Вам также может понравиться

- Chapter 11Документ13 страницChapter 11jake doinog100% (6)

- PAS 8 Accounting Policies, Estimates and ErrorsДокумент10 страницPAS 8 Accounting Policies, Estimates and ErrorsAllaine Elfa100% (2)

- Chapter 14Документ31 страницаChapter 14MARY JUSTINE PAQUIBOT100% (1)

- Chapter 10 - Prior Period Errors: Problem 10-1 (IAA)Документ12 страницChapter 10 - Prior Period Errors: Problem 10-1 (IAA)Asi Cas JavОценок пока нет

- Operating Segment Revenue and Profit ReportingДокумент21 страницаOperating Segment Revenue and Profit ReportingLouise83% (6)

- Chapter 13: Operating Segment Segment Reporting - Core PrincipleДокумент10 страницChapter 13: Operating Segment Segment Reporting - Core PrinciplePaula BautistaОценок пока нет

- 10 PriorPeriodErrorsДокумент9 страниц10 PriorPeriodErrorsstudent100% (3)

- NCA Held For Sale Discontinued OperationsДокумент15 страницNCA Held For Sale Discontinued OperationsDog WatcherОценок пока нет

- Problems Discontinued, Acctg Changes, Interim, Opseg, Correction of ErrorДокумент21 страницаProblems Discontinued, Acctg Changes, Interim, Opseg, Correction of ErrorMmОценок пока нет

- Chapter 5 Events and Disclosures"The title "TITLEДокумент6 страницChapter 5 Events and Disclosures"The title "TITLEjake doinog75% (4)

- Noncurrent Asset Held For Sale: Problem 6-1 (IFRS)Документ10 страницNoncurrent Asset Held For Sale: Problem 6-1 (IFRS)Kimberly Claire Atienza71% (7)

- Chapter 12 Interim ReportingДокумент10 страницChapter 12 Interim ReportingRay SanzeninОценок пока нет

- INTERIM REPORTING With ANSWERSДокумент6 страницINTERIM REPORTING With ANSWERSRaven Sia100% (3)

- CHAPTER 11 - Operating SegmentsДокумент22 страницыCHAPTER 11 - Operating SegmentsStychri Alindayo83% (6)

- Cash Basis Accounting ProblemsДокумент12 страницCash Basis Accounting ProblemsMCDABC100% (9)

- INTERIM FINANCIAL REPORTINGДокумент64 страницыINTERIM FINANCIAL REPORTINGNiño Mendoza Mabato100% (2)

- Cash and Accrual BasisДокумент4 страницыCash and Accrual BasisBwwwiiiii100% (1)

- Operating Segment, Interim Reporting & Events After ReportingДокумент18 страницOperating Segment, Interim Reporting & Events After ReportingLyccaPascual50% (2)

- 162.005.exercises and AssignДокумент2 страницы162.005.exercises and AssignAngelli Lamique50% (2)

- Relax Company's current assets on Dec 31, 2019Документ4 страницыRelax Company's current assets on Dec 31, 2019Glen JavellanaОценок пока нет

- Chapter 7Документ11 страницChapter 7jake doinog86% (14)

- NONCURRENT ASSET HELD FOR SALE AND DISCONTINUED OPERATIONДокумент10 страницNONCURRENT ASSET HELD FOR SALE AND DISCONTINUED OPERATIONXОценок пока нет

- ACC 577 Quiz Week 3Документ12 страницACC 577 Quiz Week 3Mary100% (2)

- Correct! A Public Company Should Disclose Information About Profit or Loss andДокумент15 страницCorrect! A Public Company Should Disclose Information About Profit or Loss andJoana Trinidad100% (1)

- Interim Financial Reporting: Indoyon - JaniolaДокумент11 страницInterim Financial Reporting: Indoyon - JaniolaCaryl JANIOLAОценок пока нет

- Chapter 27 Derivatives ProblemsДокумент20 страницChapter 27 Derivatives ProblemsDaisy Ann Cariaga SaccuanОценок пока нет

- Prac 1 Cash Basis PDFДокумент12 страницPrac 1 Cash Basis PDFJay Lord FlorescaОценок пока нет

