Вам также может понравиться

- Exp Realty Agent Attraction BookДокумент23 страницыExp Realty Agent Attraction BookErik Gerace100% (1)

- Fabm2 Q1Документ149 страницFabm2 Q1Gladys Angela Valdemoro50% (4)

- Test Bank Microeconomics-1st-Edition-Acemoglu Chapter 1Документ28 страницTest Bank Microeconomics-1st-Edition-Acemoglu Chapter 1Jai Ma Ri100% (2)

- Cindy Lota - Activity No. 4 - SFP Antonio TradingДокумент5 страницCindy Lota - Activity No. 4 - SFP Antonio TradingCindy Lota100% (2)

- Fundamentals of Accountancy, Business, and Management 2: ExpectationДокумент131 страницаFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Senior High School S.Y. 2019-2020Документ4 страницыSenior High School S.Y. 2019-2020Cy Dollete-Suarez100% (1)

- Answer Key For QuizzesДокумент2 страницыAnswer Key For QuizzesAlta SophiaОценок пока нет

- Corporate Governance in Ford Motor CompanyДокумент14 страницCorporate Governance in Ford Motor CompanyLarisa Samciuc100% (3)

- Worksheet SampleДокумент6 страницWorksheet SampleLycksele Rodulfa86% (7)

- Chapter 3statement of Changes in EquityДокумент14 страницChapter 3statement of Changes in EquityKyla DizonОценок пока нет

- ROCO - SCI Unit TestДокумент9 страницROCO - SCI Unit TestRaymond Roco100% (1)

- Fabm-2 2Документ33 страницыFabm-2 2KIRSTEN HENRYK CHINGОценок пока нет

- Name: - Date: - Grade Level & SectionДокумент11 страницName: - Date: - Grade Level & SectionCynthia Santos100% (1)

- Statement of Financial PositionДокумент10 страницStatement of Financial Positionmark jim toreroОценок пока нет

- Sdo Batangas: Department of EducationДокумент15 страницSdo Batangas: Department of EducationPrincess GabaynoОценок пока нет

- Module 6 - Fabm2-MergedДокумент37 страницModule 6 - Fabm2-MergedJaazaniah S. PavilionОценок пока нет

- Dunong Consultancy Services Income Statement For The Month of July 2020Документ4 страницыDunong Consultancy Services Income Statement For The Month of July 2020Denise MoralesОценок пока нет

- Lesson 2 - The Statement of Comprehensive Income - ActivityДокумент3 страницыLesson 2 - The Statement of Comprehensive Income - ActivityEmeldinand Padilla Motas0% (2)

- FAR Chapter4 FinalДокумент43 страницыFAR Chapter4 FinalPATRICIA COLINAОценок пока нет

- Abm Act 3 FinalДокумент6 страницAbm Act 3 FinalJasper Briones IIОценок пока нет

- Activity 4.1 JKL Company Horizontal AnalysisДокумент4 страницыActivity 4.1 JKL Company Horizontal AnalysisChancellor RimuruОценок пока нет

- Change in Equity SCEДокумент3 страницыChange in Equity SCEAizia Sarceda Guzman100% (2)

- Business MathДокумент2 страницыBusiness MathMarcОценок пока нет

- Customer Relationship Report Demo RevisedДокумент16 страницCustomer Relationship Report Demo RevisedLaila Mae PiloneoОценок пока нет

- Production BudgetДокумент11 страницProduction BudgetSamson, Ma. Louise Ren A.Оценок пока нет

- Accounting 2 Week 1 4 LPДокумент33 страницыAccounting 2 Week 1 4 LPMewifell100% (1)

- Intervention in Fabm 1: PHP 35,000 PHP 15,000 PHP 107,000 PHP 70,000 PHP 120,000 22Документ12 страницIntervention in Fabm 1: PHP 35,000 PHP 15,000 PHP 107,000 PHP 70,000 PHP 120,000 22sarah macatangayОценок пока нет

- Report in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationДокумент14 страницReport in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationKOUJI N. MARQUEZОценок пока нет

- Obien, Francine Denise Eleanor G. Abm 12 Y1-7Документ2 страницыObien, Francine Denise Eleanor G. Abm 12 Y1-7Emar Kim0% (1)

- SCI WeiLong TradingДокумент4 страницыSCI WeiLong TradingJoyce CalmaОценок пока нет

- Identify Which of The Following Transactions FallДокумент1 страницаIdentify Which of The Following Transactions FallAdoree Ramos75% (4)

- Completing The Acctg CycleДокумент14 страницCompleting The Acctg CycleHearty Hitutua100% (1)

- Lesson 1 Abm 2Документ35 страницLesson 1 Abm 2Albert Gaddiel CobicoОценок пока нет

- ACCTG 1 Week 2-3 - Accounting in BusinessДокумент13 страницACCTG 1 Week 2-3 - Accounting in BusinessReygie FabrigaОценок пока нет

- Statement of Changes in EquityДокумент2 страницыStatement of Changes in EquityNicole Allyson AguantaОценок пока нет

