Вам также может понравиться

- Book 1Документ104 страницыBook 1Naila MehboobОценок пока нет

- Feasibility Report Opening of CIIT Sub Campus in AbbottabadДокумент2 страницыFeasibility Report Opening of CIIT Sub Campus in AbbottabadNaila Mehboob100% (1)

- Memo WritingДокумент3 страницыMemo WritingNaila Mehboob100% (1)

- The Bank of KhyberДокумент15 страницThe Bank of KhyberNaila Mehboob100% (2)

- Telenor Nafisa Interview ReportДокумент7 страницTelenor Nafisa Interview ReportNaila MehboobОценок пока нет

- Impact of Performance Appraisal System On Employee Productivity in Telecom Sector of PakistanДокумент7 страницImpact of Performance Appraisal System On Employee Productivity in Telecom Sector of PakistanNaila MehboobОценок пока нет

- Emotional Intelligence White PaperДокумент10 страницEmotional Intelligence White PaperNaila MehboobОценок пока нет

- Thesis Literature DataДокумент492 страницыThesis Literature DataNaila Mehboob100% (1)

- List of Tables and Figures Page NoДокумент12 страницList of Tables and Figures Page NoNaila MehboobОценок пока нет

- List of Tables and Figures Page NoДокумент18 страницList of Tables and Figures Page NoNaila MehboobОценок пока нет

- Reliability, Replication and ValidityДокумент2 страницыReliability, Replication and ValidityNaila MehboobОценок пока нет

- Edmund BurkeДокумент85 страницEdmund BurkeNaila MehboobОценок пока нет

- Bertrand RussellДокумент80 страницBertrand RussellNaila MehboobОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Textiles 2Документ4 страницыTextiles 2Mazine QalbaouiОценок пока нет

- 6.1 and 6.2 - Balance of Payments Accounts & Exchange RatesДокумент5 страниц6.1 and 6.2 - Balance of Payments Accounts & Exchange RatesReed-Animated ProductionsОценок пока нет

- Case StudyДокумент4 страницыCase StudyJahara Obedencio CalaycaОценок пока нет

- 1segunda Entrega Cultura Y Economia Regional de EuropaДокумент5 страниц1segunda Entrega Cultura Y Economia Regional de EuropaMarian CadavidОценок пока нет

- AmBisyon Natin 2040Документ2 страницыAmBisyon Natin 2040TRISTAN CANLAS HERNANDEZОценок пока нет

- Trade and Investment Policies: True/False QuestionsДокумент24 страницыTrade and Investment Policies: True/False QuestionsAshok SubramaniamОценок пока нет

- Xiao Enterprise Payslip Mar15Документ5 страницXiao Enterprise Payslip Mar15D Jay ApostelloОценок пока нет

- GJEPC FinalДокумент21 страницаGJEPC FinalVishal RamrakhyaniОценок пока нет

- TCL Thomsons Electronics CorporationДокумент13 страницTCL Thomsons Electronics CorporationAkshay Kittur100% (1)

- PESCO ONLINE BILL Jan2023Документ2 страницыPESCO ONLINE BILL Jan2023amjadali482Оценок пока нет

- Gahum Barangay-ProfileДокумент2 страницыGahum Barangay-ProfileEmayvelleОценок пока нет

- TYBCOM SEM 5 Export Marketing Nov 2019Документ2 страницыTYBCOM SEM 5 Export Marketing Nov 2019Esha MuruganОценок пока нет

- Ann Julienne Aristoza Income Tax MatrixДокумент5 страницAnn Julienne Aristoza Income Tax MatrixJul A.Оценок пока нет

- Pay Slip For August 2023: Entero Healthcare Solutions LimitedДокумент1 страницаPay Slip For August 2023: Entero Healthcare Solutions Limitedkadamaniket7894Оценок пока нет

- Chapter 21 Problems ECON 212 AUBДокумент4 страницыChapter 21 Problems ECON 212 AUBElio BazОценок пока нет

- Sanand Gidc Company ListДокумент3 страницыSanand Gidc Company ListSomeshwar SwamiОценок пока нет

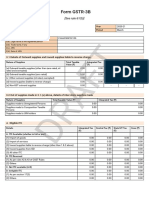

- Form GSTR-3B: (See Rule 61 (5) )Документ2 страницыForm GSTR-3B: (See Rule 61 (5) )Pabitra Kumar PrustyОценок пока нет

- PWD Budget 2019 - bp18Документ76 страницPWD Budget 2019 - bp18amitОценок пока нет

- Asian PaintsДокумент19 страницAsian PaintsAmrita KaurОценок пока нет

- Global Value Chains (GVCS) : BrazilДокумент4 страницыGlobal Value Chains (GVCS) : Braziljorgebritto1Оценок пока нет

- INTERNATIONAL MARKETING MANAGEMENT MilleДокумент9 страницINTERNATIONAL MARKETING MANAGEMENT MilleLamillaОценок пока нет

- BE-4310 Lecture 2 - ASEAN Model of Sustainable DevbelopmentДокумент36 страницBE-4310 Lecture 2 - ASEAN Model of Sustainable Devbelopmentrizallamat06Оценок пока нет

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruДокумент1 страницаIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruProfit MartОценок пока нет

- Dairy Co OperativesДокумент21 страницаDairy Co OperativesWasim KhanОценок пока нет

- Chapter 11 - International TaxationДокумент11 страницChapter 11 - International TaxationlinaelinaaaОценок пока нет

- John Lewis: by Daryl Marden, Deividas Krygeris, Andrejus Barstys, Gurpreet TaqkДокумент10 страницJohn Lewis: by Daryl Marden, Deividas Krygeris, Andrejus Barstys, Gurpreet TaqkAndrejus BarštysОценок пока нет

- Project On International BusinessДокумент13 страницProject On International BusinessShreya JainОценок пока нет

- Acct Statement XX352223062023Документ55 страницAcct Statement XX352223062023Kishore JagarapuОценок пока нет

- Swot Analysis of MDC IncДокумент4 страницыSwot Analysis of MDC IncSunny SunnyОценок пока нет

- Writing Task 1 - Sample Bar ChartДокумент22 страницыWriting Task 1 - Sample Bar ChartOanh OanhОценок пока нет