- Noncurrent Asset Held For Sale Problem 8-1Документ11 страницNoncurrent Asset Held For Sale Problem 8-1Clarisse Pelayo50% (2)

- Interim Financial Reporting PrinciplesДокумент17 страницInterim Financial Reporting PrinciplesAlexa LeeОценок пока нет

- Operating Segment: C. 71,000 AnswerДокумент152 страницыOperating Segment: C. 71,000 AnswerRuby Jane33% (3)

- Calculating Net Income Using Single Entry Accounting ProblemsДокумент14 страницCalculating Net Income Using Single Entry Accounting ProblemsHarvey Dienne Quiambao100% (6)

- Hard Company financial statement analysisДокумент4 страницыHard Company financial statement analysisMarriz Bustaliño Tan78% (9)

- Cash and Accrual Basis of Accounting, Single Entry and Error CorrectionДокумент11 страницCash and Accrual Basis of Accounting, Single Entry and Error CorrectionJoana Trinidad100% (3)

- Financial Accounting Vol.3 AДокумент10 страницFinancial Accounting Vol.3 ALovely Lorelie Del Mundo Planos29% (14)

- Single Entry, Cash and Accrual BasisДокумент36 страницSingle Entry, Cash and Accrual BasisAbby Navarro50% (2)

- Brines Christian Joseph C. Operating SegmentsДокумент58 страницBrines Christian Joseph C. Operating SegmentsAllana MierОценок пока нет

- Current Cost AccountingДокумент8 страницCurrent Cost AccountingHarvey Dienne Quiambao100% (2)

- CASH TO ACCRUAL SINGLE ENTRY With ANSWERSДокумент8 страницCASH TO ACCRUAL SINGLE ENTRY With ANSWERSRaven SiaОценок пока нет

- Operating Segment.Документ14 страницOperating Segment.Honey LimОценок пока нет

- Cfas Pfa 01Документ194 страницыCfas Pfa 01Kimberly Claire Atienza100% (1)

- ACCTGREV1 - 008 Operating Segments and Interim ReportingДокумент2 страницыACCTGREV1 - 008 Operating Segments and Interim ReportingNhaj100% (3)

- FAR2Документ27 страницFAR2Sheena CalderonОценок пока нет

- Notes To Financial Statement Problem 3-1: D. All of These Can Be Considered A Purpose of The NotesДокумент5 страницNotes To Financial Statement Problem 3-1: D. All of These Can Be Considered A Purpose of The Notesjake doinogОценок пока нет

- Cpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesДокумент15 страницCpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesSophia PerezОценок пока нет

- Intermediate Accounting 3 Quiz 1 Print ExamДокумент12 страницIntermediate Accounting 3 Quiz 1 Print ExamVerlyn ElfaОценок пока нет

- Financial Accounting Errors & CorrectionsДокумент5 страницFinancial Accounting Errors & CorrectionsHarvey Dienne QuiambaoОценок пока нет

- PAS34 Questio N& Answer!: Welcome To..Документ18 страницPAS34 Questio N& Answer!: Welcome To..Faker MejiaОценок пока нет

- Chapter 7Документ9 страницChapter 7Coursehero PremiumОценок пока нет

- Segment reporting and discontinued operationsДокумент12 страницSegment reporting and discontinued operationsAnalie Mendez100% (2)

- Accrual Accounting AdjustmentsДокумент1 страницаAccrual Accounting AdjustmentsJen DeloyОценок пока нет

- Related Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint VentureДокумент3 страницыRelated Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint Venturejake doinogОценок пока нет

- Segment ReportingДокумент2 страницыSegment ReportingNicole Chenper ChengОценок пока нет

- Operating Segments - Discussion ProblemsДокумент2 страницыOperating Segments - Discussion ProblemsHaidee Flavier SabidoОценок пока нет

- AdsadsdДокумент28 страницAdsadsdTong Wilson60% (5)

- ASSESSMENTSДокумент23 страницыASSESSMENTSJoana TrinidadОценок пока нет

- Events After The Reporting PeriodДокумент4 страницыEvents After The Reporting PeriodGlen JavellanaОценок пока нет

