Вам также может понравиться

- Bond InvestmentДокумент8 страницBond InvestmentMingmiin TeohОценок пока нет

- Understanding Debentures: Key TakeawaysДокумент8 страницUnderstanding Debentures: Key TakeawaysRichard DuniganОценок пока нет

- CAPITAL MARKET (VAC) - AssignmentДокумент9 страницCAPITAL MARKET (VAC) - Assignment22mba221Оценок пока нет

- Various Types of Corporate BondsДокумент7 страницVarious Types of Corporate BondsAbdul LatifОценок пока нет

- Investment Law - PagesДокумент9 страницInvestment Law - PagesAbhilasha RoyОценок пока нет

- E BusinessfinanceДокумент15 страницE BusinessfinanceDipannita RoyОценок пока нет

- 1.2 and Short TermДокумент18 страниц1.2 and Short TermDeeОценок пока нет

- FINMANДокумент50 страницFINMANJanna Hazel Villarino VillanuevaОценок пока нет

- Definition DebenturesДокумент8 страницDefinition DebenturesDipanjan DasОценок пока нет

- Financing Options for Non-ProfitsДокумент14 страницFinancing Options for Non-ProfitsCorolla SedanОценок пока нет

- Sabbir Hossain 111 161 350Документ37 страницSabbir Hossain 111 161 350Sabbir HossainОценок пока нет

- FINANCE MANAGEMENT FIN420 CHP 9Документ38 страницFINANCE MANAGEMENT FIN420 CHP 9Yanty IbrahimОценок пока нет

- Sources of Finance and Capitalization TheoriesДокумент11 страницSources of Finance and Capitalization Theoriespurvang selaniОценок пока нет

- Unit 2Документ11 страницUnit 2POORNA GOYANKA 2123268Оценок пока нет

- Group 4-Treasury Management-MWF 10-11 AMДокумент13 страницGroup 4-Treasury Management-MWF 10-11 AMAshley Garcia100% (1)

- Sources of Capital: Term Structure of FundsДокумент5 страницSources of Capital: Term Structure of FundsRasheed LawalОценок пока нет

- Debenture and BondДокумент7 страницDebenture and BondPiesie AmponsahОценок пока нет

- Basics of Bond With Types & FeaturesДокумент10 страницBasics of Bond With Types & FeaturesradhikaОценок пока нет

- April Roze L. Nudo Bs-Iv Financial Management 2 Quiz-S Finals 2Документ4 страницыApril Roze L. Nudo Bs-Iv Financial Management 2 Quiz-S Finals 2April NudoОценок пока нет

- Money Markets and Capital MarketsДокумент4 страницыMoney Markets and Capital MarketsEmmanuelle RojasОценок пока нет

- Report - FonterraДокумент19 страницReport - FonterraK59 DOAN THANH TAMОценок пока нет

- Bus. Finance 2. Final 2.Документ9 страницBus. Finance 2. Final 2.Gia PorqueriñoОценок пока нет

- Debentures - Meaning, Types, Features, Accounting ExamplesДокумент6 страницDebentures - Meaning, Types, Features, Accounting Examplesfarhadcse30Оценок пока нет

- Non Non Non Non - Current Liabilities Current Liabilities Current Liabilities Current LiabilitiesДокумент93 страницыNon Non Non Non - Current Liabilities Current Liabilities Current Liabilities Current LiabilitiesBantamkak FikaduОценок пока нет

- Financing Decisions 2Документ12 страницFinancing Decisions 2PUTTU GURU PRASAD SENGUNTHA MUDALIARОценок пока нет

- Funding Sources for BusinessesДокумент9 страницFunding Sources for BusinessesAbhishek Kumar100% (1)

- Understanding Equity and Debt FinancingДокумент7 страницUnderstanding Equity and Debt FinancingSindisiwe DlaminiОценок пока нет

- DebentureДокумент9 страницDebenturedrsurendrakumarОценок пока нет

- Valuation of Debt and EquityДокумент8 страницValuation of Debt and EquityhelloОценок пока нет

- Capital StructureДокумент57 страницCapital StructureRao ShekherОценок пока нет

- Sources of Funds: Unit IiДокумент36 страницSources of Funds: Unit IiFara HameedОценок пока нет