- Opportunities Atractiveness MatrixДокумент9 страницOpportunities Atractiveness MatrixEliОценок пока нет

- CHAPTER 2 Horizontal-AnalysisДокумент1 страницаCHAPTER 2 Horizontal-AnalysisAiron Bendaña0% (1)

- FABM2 Week5Документ14 страницFABM2 Week5Hazel TolentinoОценок пока нет

- Fabm2 Q1mod1 Statement of Financial Position Denver Aliwana Bgo v1Документ28 страницFabm2 Q1mod1 Statement of Financial Position Denver Aliwana Bgo v1Pedana RañolaОценок пока нет

- Assignment1 M1 Transaction AnalysisДокумент2 страницыAssignment1 M1 Transaction AnalysisAngel DIMACULANGANОценок пока нет

- General Journal: Date Account Titles and Explanation Ref Debit CreditДокумент17 страницGeneral Journal: Date Account Titles and Explanation Ref Debit CreditPrecious NosaОценок пока нет

- Seatwork 5: Application A. Owner's EquityДокумент7 страницSeatwork 5: Application A. Owner's EquityAngela GarciaОценок пока нет

- Abm 2 Topic 1: Statement of Comprehensive Income Learning ObjectivesДокумент8 страницAbm 2 Topic 1: Statement of Comprehensive Income Learning ObjectivesJUDITH PIANOОценок пока нет

- Dellosa Cleaners Adjusting Entry For The Year Ended September 30, 2022. Accounts Debit CreditДокумент6 страницDellosa Cleaners Adjusting Entry For The Year Ended September 30, 2022. Accounts Debit CreditJaira AsuncionОценок пока нет

- Problem #3 SciДокумент2 страницыProblem #3 SciJhazz Kyll100% (1)

- FABM 2 - Lesson1 5Документ78 страницFABM 2 - Lesson1 5Sis HopОценок пока нет

- Crash Landing On You Company Financial StatementsДокумент6 страницCrash Landing On You Company Financial StatementsEmar KimОценок пока нет

- CHAPTER 2 Vertical-AnalysisДокумент1 страницаCHAPTER 2 Vertical-AnalysisAiron BendañaОценок пока нет

- Exercise 9Документ4 страницыExercise 9Norhanifa CosignОценок пока нет

- Adjsuting Journal EntriesДокумент2 страницыAdjsuting Journal EntriesRey Luna100% (1)

- Fundamentals of Accounting, Business and Management 2: Quarter 1-Module 1: Statement of Financial Position (SFP)Документ20 страницFundamentals of Accounting, Business and Management 2: Quarter 1-Module 1: Statement of Financial Position (SFP)Arvin Salazar Llaneta100% (1)

- Effcets of Choosing AbmДокумент25 страницEffcets of Choosing AbmJanesa MaxcenОценок пока нет

- Balance Sheet Only-Agatha TradingДокумент1 страницаBalance Sheet Only-Agatha TradingJasmine Acta0% (1)

- Hourly Employee Earnings Rate M T W TH F Reg. OT GrossДокумент6 страницHourly Employee Earnings Rate M T W TH F Reg. OT GrossAislin Joy SabusapОценок пока нет

- 2nd QTR SLM FundamentalsABM1 CompleteДокумент129 страниц2nd QTR SLM FundamentalsABM1 CompleteJulia Sophia Mendoza100% (2)

- Activity:: I. Define The Following TermsДокумент3 страницыActivity:: I. Define The Following TermsAnonymousОценок пока нет

- Change in Equity SCEДокумент3 страницыChange in Equity SCEAizia Sarceda GuzmanОценок пока нет

- Group 6Документ6 страницGroup 6Love KarenОценок пока нет

- FABM2 Full ModuleДокумент201 страницаFABM2 Full ModuleSumma Comms Laude100% (3)

- Name: - Section: - Schedule: - Class Number: - DateДокумент8 страницName: - Section: - Schedule: - Class Number: - DateBridgette Hanna MortellОценок пока нет

- MATH 11 FABM Quarter 1Документ46 страницMATH 11 FABM Quarter 1cjОценок пока нет

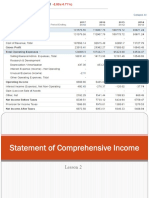

- Lesson 2 Statement of Comprehensive IncomeДокумент23 страницыLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Financial Accounting and Reporting: Exercise 1Документ6 страницFinancial Accounting and Reporting: Exercise 1Lenneth MonesОценок пока нет

- Statement of Comprehensive IncomeДокумент28 страницStatement of Comprehensive IncomePrincess GuimbalОценок пока нет

- UST Golden Notes in Obligations and ContДокумент56 страницUST Golden Notes in Obligations and ContYannaОценок пока нет

- Theory Financial Accounting Valix 2018 Revised EditionДокумент465 страницTheory Financial Accounting Valix 2018 Revised EditionYannaОценок пока нет