- PFA 1 Chapter 1 Current Assets SolutionsДокумент38 страницPFA 1 Chapter 1 Current Assets SolutionsAsi Cas Jav0% (1)

- 1T Siñel ACTIVITY7Документ10 страниц1T Siñel ACTIVITY7Von Jaurdan SinelОценок пока нет

- Assignment in Intermediateaccounting October 21Документ12 страницAssignment in Intermediateaccounting October 21Monica mangobaОценок пока нет

- Interim Reporting - Exercises and AnswersДокумент2 страницыInterim Reporting - Exercises and AnswersMARCUAP Flora Mel Joy H.Оценок пока нет

- 1.0 Law On Sales Nature and Form of The ContractДокумент116 страниц1.0 Law On Sales Nature and Form of The Contractjake doinogОценок пока нет

- Law On Agency PDFДокумент61 страницаLaw On Agency PDFjake doinogОценок пока нет

- Law of Agency Online VersionДокумент31 страницаLaw of Agency Online VersionDan Dan Dan DanОценок пока нет

- Masay Company's Statement of Comprehensive IncomeДокумент24 страницыMasay Company's Statement of Comprehensive Incomejake doinog88% (16)

- Partnership - Part 3: Case #1Документ15 страницPartnership - Part 3: Case #1jake doinogОценок пока нет

- Related Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint VentureДокумент3 страницыRelated Parties Problem 4-1: D. Two Ventures Simply Because They Share Joint Control Over Joint Venturejake doinogОценок пока нет

- Chapter 2Документ33 страницыChapter 2jake doinog93% (14)

- Sales Agency and Credit TransactionsДокумент144 страницыSales Agency and Credit TransactionsFrl Rizal100% (2)

- Chapter 7Документ11 страницChapter 7jake doinog86% (14)

- Chapter 9 Consignment SalesДокумент9 страницChapter 9 Consignment SalesAimee Diaz100% (3)

- Chapter 10 - Teacher's Manual - Afar Part 1Документ20 страницChapter 10 - Teacher's Manual - Afar Part 1Angelic67% (3)

- Chapter 5 Events and Disclosures"The title "TITLEДокумент6 страницChapter 5 Events and Disclosures"The title "TITLEjake doinog75% (4)

- 4Документ7 страниц4Venz LacreОценок пока нет

- Notes To Financial Statement Problem 3-1: D. All of These Can Be Considered A Purpose of The NotesДокумент5 страницNotes To Financial Statement Problem 3-1: D. All of These Can Be Considered A Purpose of The Notesjake doinogОценок пока нет

- What Is Production Planning?: Does That Seem Like A Pipe Dream?Документ6 страницWhat Is Production Planning?: Does That Seem Like A Pipe Dream?jake doinogОценок пока нет

- ContributionДокумент4 страницыContributionjake doinogОценок пока нет

- Chapter 6 Construction Contracts ProblemsДокумент25 страницChapter 6 Construction Contracts ProblemsjuennaguecoОценок пока нет

- Time Series Analysis: Meaning:A Time Series Consists of A Set of Observations Arranged in Chronological OrderДокумент11 страницTime Series Analysis: Meaning:A Time Series Consists of A Set of Observations Arranged in Chronological Orderjake doinogОценок пока нет

- Name of BusinessДокумент2 страницыName of Businessjake doinogОценок пока нет

- 1Документ3 страницы1jake doinogОценок пока нет

- Effects of social media, verbal abuse, and cleanliness on student performanceДокумент4 страницыEffects of social media, verbal abuse, and cleanliness on student performancejake doinogОценок пока нет

- SSCI PresentationДокумент3 страницыSSCI Presentationjake doinogОценок пока нет

- Business ProposalДокумент15 страницBusiness Proposaljake doinogОценок пока нет

- This Is My FieДокумент1 страницаThis Is My Fiejake doinogОценок пока нет

- This Is My FieДокумент1 страницаThis Is My Fiejake doinogОценок пока нет

- ThatДокумент1 страницаThatjake doinogОценок пока нет

- ThatДокумент1 страницаThatjake doinogОценок пока нет

- Text ScribdДокумент1 страницаText Scribdjake doinogОценок пока нет

- Management Accounting - IДокумент41 страницаManagement Accounting - Ivicky bindassОценок пока нет

