Вам также может понравиться

- Consolidated Profit and Loss Account For The Year Ended December 31, 2008Документ16 страницConsolidated Profit and Loss Account For The Year Ended December 31, 2008madihaijazОценок пока нет

- Financial Statement Analysis: Business Strategy & Competitive AdvantageОт EverandFinancial Statement Analysis: Business Strategy & Competitive AdvantageРейтинг: 5 из 5 звезд5/5 (1)

- Term Paper of Reliance Weaving LTDДокумент12 страницTerm Paper of Reliance Weaving LTDadeelasghar091Оценок пока нет

- Ratio Analysis of TATA MotorsДокумент7 страницRatio Analysis of TATA MotorsyashlathaОценок пока нет

- Toyota Common Size Balance Sheet For The Years 2005 & 2006 (Rs. in Crores)Документ25 страницToyota Common Size Balance Sheet For The Years 2005 & 2006 (Rs. in Crores)balki123Оценок пока нет

- Financial Analysis of Dabur Industries PVTДокумент20 страницFinancial Analysis of Dabur Industries PVTRahul BattooОценок пока нет

- ICI Pakistan AnalysisДокумент19 страницICI Pakistan AnalysisAffan AnwarОценок пока нет

- RatiosДокумент12 страницRatiosstuck00123Оценок пока нет

- Income Statement OldДокумент9 страницIncome Statement OldjhanzabОценок пока нет

- Ratio Analysis: Presented By: Ajay BankaДокумент16 страницRatio Analysis: Presented By: Ajay Bankaajay070188Оценок пока нет

- Ratio Analysis of Hero Honda 2007-2008: Prepared byДокумент25 страницRatio Analysis of Hero Honda 2007-2008: Prepared byAkanksha RajanОценок пока нет

- Return On Assets (ROA) : ROA Is An Indicator of How Profitable A Company Is Relative To ItsДокумент4 страницыReturn On Assets (ROA) : ROA Is An Indicator of How Profitable A Company Is Relative To ItsTanya RahmanОценок пока нет

- Singer BangladeshДокумент16 страницSinger BangladeshMahbubur RahmanОценок пока нет

- 9 Income STMTДокумент20 страниц9 Income STMTPragya JainОценок пока нет

- 9 Income STMTДокумент20 страниц9 Income STMTSapna BansalОценок пока нет

- 9 Income STMTДокумент20 страниц9 Income STMTNishant_Gupta_8770Оценок пока нет

- Chapter 6 Valuating StocksДокумент46 страницChapter 6 Valuating StocksCezarene FernandoОценок пока нет

- Ratio AnalysisДокумент17 страницRatio AnalysisXain SyedОценок пока нет

- FMДокумент233 страницыFMparika khannaОценок пока нет

- Econ 3073 Assignment - 1 and 2 CompleteДокумент12 страницEcon 3073 Assignment - 1 and 2 CompleteMudassar Gul Bin AshrafОценок пока нет

- Trend Analysis of ACI Ltd. & Renata Ltd.Документ22 страницыTrend Analysis of ACI Ltd. & Renata Ltd.sabbir_amОценок пока нет

- Ratio Analysis of Singer Bangladesh LTDДокумент22 страницыRatio Analysis of Singer Bangladesh LTDSandip Kar100% (1)

- Muhammad Usman JamilДокумент15 страницMuhammad Usman JamilMuhammad UmarОценок пока нет

- Anamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaДокумент24 страницыAnamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaAnamika ChakrabartyОценок пока нет

- Financial Statement Analysis of Lucky CementДокумент27 страницFinancial Statement Analysis of Lucky CementRaja UmairОценок пока нет

- Ratio Analysis .. Horizontal and Vertical AnalysisДокумент21 страницаRatio Analysis .. Horizontal and Vertical AnalysisBabar Ali100% (1)

- Bajaj TilesДокумент27 страницBajaj TilesAkash GuptaОценок пока нет

- Profitability Ratios: Profit MarginДокумент6 страницProfitability Ratios: Profit Marginimdad1986Оценок пока нет

