Вам также может понравиться

- Advanced Accounting 2:: Home Office, Branch and Agency - General ProceduresДокумент37 страницAdvanced Accounting 2:: Home Office, Branch and Agency - General ProceduresIzzy B94% (16)

- LBO Analysis TemplateДокумент11 страницLBO Analysis TemplateBobby Watkins75% (4)

- Government Accounting Final Examination With Answer and SolutionДокумент13 страницGovernment Accounting Final Examination With Answer and SolutionRheu Reyes100% (6)

- ACCOUNTING 3B Homework 3Документ3 страницыACCOUNTING 3B Homework 3Jasmin Escaño100% (1)

- Value InterviewsДокумент31 страницаValue InterviewsAmit Rana100% (1)

- P2 105 Agency Home Office and Branch Accounting Key AnswersДокумент6 страницP2 105 Agency Home Office and Branch Accounting Key AnswersHikari100% (1)

- Chapter 4 - Problems - Non-Current Assets Held For Sale and Discontinued OperationsДокумент17 страницChapter 4 - Problems - Non-Current Assets Held For Sale and Discontinued OperationsVictor TucoОценок пока нет

- Sales agency net income and cost of sales calculationДокумент27 страницSales agency net income and cost of sales calculationKandiz89% (9)

- Book Value per Share CalculationsДокумент3 страницыBook Value per Share CalculationsNor-hayne LucmanОценок пока нет

- Midterms Advanced Finac Acctg Set AДокумент9 страницMidterms Advanced Finac Acctg Set ALuisitoОценок пока нет

- Book Value per Share CalculationsДокумент5 страницBook Value per Share CalculationsXienaОценок пока нет

- Chapter 15 - EpsДокумент5 страницChapter 15 - EpsXiena100% (1)

- Kashato-Shirts Compress PDFДокумент20 страницKashato-Shirts Compress PDFApril Joy Tamayo100% (2)

- 85560539Документ2 страницы85560539Garp BarrocaОценок пока нет

- GEN 010 P1 ExamДокумент20 страницGEN 010 P1 ExamJulian Adam PagalОценок пока нет

- Shareholders' Equity QuestionsДокумент4 страницыShareholders' Equity QuestionsXienaОценок пока нет

- ACCTG-206B-FIRST-PREBOARD Without AnswerДокумент16 страницACCTG-206B-FIRST-PREBOARD Without AnswerRheu ReyesОценок пока нет

- Latin Words in Business Law Simplified Explanation - WPS OfficeДокумент2 страницыLatin Words in Business Law Simplified Explanation - WPS OfficeRheu Reyes50% (2)

- SheДокумент12 страницSheMark Anthony Tibule80% (5)

- LIABILITIES and EQUITY ALASTOY BSA 2Документ91 страницаLIABILITIES and EQUITY ALASTOY BSA 2JAY AUBREY PINEDAОценок пока нет

- Book value per share calculationДокумент2 страницыBook value per share calculationNicki Lyn Dela CruzОценок пока нет

- Danske Bank statement breakdownДокумент3 страницыDanske Bank statement breakdownamirОценок пока нет

- Income Taxes Problem SolvingДокумент3 страницыIncome Taxes Problem SolvingLara FloresОценок пока нет

- Chapter 19Документ42 страницыChapter 19Karissa GaviolaОценок пока нет

- Finac 3 TopicsДокумент9 страницFinac 3 TopicsCielo Mae Parungo60% (5)

- Book Value Per Share: Name: Date: QuizДокумент3 страницыBook Value Per Share: Name: Date: QuizLara FloresОценок пока нет

- Page 1 of 4 Chapter 4 - Intermediate Accounting 3Документ4 страницыPage 1 of 4 Chapter 4 - Intermediate Accounting 3happy2408230% (1)

- Cash BasisДокумент4 страницыCash BasisMark DiezОценок пока нет

- Thrift Corp. Prepaid Expenses QuizДокумент9 страницThrift Corp. Prepaid Expenses QuizKristine VertucioОценок пока нет

- Accounting ProbДокумент2 страницыAccounting ProbLino GumpalОценок пока нет

- Sol. Man. - Chapter 15 EpsДокумент12 страницSol. Man. - Chapter 15 Epsfinn mertensОценок пока нет

- Chapter 12 - Sh. Based Payments (Part 1)Документ6 страницChapter 12 - Sh. Based Payments (Part 1)Xiena100% (1)

- Ncpar Cup 2012Документ18 страницNcpar Cup 2012Allen Carambas Astro100% (2)

- Use The Following Information For The Next Four QuestionsДокумент1 страницаUse The Following Information For The Next Four QuestionsTine Vasiana DuermeОценок пока нет

- Investment in Equity - MCДокумент5 страницInvestment in Equity - MCLeisleiRago100% (1)

- Leases (PART I)Документ28 страницLeases (PART I)Carl Adrian Valdez100% (1)

- Practical Accounting Problems II SolutionsДокумент9 страницPractical Accounting Problems II SolutionsEunice BernalОценок пока нет

- INVESTMENT PROPERTY CHAPTERДокумент8 страницINVESTMENT PROPERTY CHAPTERPacifico HernandezОценок пока нет

- Entity A Issues Convertible Bonds With Face Amount ofДокумент1 страницаEntity A Issues Convertible Bonds With Face Amount ofNicole AguinaldoОценок пока нет

- Contest FARДокумент31 страницаContest FARTerence Jeff Tamondong67% (3)

- Negros Oriental State University: Instruction: Read The Problems Carefully and Answer It Correctly. Problem 1Документ1 страницаNegros Oriental State University: Instruction: Read The Problems Carefully and Answer It Correctly. Problem 1Mia Dy0% (1)

- B. Winnings Not Exceeding 10,000 D. Interest Income From Bank DepositsДокумент3 страницыB. Winnings Not Exceeding 10,000 D. Interest Income From Bank DepositsVanesa Calimag ClementeОценок пока нет

- Accounting for Derivatives and Hedging Transactions (Part 3Документ13 страницAccounting for Derivatives and Hedging Transactions (Part 3Sheed ChiuОценок пока нет

- Chapter 09Документ16 страницChapter 09FireBОценок пока нет

- Practical Accounting 2 (P2)Документ12 страницPractical Accounting 2 (P2)Nico evansОценок пока нет

- Absorption vs Variable Costing CalculationsДокумент6 страницAbsorption vs Variable Costing CalculationsVexana NecromancerОценок пока нет

- Chapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Документ20 страницChapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Alvin Jheii Sioco Alfonso0% (1)

- SMEs (Students Guide)Документ11 страницSMEs (Students Guide)Erica CaliuagОценок пока нет

- Name: - Section: - Schedule: - Class Number: - DateДокумент4 страницыName: - Section: - Schedule: - