Вам также может понравиться

- HMCost3e SM Ch12Документ31 страницаHMCost3e SM Ch12Ahmed Abdel-FattahОценок пока нет

- Landscape With Invisible Hand by M.T. Anderson Chapter SamplerДокумент26 страницLandscape With Invisible Hand by M.T. Anderson Chapter SamplerCandlewick PressОценок пока нет

- Housing Loan AgreementДокумент5 страницHousing Loan AgreementVADeleon100% (1)

- Cost of CapitalДокумент44 страницыCost of CapitalSubia Hasan50% (4)

- CVP Analysis Review Problem SolutionДокумент3 страницыCVP Analysis Review Problem SolutionSUNNY BHUSHANОценок пока нет

- Man Acc 1Документ6 страницMan Acc 1Ange Buenaventura SalazarОценок пока нет

- 02 CVP Analysis For PrintingДокумент8 страниц02 CVP Analysis For Printingkristine claire50% (2)

- CVP Analysis Lecture Notes PDFДокумент32 страницыCVP Analysis Lecture Notes PDFReverie Sevilla100% (1)

- Brand Image ToyotaДокумент76 страницBrand Image ToyotaNishant Salunkhe100% (1)

- Profile On The Production of Shock Absorber (Spring)Документ26 страницProfile On The Production of Shock Absorber (Spring)ak123456Оценок пока нет

- How To Calculate Machine Hour RateДокумент4 страницыHow To Calculate Machine Hour Rateprasad_kcpОценок пока нет

- Management Advisory Services Transfer PricingДокумент6 страницManagement Advisory Services Transfer PricingLuming50% (2)

- Transfer PricingДокумент41 страницаTransfer PricingJudy Ann AcruzОценок пока нет

- Chapter 13 - Tor F and MCДокумент13 страницChapter 13 - Tor F and MCAnika100% (1)

- Module 2 - Asset Based Valuation For Going Concern Opportunities Part 1Документ2 страницыModule 2 - Asset Based Valuation For Going Concern Opportunities Part 1Marlou AbejuelaОценок пока нет

- Module 7 ELIMINATION OF UNREALIZED GAINS OR LOSSES ON INTERCOMPANY SALES OF PROPERTY AND EQUIPMENTДокумент33 страницыModule 7 ELIMINATION OF UNREALIZED GAINS OR LOSSES ON INTERCOMPANY SALES OF PROPERTY AND EQUIPMENTJulliena BakersОценок пока нет

- MA Cabrera 2010 - SolManДокумент4 страницыMA Cabrera 2010 - SolManCarla Francisco Domingo40% (5)

- Responsibility Accounting and TP Transfer PricingДокумент8 страницResponsibility Accounting and TP Transfer PricingAmdcОценок пока нет

- QUIZZER Cost of CapitalДокумент8 страницQUIZZER Cost of CapitalJOHN PAOLO EVORAОценок пока нет

- Capital Budgeting Lesson NewДокумент44 страницыCapital Budgeting Lesson NewLea MachadoОценок пока нет

- MSQ-01 - Cost Behavior CVP AnalysisДокумент7 страницMSQ-01 - Cost Behavior CVP AnalysisrochielanciolaОценок пока нет

- Activity-Based CostingДокумент2 страницыActivity-Based CostingClaire BarbaОценок пока нет

- Mas 3 Module 1 Fs AnalysisДокумент19 страницMas 3 Module 1 Fs AnalysisHazel Jane EsclamadaОценок пока нет

- Interactive Model of An EconomyДокумент142 страницыInteractive Model of An Economyrajraj999Оценок пока нет

- T02 - Capital BudgetingДокумент107 страницT02 - Capital BudgetingSuehОценок пока нет

- Notes On Responsibility AccountingДокумент6 страницNotes On Responsibility AccountingFlorie-May GarciaОценок пока нет

- Objectives, Roles, and Scope of Management AccountingДокумент4 страницыObjectives, Roles, and Scope of Management AccountingElla TuratoОценок пока нет

- AC13.1.1 Module 1 - Provisions, Contingencies, and Other LiabilitiesДокумент15 страницAC13.1.1 Module 1 - Provisions, Contingencies, and Other LiabilitiesRenelle HabacОценок пока нет