- Acma Final ReportДокумент11 страницAcma Final ReportparidhiОценок пока нет

- Financial Analysis of Ashok Leyland LimitedДокумент15 страницFinancial Analysis of Ashok Leyland LimitedYamini NegiОценок пока нет

- Amul PresentationДокумент21 страницаAmul PresentationpkdobariyaОценок пока нет

- Ratio Analysis of BMWДокумент16 страницRatio Analysis of BMWRashidsarwar01Оценок пока нет

- Analysis of Financial StatementsДокумент36 страницAnalysis of Financial StatementsHery PrambudiОценок пока нет

- 9 Income STMTДокумент20 страниц9 Income STMTKamal Kannan GОценок пока нет

- Advance Analysis of Financial Statement AssignmentДокумент17 страницAdvance Analysis of Financial Statement AssignmentWaqas Ur RehmanОценок пока нет

- Objective of Ratio AnalysisДокумент5 страницObjective of Ratio AnalysisAvinash SinhaОценок пока нет

- Afs Assignment Profitability RatiosДокумент9 страницAfs Assignment Profitability RatiosMohsin AzizОценок пока нет

- NestleДокумент25 страницNestleShafali PrabhakarОценок пока нет

- Current Ratio: Nestle Pakistan LimitedДокумент12 страницCurrent Ratio: Nestle Pakistan Limitedadilshaukat24Оценок пока нет

- Accounts Project NestleДокумент23 страницыAccounts Project NestleDhanshree KhupkarОценок пока нет

- Accounting Question 2Документ8 страницAccounting Question 2Moustafa Almoataz100% (1)

- Bajaj Auto LTD: Presented By: Hitesh RameshДокумент15 страницBajaj Auto LTD: Presented By: Hitesh RameshnancyagarwalОценок пока нет

- CF AssignmentДокумент9 страницCF Assignmentsadhana tiwariОценок пока нет

- Aetna Financial AnalysisДокумент11 страницAetna Financial AnalysisKimberlyHerringОценок пока нет

- Ratio Analysis:: Types of RatiosДокумент17 страницRatio Analysis:: Types of RatiossagarОценок пока нет

- JyotiNishad CeresДокумент7 страницJyotiNishad CeresDancing DopeОценок пока нет

- 1.1 General BackgroungДокумент20 страниц1.1 General BackgroungPradeep GhimireОценок пока нет

- Financial Statements Ratio Analysis of InfosysДокумент15 страницFinancial Statements Ratio Analysis of InfosysVishal KushwahaОценок пока нет

- Bluestar Limited: Annual Report AnalysisДокумент16 страницBluestar Limited: Annual Report AnalysisKunal NegiОценок пока нет

- A Report On Financial Analysis of Next PLC 3Документ11 страницA Report On Financial Analysis of Next PLC 3Hamza AminОценок пока нет

- Atlas Honda Limited PresentationДокумент14 страницAtlas Honda Limited PresentationusmanjuttОценок пока нет

- Case: Big Boy: Levarage Various Ratios and TheirДокумент24 страницыCase: Big Boy: Levarage Various Ratios and TheirShagun SetiaОценок пока нет

- Accounting and Finance For Managers: Profitability Analysis RatiosДокумент20 страницAccounting and Finance For Managers: Profitability Analysis RatiosRiz KhanОценок пока нет

- Dupont Analysis For 3 Automobile CompaniesДокумент6 страницDupont Analysis For 3 Automobile Companiesradhika chaudharyОценок пока нет

- Name: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceДокумент46 страницName: Bilal Ahmed ID: Mc090200863 Degree: MBA Specialization: FinanceEngr MahaОценок пока нет

- RATIOS AnalysisДокумент61 страницаRATIOS AnalysisSamuel Dwumfour100% (1)

- Ratio Analysis - Montex PensДокумент28 страницRatio Analysis - Montex Penss_sannit2k9Оценок пока нет

- Case Study On AutomobileДокумент8 страницCase Study On AutomobileDipock MondalОценок пока нет

- FFC vs. EngroДокумент36 страницFFC vs. EngroAnsaria100% (1)

