Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- A Case Study Report On Plastic Industries Inc. 1Документ20 страницA Case Study Report On Plastic Industries Inc. 1danielaltah67% (6)

- Resident To Nro Conversion FormДокумент3 страницыResident To Nro Conversion FormAbhiruchiОценок пока нет

- Nri Investors - DeclarationДокумент1 страницаNri Investors - DeclarationAbhiruchiОценок пока нет

- Parkwheels PDFДокумент14 страницParkwheels PDFAbhiruchiОценок пока нет

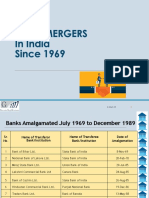

- Merger of Commercial Banks Since 1969Документ9 страницMerger of Commercial Banks Since 1969AbhiruchiОценок пока нет

- Ch4-Change CommunicationsДокумент18 страницCh4-Change CommunicationsMohammed NafeaОценок пока нет

- ASUG84069 - The Fashion Solution Portfolio From SAP and What You Need To KnowДокумент82 страницыASUG84069 - The Fashion Solution Portfolio From SAP and What You Need To KnowCharith WeerasekaraОценок пока нет

- Abdul Awet CV-1Документ5 страницAbdul Awet CV-1Johnson GirsangОценок пока нет

- The Impact of Employee Engagement On Job Satisfaction - An Emerging Trend PDFДокумент11 страницThe Impact of Employee Engagement On Job Satisfaction - An Emerging Trend PDFNitin SharmaОценок пока нет

- Alcoa PDFДокумент184 страницыAlcoa PDFNADIA SABINA SUASTI GUDIÑOОценок пока нет

- Analysing The Internal Environment of The FirmДокумент13 страницAnalysing The Internal Environment of The Firmfadillah manuhutuОценок пока нет

- Lean Manufacturing BasicsДокумент29 страницLean Manufacturing Basicssunilkhairnar38Оценок пока нет

- Reviewer RESA LAWДокумент34 страницыReviewer RESA LAWMadonna P. EsperaОценок пока нет

- Job Opportunities in The Film IndustryДокумент7 страницJob Opportunities in The Film Industryapi-496240163Оценок пока нет

- REDBULL Final For Print GauravДокумент46 страницREDBULL Final For Print Gauravanju manolaОценок пока нет

- Group Case AnalysisДокумент5 страницGroup Case AnalysisMislav Matijević100% (1)

- EMPEA CaseStudy OlamДокумент2 страницыEMPEA CaseStudy Olamcatiblacki420Оценок пока нет

- Strategic Analysis of Bisleri: Project Report ONДокумент26 страницStrategic Analysis of Bisleri: Project Report ONSamar Asil0% (1)

- Diploma in International Financial Reporting (Dipifr) : Syllabus and Study GuideДокумент14 страницDiploma in International Financial Reporting (Dipifr) : Syllabus and Study GuideAnil Kumar AkОценок пока нет

- BIMДокумент9 страницBIMNaseem KhanОценок пока нет

- Week 1 AssignmentДокумент2 страницыWeek 1 AssignmentSHERMIN AKTHER RUMAОценок пока нет

- Tds TcsДокумент20 страницTds TcsnaysarОценок пока нет

- Think Outside The Boss Pop Ed SlidesДокумент31 страницаThink Outside The Boss Pop Ed SlidesmerrickОценок пока нет

- Inspection and TestingДокумент5 страницInspection and TestingAhmed Elhaj100% (1)

- May - August 2020 Exam Timetable FinalДокумент24 страницыMay - August 2020 Exam Timetable FinalMARSHAОценок пока нет

- R.K.Enterprises: Particulars Credit DebitДокумент3 страницыR.K.Enterprises: Particulars Credit DebitRakesh Kumar bairwaОценок пока нет

- Week 2 Lecture SlidesДокумент32 страницыWeek 2 Lecture SlidesMike AmukhumbaОценок пока нет

- Sample Paper 4Документ6 страницSample Paper 4Ashish BatraОценок пока нет

- Merger and ConsolidationДокумент40 страницMerger and ConsolidationalbycadavisОценок пока нет

- Co-Operative Movements in NepalДокумент18 страницCo-Operative Movements in NepalSunil Kumar MahatoОценок пока нет

- Registration Form - Thailand 2010 July - SeptДокумент1 страницаRegistration Form - Thailand 2010 July - SeptniaseanОценок пока нет

- Energy Derivatives: Sonal GuptaДокумент48 страницEnergy Derivatives: Sonal GuptaVindyanchal Kumar100% (1)

- Cost Estimating: Microsoft ProjectДокумент3 страницыCost Estimating: Microsoft Projectain_ykbОценок пока нет

- Sarah Chey's ResumeДокумент1 страницаSarah Chey's Resumeca8sarah15Оценок пока нет