- Financial Management and Securities MarketsДокумент6 страницFinancial Management and Securities MarketsKomal RahimОценок пока нет

- Financial MGT NotesДокумент42 страницыFinancial MGT Notes匿匿Оценок пока нет

- DebenturesДокумент16 страницDebenturesJenice Victoria CrastoОценок пока нет

- Definition of Bonds and DebenturesДокумент3 страницыDefinition of Bonds and Debenturesremruata rascalralteОценок пока нет

- Mezzanine Finance ExplainedДокумент8 страницMezzanine Finance ExplainedJyoti Uppal SachdevaОценок пока нет

- Vce ST01 FMДокумент4 страницыVce ST01 FMSourabh ChiprikarОценок пока нет

- AssaignmentДокумент11 страницAssaignmentMaruf HasanОценок пока нет

- Sources of FinanceДокумент17 страницSources of FinanceNikita ParidaОценок пока нет

- Tai Chinh Doanh NghiepДокумент30 страницTai Chinh Doanh Nghiepl NguyenОценок пока нет

- BBA VI TH Sem Financial Institution & MarketsДокумент2 страницыBBA VI TH Sem Financial Institution & MarketsJordan ThapaОценок пока нет

- Sources and Uses of Short-Term and Long-Term FundsДокумент7 страницSources and Uses of Short-Term and Long-Term FundsSyrill Cayetano0% (1)

- Raising finances through debentures and types of debenturesДокумент6 страницRaising finances through debentures and types of debenturesAditya Sawant100% (1)

- Inve, T and Portfolio Management Assin 1Документ11 страницInve, T and Portfolio Management Assin 1Filmona YonasОценок пока нет

- FM ExamДокумент13 страницFM Examtigist abebeОценок пока нет

- Business Finance Project - DebenturesДокумент16 страницBusiness Finance Project - DebenturesMuhammad TalhaОценок пока нет

- What Is An IndentureДокумент6 страницWhat Is An IndenturecruellaОценок пока нет

- Bond MarketsДокумент8 страницBond MarketsZaira Mae DungcaОценок пока нет

- Capital Structure DefinitionДокумент15 страницCapital Structure DefinitionVan MateoОценок пока нет

- Types of DebenturesДокумент3 страницыTypes of DebenturesMadhumitaSinghОценок пока нет

- Deb An TuresДокумент10 страницDeb An TuresWeОценок пока нет

- Chapter Three: Fixed Income Securities: BondДокумент11 страницChapter Three: Fixed Income Securities: BondGemechisОценок пока нет

- Debt Obligation: Refinancing May Refer To The Replacement of An ExistingДокумент8 страницDebt Obligation: Refinancing May Refer To The Replacement of An ExistingMani MaranОценок пока нет

- Chapter 5 Non-Current Liabilities-Kieso IfrsДокумент67 страницChapter 5 Non-Current Liabilities-Kieso IfrsAklil TeganewОценок пока нет

- Accounting 2Документ4 страницыAccounting 2DEVASHYA KHATIKОценок пока нет

- Arrangement of Funds LPSДокумент57 страницArrangement of Funds LPSRohan SinglaОценок пока нет

- First Slide:: Independent Agencies Such As Moody's, Fitch, and Standard & Poor's Evaluates BondsДокумент16 страницFirst Slide:: Independent Agencies Such As Moody's, Fitch, and Standard & Poor's Evaluates BondsMavis LunaОценок пока нет

- BBA2030493Документ14 страницBBA2030493Saad AhmedОценок пока нет

- Unit - II SECURITY INVESTMENTДокумент8 страницUnit - II SECURITY INVESTMENTnivantheking123Оценок пока нет

- The Constitutional Relationship Between Fundamental Rights and Directive PrinciplesДокумент10 страницThe Constitutional Relationship Between Fundamental Rights and Directive PrinciplesShreyaОценок пока нет

- 2021PGLAW14 - Penal Laws and Theorization of Deviant BehaviourДокумент4 страницы2021PGLAW14 - Penal Laws and Theorization of Deviant BehaviourShreyaОценок пока нет