- Debit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Документ6 страницDebit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Riza Mae AlceОценок пока нет

- Tugas Inggris Chapter 2Документ5 страницTugas Inggris Chapter 2Alam MahardikaОценок пока нет

- Auditing Problems EmpleoДокумент19 страницAuditing Problems EmpleoGloria Bernal BonifacioОценок пока нет

- اسئلة اقتصادية باللغة الانجليزيةДокумент5 страницاسئلة اقتصادية باللغة الانجليزيةMoun DirОценок пока нет

- Financial Management - FSAДокумент6 страницFinancial Management - FSAAbby EsculturaОценок пока нет

- AFM Sample Model - 2 (Horizontal)Документ18 страницAFM Sample Model - 2 (Horizontal)munaftОценок пока нет

- Neraca Lajur P2 JayatamaДокумент3 страницыNeraca Lajur P2 JayatamaShula KinantiОценок пока нет

- Financial AspectДокумент16 страницFinancial AspectJezeree DichosoОценок пока нет

- P1-2B 6081901141Документ3 страницыP1-2B 6081901141Mentari Anggari67% (3)

- M3A Expanded Accounting EquationДокумент20 страницM3A Expanded Accounting EquationCharles Eli AlejandroОценок пока нет

- Accounting ReviewerДокумент21 страницаAccounting ReviewerAdriya Ley PangilinanОценок пока нет

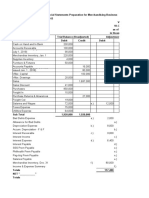

- DB6 - Worksheet & FS Prep For Merchandising BusinessДокумент4 страницыDB6 - Worksheet & FS Prep For Merchandising BusinessArrianeОценок пока нет

- Fundamentals of Accountancy, Business and Management 1 (FABM 1)Документ15 страницFundamentals of Accountancy, Business and Management 1 (FABM 1)cindy100% (4)

- Minority InterestДокумент28 страницMinority InterestKevin Leonel ManurungОценок пока нет

- Cup - Basic ParcorДокумент8 страницCup - Basic ParcorJerauld BucolОценок пока нет

- 1Документ48 страниц1Hamza Ali100% (2)

- InventoryДокумент93 страницыInventoryCarmelo John DelacruzОценок пока нет

- 09-DepEd2018 Part2-Observations and RecommДокумент279 страниц09-DepEd2018 Part2-Observations and RecommEmosОценок пока нет

- Audit of Intangible AssetsДокумент8 страницAudit of Intangible AssetsHira IdaceiОценок пока нет

- CH05Документ47 страницCH05carlosortizfelixОценок пока нет

- Assets Liabilities and Owner's Equity: Balance Sheet As On 1 January, 2019Документ5 страницAssets Liabilities and Owner's Equity: Balance Sheet As On 1 January, 2019KARUN RAJ K MBA IB 2018-20Оценок пока нет

- Problem 1 ReqДокумент5 страницProblem 1 ReqAgent348Оценок пока нет

- Accountancy-I SubjectiveДокумент2 страницыAccountancy-I SubjectiveAhmedОценок пока нет

- AP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYДокумент12 страницAP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYjasfОценок пока нет

- Question 1: Debit BalancesДокумент9 страницQuestion 1: Debit BalancesAsdfghjkl LkjhgfdsaОценок пока нет

- HOBA QuestionsДокумент7 страницHOBA QuestionsKristine CorporalОценок пока нет

- Castro Company ZABALLAДокумент11 страницCastro Company ZABALLAHelping Five (H5)Оценок пока нет

- SFM-Forecasting-Case-Study 1 - MicroDrive-QДокумент4 страницыSFM-Forecasting-Case-Study 1 - MicroDrive-QRehan KhanОценок пока нет

- Hari I - Comprehensive Financial Performance StrategyДокумент37 страницHari I - Comprehensive Financial Performance Strategydenta pradiptaОценок пока нет

- Madelyn Rialubin Travel Agency Adjusting Entries AdjustedДокумент5 страницMadelyn Rialubin Travel Agency Adjusting Entries AdjustedJustine Almodiel100% (1)