- Cost Volume Profit AnalysisДокумент6 страницCost Volume Profit AnalysisCindy CrausОценок пока нет

- Capital Budgeting ReviewerДокумент50 страницCapital Budgeting ReviewerPines MacapagalОценок пока нет

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoДокумент6 страницManila Cavite Laguna Cebu Cagayan de Oro Davaovane rondinaОценок пока нет

- MODULE 4 Relevant CostingДокумент9 страницMODULE 4 Relevant Costingsharielles /Оценок пока нет

- Activity Based Costing: Unit-Level Activities Batch-Level Activities Product-Level Activities Facility-Level ActivitiesДокумент3 страницыActivity Based Costing: Unit-Level Activities Batch-Level Activities Product-Level Activities Facility-Level ActivitiesPrincess Corine BurgosОценок пока нет

- Chapter 13 - Resp-Acctg PT 6Документ9 страницChapter 13 - Resp-Acctg PT 6Hiraya ManawariОценок пока нет

- L16 Problem On Transfer PricingДокумент20 страницL16 Problem On Transfer Pricingapi-382061990% (20)

- Ch13 Responsibility Accounting and Transfer PricingДокумент39 страницCh13 Responsibility Accounting and Transfer PricingChin-Chin Alvarez SabinianoОценок пока нет

- Variable Costing - Lecture NoteДокумент2 страницыVariable Costing - Lecture NoteCrestu JinОценок пока нет

- CVP AnalysisДокумент2 страницыCVP Analysisjhean dabatosОценок пока нет

- Running Head: FINAL PAPER 1Документ11 страницRunning Head: FINAL PAPER 1Iam TwinStorms0% (1)

- Auditors Report On Financial StatementДокумент4 страницыAuditors Report On Financial StatementKafonyi JohnОценок пока нет

- Decision Making and Relevant Costing TestДокумент61 страницаDecision Making and Relevant Costing TestSUBMERIN100% (1)

- 01 x01 Basic ConceptsДокумент10 страниц01 x01 Basic ConceptsXandae MempinОценок пока нет

- Ifrs 5 Acca AnswersДокумент2 страницыIfrs 5 Acca AnswersMonirul Islam MoniirrОценок пока нет

- Solution Manual Management Advisory Services by Agamata-77Документ3 страницыSolution Manual Management Advisory Services by Agamata-77AubreyGayleTrinidadDiaz0% (2)

- MA2 04 Relevant Costing Problem 20Документ4 страницыMA2 04 Relevant Costing Problem 20Joy Deocaris100% (1)

- 2.lesson 3 (Cost Behavior - Solution)Документ5 страниц2.lesson 3 (Cost Behavior - Solution)Aamir DossaniОценок пока нет

- Lecture 10 Relevant Costing PDFДокумент49 страницLecture 10 Relevant Costing PDFShweta Sridhar57% (7)

- Ac102 ch11Документ19 страницAc102 ch11Yenny Torro100% (1)

- Chapter 9 - Responsibility AccountingДокумент44 страницыChapter 9 - Responsibility Accountingsathishiim1985Оценок пока нет

- IMT Custom MachineДокумент3 страницыIMT Custom MachineSonia A. UsmanОценок пока нет

- Chapter 7 ProblemsДокумент4 страницыChapter 7 ProblemsZyraОценок пока нет

- Capital Budgeting Techniques NotesДокумент4 страницыCapital Budgeting Techniques NotesSenelwa Anaya83% (6)

- Variable Costing - Lecture NotesДокумент22 страницыVariable Costing - Lecture NotesRaghavОценок пока нет

- MasterbudgetДокумент154 страницыMasterbudgetrochielanciolaОценок пока нет

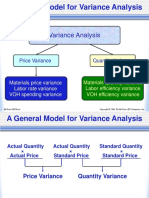

- Standard Costing and Variance AnalysisДокумент11 страницStandard Costing and Variance AnalysisMd AzimОценок пока нет

- Absorption Costing and Variable Costing QuizДокумент3 страницыAbsorption Costing and Variable Costing QuizKeir GaspanОценок пока нет

- Chapter 10 Practice ProblemsДокумент5 страницChapter 10 Practice ProblemsEvelyn RoldanОценок пока нет

- Tax Review - FinalsДокумент8 страницTax Review - FinalsRobert Castillo100% (2)

