Вам также может понравиться

- Chicago Booth Case Interviewing PDFДокумент16 страницChicago Booth Case Interviewing PDFTorresLiangОценок пока нет

- Asia Charts Super Rally (SR) Trading CourseДокумент5 страницAsia Charts Super Rally (SR) Trading Coursejancok asuОценок пока нет

- S&D Unit-2 PDFДокумент68 страницS&D Unit-2 PDFPranathi ShivaniОценок пока нет

- Screener Setup - GersteinДокумент86 страницScreener Setup - Gersteinsreekesh unnikrishnanОценок пока нет

- B2B Marketing PPT by SirДокумент115 страницB2B Marketing PPT by SirraghonittyОценок пока нет

- IIM Lucknow Case Solving Guide 2019Документ31 страницаIIM Lucknow Case Solving Guide 2019Isa100% (1)

- Bar Chart Patterns CMT 1Документ49 страницBar Chart Patterns CMT 1Mood OkОценок пока нет

- Strategic MarketingДокумент35 страницStrategic Marketingpikuoec86% (7)

- Retail Strategy and Planning Module IIДокумент228 страницRetail Strategy and Planning Module IIDEVANSH KOTHARIОценок пока нет

- Hedging With OptionsДокумент4 страницыHedging With OptionsboletodonОценок пока нет

- 2010-2011 Chicago Booth Case InterviewingДокумент16 страниц2010-2011 Chicago Booth Case Interviewingr_oko100% (4)

- Security Analysis (Begg) FA2016Документ8 страницSecurity Analysis (Begg) FA2016darwin12Оценок пока нет

- L4M5 Summarised NoteДокумент11 страницL4M5 Summarised NoteAmoge MbadiweОценок пока нет

- Lecture 5 - Competitive StrategyДокумент17 страницLecture 5 - Competitive StrategySachin kumarОценок пока нет

- Case in Point FrameworksДокумент33 страницыCase in Point FrameworksmahapatrarajeshranjanОценок пока нет

- Strategy and Strategic Management: InsightДокумент26 страницStrategy and Strategic Management: InsightNuruddin AsyifaОценок пока нет

- Frameworks To Use: FOUR P'S OF MARKETING: Product, Place, Promotion, PriceДокумент9 страницFrameworks To Use: FOUR P'S OF MARKETING: Product, Place, Promotion, Pricesbahadur86Оценок пока нет

- Lecture 5 - Competitive StrategyДокумент17 страницLecture 5 - Competitive StrategySachin kumarОценок пока нет

- Overview of Strategy: Competitive IntelligenceДокумент34 страницыOverview of Strategy: Competitive Intelligenceissu8789Оценок пока нет

- Hofer's Matrices and Directional PoliciesДокумент23 страницыHofer's Matrices and Directional Policiesshweta_4666480% (5)

- T Cikyr Udocf Gupresentactfit Ugbfort TVFT 7y9ghjiju9ons - 08052018120457Документ25 страницT Cikyr Udocf Gupresentactfit Ugbfort TVFT 7y9ghjiju9ons - 08052018120457hrshpatelОценок пока нет

- MM Chapter 4Документ33 страницыMM Chapter 4Robin Van SoCheat100% (2)

- Analysis, Segmentation & Consumer Buying Behavior: MarketДокумент41 страницаAnalysis, Segmentation & Consumer Buying Behavior: MarketpurvagadОценок пока нет

- M&E 2014 Session 9 Feasibility BBДокумент17 страницM&E 2014 Session 9 Feasibility BBsidОценок пока нет

- Strategy Under UncertaintyДокумент17 страницStrategy Under UncertaintySKОценок пока нет

- BS - L06 - Internal Business Environment AnalysisДокумент21 страницаBS - L06 - Internal Business Environment AnalysisRashad OrudjovОценок пока нет

- Wal Mart FinalДокумент28 страницWal Mart FinalThë FähãdОценок пока нет

- Competitive Strategies Marketing WarfareДокумент42 страницыCompetitive Strategies Marketing Warfarekartikkohli65Оценок пока нет

- Product Life Cycles (PLC)Документ27 страницProduct Life Cycles (PLC)anon_386582264Оценок пока нет

- Deep Value Investing Themes by Prof. Sanjay BakshiДокумент23 страницыDeep Value Investing Themes by Prof. Sanjay BakshiindianequityinvestorОценок пока нет

- Foundations of Business StrategyДокумент28 страницFoundations of Business StrategyInevitable CowboyОценок пока нет

- Introducing New Market OfferingsДокумент25 страницIntroducing New Market OfferingsRajat RanjanОценок пока нет

- Session 9sДокумент39 страницSession 9sSahil PandaОценок пока нет

- Technical Analysis & Market EfficiencyДокумент23 страницыTechnical Analysis & Market EfficiencyHamjaОценок пока нет

- MGMT 005 - Managing in A Vuca Context: Class 3Документ28 страницMGMT 005 - Managing in A Vuca Context: Class 3benОценок пока нет

- Strategic Management-1: Dr. Kamal Kishore SharmaДокумент45 страницStrategic Management-1: Dr. Kamal Kishore SharmaRadhakrishnan PadmanabhanОценок пока нет