- BASL Ratio Analysis Highlights Strong Financial PositionДокумент18 страницBASL Ratio Analysis Highlights Strong Financial PositionSreeram Anand IrugintiОценок пока нет

- Numeric Model MetricsДокумент5 страницNumeric Model MetricsAnkit NarulaОценок пока нет

- Break Even Chart-Meaning-Advantages and TypesДокумент12 страницBreak Even Chart-Meaning-Advantages and TypesrlwersalОценок пока нет

- Discontinued Operation IncomeДокумент15 страницDiscontinued Operation IncomeChristian GatchalianОценок пока нет

- Financial Ratio Analysis of Bajaj FinservДокумент43 страницыFinancial Ratio Analysis of Bajaj FinservAyaz Raza90% (10)

- SEE Diversey ProFormaДокумент34 страницыSEE Diversey ProFormaJose Luis Becerril BurgosОценок пока нет

- Financial Management Project Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 Management of Working CapitalДокумент5 страницFinancial Management Project Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 Management of Working CapitalDev ShahОценок пока нет

- Finance MC 1 2 3 4 17Документ28 страницFinance MC 1 2 3 4 17snipezor1991100% (3)

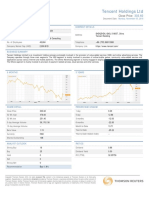

- Tencent Holdings LTD: Close PriceДокумент2 страницыTencent Holdings LTD: Close PricetrungОценок пока нет

- Powered: by Upgrad Education Private LimitedДокумент6 страницPowered: by Upgrad Education Private LimitedomОценок пока нет

- Tina Louise Company financial recordsДокумент4 страницыTina Louise Company financial recordsViệt DuyОценок пока нет

- Audit of Prepayment and Intangible Asset: Problem 6-1Документ42 страницыAudit of Prepayment and Intangible Asset: Problem 6-1Un knownОценок пока нет

- TM 10 - Financial Planning and ForecastingДокумент29 страницTM 10 - Financial Planning and ForecastingTul KuntullОценок пока нет

- CIMA F2 Course Notes PDFДокумент293 страницыCIMA F2 Course Notes PDFganОценок пока нет

- Group 4 - Assignment #5Документ57 страницGroup 4 - Assignment #5Rhad Lester C. MaestradoОценок пока нет

- EVA ExampleДокумент27 страницEVA Examplewelcome2jungleОценок пока нет

- Tutorial 3 QДокумент8 страницTutorial 3 Q杰小Оценок пока нет

- Ats StrategyДокумент9 страницAts StrategypradeephdОценок пока нет

- Forming Partnerships & Adjusting Sole Proprietor AccountsДокумент12 страницForming Partnerships & Adjusting Sole Proprietor Accountsۦۦ ۦۦ ۦۦ ۦۦОценок пока нет

- Calculating Cost of Capital and WACCДокумент21 страницаCalculating Cost of Capital and WACCMardi UmarОценок пока нет

- Chapter 1 Ethiopian Govt AcctingДокумент22 страницыChapter 1 Ethiopian Govt AcctingwubeОценок пока нет

- Analyze Financial StatementsДокумент2 страницыAnalyze Financial StatementsRabie HarounОценок пока нет

- Intermediate Accounting Volume 1 Chapter 5Документ179 страницIntermediate Accounting Volume 1 Chapter 5Catherine JaramillaОценок пока нет

- PPE Lecture NotesДокумент54 страницыPPE Lecture Notesmacmac29Оценок пока нет

- Financial Accounting FundamentalsДокумент54 страницыFinancial Accounting FundamentalsBiruk TesfayeОценок пока нет

- CF Assignment 2 Group 9Документ35 страницCF Assignment 2 Group 9rishabh tyagiОценок пока нет

- Al ArafahДокумент10 страницAl ArafahHasneen HasinОценок пока нет

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDДокумент10 страницAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarОценок пока нет

- Chapter 5Документ6 страницChapter 5Azi LheyОценок пока нет