- Government Accounting Chapter 6Документ33 страницыGovernment Accounting Chapter 6Charlagne LacreОценок пока нет

- Responsibility Accounting and Transfer PricingДокумент23 страницыResponsibility Accounting and Transfer PricingNekibur DeepОценок пока нет

- Managerial AccountingMid Term Examination (1) - CONSULTAДокумент7 страницManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- High Low MethodДокумент4 страницыHigh Low MethodSamreen LodhiОценок пока нет

- Transfer Pricing To Be PrintedДокумент4 страницыTransfer Pricing To Be Printedalford sery CammayoОценок пока нет

- Chapter 5Документ26 страницChapter 5Hoàng Phương ThảoОценок пока нет

- Chapter 12 TRF PricingДокумент30 страницChapter 12 TRF Pricingleeroybradley44Оценок пока нет

- Finc600 Week 4 Required Quiz 1Документ10 страницFinc600 Week 4 Required Quiz 1Donald112100% (1)

- 04 Slides Tot R PDFДокумент31 страница04 Slides Tot R PDFSamiyah HaqueОценок пока нет

- Foreign Currency ConversionДокумент42 страницыForeign Currency ConversionAvish Shah100% (4)

- Quiz Bee - Pa1 & Toa - DifficultДокумент4 страницыQuiz Bee - Pa1 & Toa - DifficultskylavanderОценок пока нет

- Practice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Документ5 страницPractice Quiz - Quiz 2: Answer: Debit Accounts Receivable 26,250 Debit Freight Out 1,250 Credit Sales 27,500Kieht catcherОценок пока нет

- Bombay Textile Mill Strike PDFДокумент10 страницBombay Textile Mill Strike PDFPrasad BorkarОценок пока нет

- DS II Packet 2Документ31 страницаDS II Packet 2NitishОценок пока нет

- SixtДокумент7 страницSixtAmit BaharaОценок пока нет

- Chapter 6 Practice QuestionsДокумент9 страницChapter 6 Practice QuestionsAbdul Wajid Nazeer CheemaОценок пока нет

- Mock Exam MG T Acct 2019Документ3 страницыMock Exam MG T Acct 2019Lê Việt HoàngОценок пока нет

- Global Promotion StrategiesДокумент4 страницыGlobal Promotion StrategiesPatricia MumbiОценок пока нет

- Bab106 PDF EngДокумент21 страницаBab106 PDF EngdrrameshgargОценок пока нет

- Business Model CanvasДокумент2 страницыBusiness Model CanvasKorir BrianОценок пока нет

- Touchpoints in CRM of LICДокумент7 страницTouchpoints in CRM of LICShahnwaz AlamОценок пока нет

- Estimating The Cost of The Proposed Reston VPAC: Construction and Operating Costs, December 8, 2022Документ10 страницEstimating The Cost of The Proposed Reston VPAC: Construction and Operating Costs, December 8, 2022Terry MaynardОценок пока нет

- Share Based NotesДокумент5 страницShare Based NotesJP MJОценок пока нет

- Accounting For Specialized InstituitionsДокумент4 страницыAccounting For Specialized InstituitionsTitus Clement100% (1)

- B&D Case MMUGMДокумент8 страницB&D Case MMUGMrobbyapr100% (4)

- ECONOMIC ADMINISTRATION AND FINANCIAL MANAGEMENT First Paper: Business EconomicsДокумент4 страницыECONOMIC ADMINISTRATION AND FINANCIAL MANAGEMENT First Paper: Business EconomicsGuruKPOОценок пока нет

- My Heal Worldwide ReviewДокумент26 страницMy Heal Worldwide ReviewPaul HutchingsОценок пока нет

- Answer in BudgetingДокумент9 страницAnswer in BudgetingkheymiОценок пока нет

- Audit of Biological AssetsДокумент5 страницAudit of Biological AssetsTrisha Mae RodillasОценок пока нет

- What Is Costing?Документ27 страницWhat Is Costing?wickygeniusОценок пока нет

- Business Ethics Concepts & Cases: Manuel G. VelasquezДокумент19 страницBusiness Ethics Concepts & Cases: Manuel G. VelasquezAdhi KurniawanОценок пока нет

- Prep50 Economics Sample PagesДокумент5 страницPrep50 Economics Sample PagesOnyinyechi Samuel0% (1)