- 2021PGLAW14 - Penal Laws and Theorization of Deviant BehaviourДокумент4 страницы2021PGLAW14 - Penal Laws and Theorization of Deviant BehaviourShreyaОценок пока нет

- 3 (B)Документ1 страница3 (B)ShreyaОценок пока нет

- 1648 - Media LawДокумент22 страницы1648 - Media LawShreya50% (2)

- 2021PGLAW14 - IA Test - AnswersДокумент5 страниц2021PGLAW14 - IA Test - AnswersShreyaОценок пока нет

- Rehabilitative Theory of Punishment and Its ShortcomingsДокумент4 страницыRehabilitative Theory of Punishment and Its ShortcomingsShreyaОценок пока нет

- Panchayats and Nyaya Panchayats: A Historical OverviewДокумент20 страницPanchayats and Nyaya Panchayats: A Historical OverviewShreya100% (2)

- Rehabilitative Theory of Punishment and Its ShortcomingsДокумент4 страницыRehabilitative Theory of Punishment and Its ShortcomingsShreyaОценок пока нет

- 2021PGLAW14 AnswersДокумент8 страниц2021PGLAW14 AnswersShreyaОценок пока нет

- 2021PGLAW14 AnswersДокумент8 страниц2021PGLAW14 AnswersShreyaОценок пока нет

- Weaknesses of International Law Exposed by Covid 19 PandemicДокумент1 страницаWeaknesses of International Law Exposed by Covid 19 PandemicVivek VaibhavОценок пока нет

- Project Report On Contract Depriving A Party of Interest: Ground For VoidДокумент12 страницProject Report On Contract Depriving A Party of Interest: Ground For VoidShreyaОценок пока нет

- JayeshAgrawal 1625 InvestigationIntoAffairsOfTheCompany 2020Документ17 страницJayeshAgrawal 1625 InvestigationIntoAffairsOfTheCompany 2020ShreyaОценок пока нет

- Cybersecurity: Issues and ChallengesДокумент3 страницыCybersecurity: Issues and ChallengesShreyaОценок пока нет

- P W ON: Roject ORKДокумент51 страницаP W ON: Roject ORKShreyaОценок пока нет

- CM L 15 110415 Sunil AbrahamДокумент5 страницCM L 15 110415 Sunil AbrahamShreyaОценок пока нет

- Jayesh PILДокумент21 страницаJayesh PILShreyaОценок пока нет

- Project Report On BANKING LAW A Case Study On Ifci Submitted To - Dr. AJAY KUMAR Submitted by - Swetank Sharma Roll No - 1179Документ18 страницProject Report On BANKING LAW A Case Study On Ifci Submitted To - Dr. AJAY KUMAR Submitted by - Swetank Sharma Roll No - 1179ShreyaОценок пока нет

- Managing Stress in CollegeДокумент33 страницыManaging Stress in Collegebhargavi mishraОценок пока нет

- Project Report On Drafting, Pleading and Conveyancing: Drafting of Sale DeedДокумент21 страницаProject Report On Drafting, Pleading and Conveyancing: Drafting of Sale DeedShreyaОценок пока нет

- Panchayats and Nyaya Panchayats: A Historical OverviewДокумент20 страницPanchayats and Nyaya Panchayats: A Historical OverviewShreya100% (2)

- Project Report On TAXATION LAW-II: Abatement of Duty On Damaged or Deteriorated GoodsДокумент15 страницProject Report On TAXATION LAW-II: Abatement of Duty On Damaged or Deteriorated GoodsShreya100% (1)

- Chanakya National Law University: A Project ofДокумент38 страницChanakya National Law University: A Project ofShreyaОценок пока нет

- Public Policy & Contracts: Recent TrendsДокумент2 страницыPublic Policy & Contracts: Recent TrendsShreyaОценок пока нет

- Dr.P.P.Rao Unit-I: Nature, Scope and Basis of Private International LawДокумент14 страницDr.P.P.Rao Unit-I: Nature, Scope and Basis of Private International LawShreyaОценок пока нет

- Insurance Project Inzmamul Haque 933Документ22 страницыInsurance Project Inzmamul Haque 933ShreyaОценок пока нет