- Km. 30 Aguinaldo Highway, City of Dasmariñas, CaviteДокумент1 страницаKm. 30 Aguinaldo Highway, City of Dasmariñas, CaviteYannaОценок пока нет

- John Proust (1799)Документ7 страницJohn Proust (1799)YannaОценок пока нет

- Qualitative Research in Computer Science Education PDFДокумент6 страницQualitative Research in Computer Science Education PDFYannaОценок пока нет

- John Proust (1799)Документ7 страницJohn Proust (1799)YannaОценок пока нет

- SurveyДокумент2 страницыSurveyYannaОценок пока нет

- Discounts, Markup and MarkdownДокумент3 страницыDiscounts, Markup and MarkdownYannaОценок пока нет

- Final Module g11 1Документ18 страницFinal Module g11 1YannaОценок пока нет

- AbcdefgДокумент4 страницыAbcdefgYannaОценок пока нет

- Sequin July 2018 Case Study AInformationДокумент42 страницыSequin July 2018 Case Study AInformationMuhd FaridОценок пока нет

- Scope of Work For Corporate & Tax ConsultantДокумент10 страницScope of Work For Corporate & Tax ConsultantStartup CAОценок пока нет

- Cma (Usa) (Certified Management Accounting) Part 1: External Financial Reporting Analysis CHP 1: Financial StatementsДокумент3 страницыCma (Usa) (Certified Management Accounting) Part 1: External Financial Reporting Analysis CHP 1: Financial StatementsAakash SonarОценок пока нет

- 4 - Home Loan TerminolgyДокумент210 страниц4 - Home Loan Terminolgypurit83Оценок пока нет

- Financial Statement AnalysisДокумент40 страницFinancial Statement AnalysisYucel BozbasОценок пока нет

- 27 Jul 2018 Tenders Bids of Pakistan by Maven PKДокумент162 страницы27 Jul 2018 Tenders Bids of Pakistan by Maven PKMaven PKОценок пока нет

- Payslip - 2020 11 26Документ1 страницаPayslip - 2020 11 26itkrishna1988Оценок пока нет

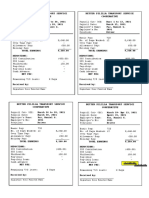

- Better Pililla Transport Service Cooperative Better Pililla Transport Service CooperativeДокумент1 страницаBetter Pililla Transport Service Cooperative Better Pililla Transport Service CooperativeHellen DeaОценок пока нет

- HP - Argus PDFДокумент5 страницHP - Argus PDFJeff SturgeonОценок пока нет

- TEMPLATE Financial Projections WorkbookДокумент22 страницыTEMPLATE Financial Projections WorkbookFrancois ChampenoisОценок пока нет

- FA Foundations Module 2Документ66 страницFA Foundations Module 2Irfan AhmedОценок пока нет

- Q - Shut Down ReplacementДокумент1 страницаQ - Shut Down ReplacementIrahq Yarte TorrejosОценок пока нет

- Soal Latihan 2Документ4 страницыSoal Latihan 2Fradila Ayu NabilaОценок пока нет

- Valeant Presentation PershingДокумент47 страницValeant Presentation PershingNick SposaОценок пока нет

- Date Account Title Debit Credit: Cost Method Equity MethodДокумент4 страницыDate Account Title Debit Credit: Cost Method Equity MethodFriska AvriliaОценок пока нет

- Revised DASAP Application For MicrograntДокумент4 страницыRevised DASAP Application For Micrograntabrshseven8Оценок пока нет

- Cash Flow Statement 2016-2020Документ8 страницCash Flow Statement 2016-2020yip manОценок пока нет

- Analysis of The Factors Affecting Devident PolicyДокумент12 страницAnalysis of The Factors Affecting Devident PolicyJung AuLiaОценок пока нет

- Corporate CitizenshipДокумент4 страницыCorporate CitizenshipAngelica MarinОценок пока нет

- ACCT1002 Assignment 3B 2nd S 2021-2022Документ16 страницACCT1002 Assignment 3B 2nd S 2021-2022Zenika PetersОценок пока нет

- Tax Law CasesДокумент10 страницTax Law CasespriyaОценок пока нет

- Trusts: Reading: Australian Master Tax Guide 59 Edition Chapter 6Документ62 страницыTrusts: Reading: Australian Master Tax Guide 59 Edition Chapter 6Robin LiuОценок пока нет

- The Analysis of The Impact of Accounting Records Keeping On The Performance of The Small Scale EnterprisesДокумент17 страницThe Analysis of The Impact of Accounting Records Keeping On The Performance of The Small Scale EnterprisesBaziyaka VincianneОценок пока нет

- BAC 2684 - Group Assignment & Guidelines - 2022Документ10 страницBAC 2684 - Group Assignment & Guidelines - 2022premsuwaatiiОценок пока нет

- (8b) Analysis of Leverages (Cir. 9.3.2017)Документ44 страницы(8b) Analysis of Leverages (Cir. 9.3.2017)Sarvar PathanОценок пока нет