Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Sec. 24. Election of Directors or Trustees.Документ7 страницSec. 24. Election of Directors or Trustees.Lean Rain SandiОценок пока нет

- Noel Nettey ResumeДокумент6 страницNoel Nettey ResumeNoel NetteyОценок пока нет

- Blue Danube Si Green HydrobenДокумент11 страницBlue Danube Si Green HydrobenDiana AchimescuОценок пока нет

- Pricelist for Alpine Villas-Blanc units as of September 2017Документ1 страницаPricelist for Alpine Villas-Blanc units as of September 2017Snorri RaleОценок пока нет

- Paris Region Facts and Figures. 2020 EditionДокумент44 страницыParis Region Facts and Figures. 2020 EditionJerson ValenciaОценок пока нет

- A Study of Consumers Behaviour Related To KTMДокумент8 страницA Study of Consumers Behaviour Related To KTMDiganta DaimaryОценок пока нет

- Environmental Sustainability, Research, IOT, and Future DevelopmentДокумент4 страницыEnvironmental Sustainability, Research, IOT, and Future DevelopmentEditor IJTSRDОценок пока нет

- Natural Resources of BangladeshДокумент22 страницыNatural Resources of BangladeshDibakar Das0% (1)

- Ac 418 Group AssignmentДокумент6 страницAc 418 Group AssignmentJacob PossibilityОценок пока нет

- FB Marketing Tips For YouДокумент13 страницFB Marketing Tips For YouPamoris PamorisОценок пока нет

- Jaquard Fabrics FS 19-20Документ57 страницJaquard Fabrics FS 19-20Tarun KumarОценок пока нет

- History of Titan Watch IndustryДокумент46 страницHistory of Titan Watch IndustryWasim Khan25% (4)

- 7 Stages or Steps Involved in Marketing Research ProcessДокумент8 страниц7 Stages or Steps Involved in Marketing Research Processaltaf_catsОценок пока нет

- Architectural Record 2024-01Документ124 страницыArchitectural Record 2024-01ricardoОценок пока нет

- ProblemДокумент2 страницыProblemchandra K. SapkotaОценок пока нет

- Pega CSSAДокумент851 страницаPega CSSAkollarajasekharОценок пока нет

- PYC Navratri Festival 2023 - Introduction DeckДокумент36 страницPYC Navratri Festival 2023 - Introduction DeckNeel PanchalОценок пока нет

- Principles of AccountingДокумент70 страницPrinciples of AccountingCassandra UmaliОценок пока нет

- Valuation Report: Al Andalus Mall and Hotel, Jeddah, Kingdom of Saudi ArabiaДокумент96 страницValuation Report: Al Andalus Mall and Hotel, Jeddah, Kingdom of Saudi Arabiaalim shaikhОценок пока нет

- TAX Midterm ReviewerДокумент10 страницTAX Midterm ReviewerCookie MasterОценок пока нет

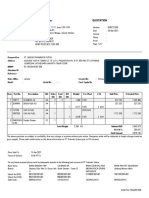

- PT Trakindo Utama Quotation for PT Basuki Rahmanta PutraДокумент2 страницыPT Trakindo Utama Quotation for PT Basuki Rahmanta PutraDeden PramikaОценок пока нет

- Estimation Engineer Role, Duties & Career GrowthДокумент19 страницEstimation Engineer Role, Duties & Career GrowthBehram Ciodia100% (1)

- Bidding DocumentsДокумент82 страницыBidding DocumentsPalwasha GulОценок пока нет

- System Features: 4.1 Query For A BookДокумент4 страницыSystem Features: 4.1 Query For A BookGowtham SaiОценок пока нет

- hyperMILL 2D 3DДокумент602 страницыhyperMILL 2D 3DX800XL100% (1)

- Web Development Using Wordpress - Unit-1Документ16 страницWeb Development Using Wordpress - Unit-1mekhushal07Оценок пока нет

- Wilson, Harry - Silverwork and JewelryДокумент542 страницыWilson, Harry - Silverwork and JewelryTecnologiaFAUDUNMdPОценок пока нет

- A Project Report On The Study of Consumer Satisfaction: Submitted ToДокумент35 страницA Project Report On The Study of Consumer Satisfaction: Submitted ToAshuОценок пока нет

- A Study On The Impact of Covid-19 On Digital MarketingДокумент66 страницA Study On The Impact of Covid-19 On Digital MarketingFitha FathimaОценок пока нет

- C. Castro Company-Cdc 2018Документ42 страницыC. Castro Company-Cdc 2018Gennelyn Lairise Rivera100% (1)