- Assignment Solutions GUIDE (2019-2020)Документ9 страницAssignment Solutions GUIDE (2019-2020)ShreyaОценок пока нет

- Managing Stress in CollegeДокумент33 страницыManaging Stress in Collegebhargavi mishraОценок пока нет

- Format - Suit For Dissolution of PartnershipДокумент5 страницFormat - Suit For Dissolution of PartnershipShreya67% (6)

- Exercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Документ3 страницыExercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Sylvia GynОценок пока нет

- BonusLetter 3Документ1 страницаBonusLetter 3ckpfx6qsggОценок пока нет

- Financial Mathematics Exercises Actuarial Studies UNSWДокумент115 страницFinancial Mathematics Exercises Actuarial Studies UNSWgy5115123Оценок пока нет

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент12 страницStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceamool rokadeОценок пока нет

- UntitledДокумент71 страницаUntitledIsaque Dietrich GarciaОценок пока нет

- Monetary PolicyДокумент31 страницаMonetary PolicyInderpreet KaurОценок пока нет

- Hilton Black Stone CaseДокумент13 страницHilton Black Stone CaseAman Baweja100% (1)

- Joy 1Документ27 страницJoy 1rp63337651Оценок пока нет

- These Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyДокумент2 страницыThese Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyTech Dealer50% (2)

- Sample Bank Customer Satisfaction QuestionnaireДокумент13 страницSample Bank Customer Satisfaction QuestionnaireUjjal Banerjee100% (4)

- Report Format - FFMДокумент6 страницReport Format - FFMMuhammad MansoorОценок пока нет

- Export Import Process DocumentationДокумент13 страницExport Import Process Documentationgarganurag12Оценок пока нет

- How To File Bir Form 1700 Using EbirformsДокумент7 страницHow To File Bir Form 1700 Using EbirformsMECHILLE PAY VILLAREALОценок пока нет

- Impact of Working Capital on Bank ProfitabilityДокумент9 страницImpact of Working Capital on Bank ProfitabilitySocialist GopalОценок пока нет

- Apr FinalДокумент48 страницApr FinalVivek PatilОценок пока нет

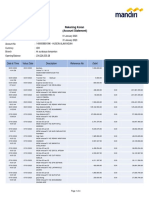

- Rek Koran Mandiri PT HAI Jan-April 2023Документ14 страницRek Koran Mandiri PT HAI Jan-April 2023wahyu suhartonoОценок пока нет

- Astronaut AstroДокумент2 страницыAstronaut AstroSugar SugarОценок пока нет

- Uv2499 PDF EngДокумент3 страницыUv2499 PDF Engharisankar suresh100% (1)

- Service Marketing Mix or 7p'sДокумент5 страницService Marketing Mix or 7p'srasel_ustcОценок пока нет

- Quick Bill Summary: Manage Your Account & View Your Usage Details Account Number Date DueДокумент4 страницыQuick Bill Summary: Manage Your Account & View Your Usage Details Account Number Date Duekristen kindleОценок пока нет

- 1601 EqДокумент2 страницы1601 EqJam DiolazoОценок пока нет

- Whitepaper DragonДокумент26 страницWhitepaper DragonSanjayThakkar100% (1)

- Power To Make Rules For Controlling Stock ExchangeДокумент3 страницыPower To Make Rules For Controlling Stock ExchangeSambit Kumar PaniОценок пока нет

- Housing Finance in AfricaДокумент12 страницHousing Finance in AfricaOluwole DaramolaОценок пока нет

- Bank service charge noticeДокумент3 страницыBank service charge noticeDr GoherОценок пока нет

- Understanding Balance SheetsДокумент40 страницUnderstanding Balance SheetsHimanshu KashyapОценок пока нет

- Farm Financial Statements GuideДокумент8 страницFarm Financial Statements GuideGENER DE GUZMANОценок пока нет

- General Quarter 2 - Week 1: ZZZZZZДокумент14 страницGeneral Quarter 2 - Week 1: ZZZZZZJakim Lopez0% (1)

- My BillДокумент2 страницыMy BillMohammad AtifОценок пока нет

- Working Capital Management AssignmentДокумент10 страницWorking Capital Management AssignmentRitesh Singh RathoreОценок пока нет