- DBA 403 Lesson 7 & 8 November 2022Документ65 страницDBA 403 Lesson 7 & 8 November 2022EricОценок пока нет

- Marketing Gyaan - Summer PrepДокумент23 страницыMarketing Gyaan - Summer PrepDeepak PrasadОценок пока нет

- 01 Session Strat MGMT 2023FДокумент21 страница01 Session Strat MGMT 2023FYukinaMinatoОценок пока нет

- New Final MMДокумент13 страницNew Final MMNayeem SiddiqueОценок пока нет

- Lecture 6 - Qualitative ResearchДокумент62 страницыLecture 6 - Qualitative ResearchErasyl AydarkhanОценок пока нет

- Strategic Marketing MKT703: Virtual University of PakistanДокумент9 страницStrategic Marketing MKT703: Virtual University of PakistanRABIAОценок пока нет

- IntershipДокумент16 страницIntershipVijay DОценок пока нет

- Module 4 Offensive and Defensive StrategiesДокумент25 страницModule 4 Offensive and Defensive StrategieskjkaranОценок пока нет

- Honda Revisited. Debate - Fall 2019Документ5 страницHonda Revisited. Debate - Fall 2019Saad SohailОценок пока нет

- MM-Unit 2 - MR and Sales ForecastingДокумент25 страницMM-Unit 2 - MR and Sales ForecastingshyamОценок пока нет

- Week 6 Entrepreneurial Marketing PDFДокумент29 страницWeek 6 Entrepreneurial Marketing PDFAsifIsmayilovОценок пока нет

- Learning With Cases: MBAB 5P06Документ24 страницыLearning With Cases: MBAB 5P06Jayanthi HeeranandaniОценок пока нет

- RM6 MerchandisingДокумент28 страницRM6 MerchandisingbobymohanОценок пока нет

- Section 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityДокумент12 страницSection 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityJAYANT MAHAJANОценок пока нет

- Marketing in The Modern WorldДокумент36 страницMarketing in The Modern WorldElla B. CollantesОценок пока нет

- Advance Marketing Res. IIДокумент21 страницаAdvance Marketing Res. IIImranОценок пока нет

- Damodaran Chapter 1 Introduction To Valuation Winter 2020Документ28 страницDamodaran Chapter 1 Introduction To Valuation Winter 2020Jeff SОценок пока нет

- Exploring Marketing ResearchДокумент31 страницаExploring Marketing ResearchSam Sep A SixtyoneОценок пока нет

- MM ZG512 Manufacturing Strategy: Rajiv Gupta BITS Pilani Live Lecture 1Документ39 страницMM ZG512 Manufacturing Strategy: Rajiv Gupta BITS Pilani Live Lecture 1FUNTV5Оценок пока нет

- Ilovepdf MergedДокумент219 страницIlovepdf MergedFUNTV5Оценок пока нет

- EP EndSemДокумент195 страницEP EndSemSaksham GuptaОценок пока нет

- Topic 3:the External, Internal and Implementation of StrategyДокумент15 страницTopic 3:the External, Internal and Implementation of StrategyAbdulrahman AlMesferОценок пока нет

- Unit II Strategy Formulation Value Chain AnalysisДокумент19 страницUnit II Strategy Formulation Value Chain AnalysisAmit Pandey100% (1)

- Document PDFДокумент1 страницаDocument PDFboletodonОценок пока нет

- Strings: Eric MccreathДокумент4 страницыStrings: Eric MccreathboletodonОценок пока нет

- 156720287X PDFДокумент1 страница156720287X PDFboletodonОценок пока нет

- Math 60082Документ1 страницаMath 60082boletodonОценок пока нет

- Strategic Asset Allocation and Portfolio Optimal ChoiceДокумент4 страницыStrategic Asset Allocation and Portfolio Optimal ChoiceboletodonОценок пока нет

- Korean Conversations PDFДокумент4 страницыKorean Conversations PDFboletodonОценок пока нет

- Prob 21Документ1 страницаProb 21boletodonОценок пока нет

- Urn Process CheckДокумент1 страницаUrn Process CheckboletodonОценок пока нет

- Market Microstructure of Japanese ETF MarketДокумент1 страницаMarket Microstructure of Japanese ETF MarketboletodonОценок пока нет

- NotesДокумент1 страницаNotesboletodonОценок пока нет

- Course Otam32Документ4 страницыCourse Otam32Sushil MundelОценок пока нет

- Intersecting Curves: Cubic Linear IntersectionsДокумент1 страницаIntersecting Curves: Cubic Linear IntersectionsboletodonОценок пока нет

- New Strategies For Risk ManagementДокумент20 страницNew Strategies For Risk ManagementboletodonОценок пока нет

- Seeking AlphaДокумент3 страницыSeeking AlphaboletodonОценок пока нет

- Neyman Pearson LemmaДокумент10 страницNeyman Pearson LemmaboletodonОценок пока нет

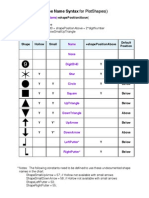

- AFL Shape NamesДокумент1 страницаAFL Shape NamesboletodonОценок пока нет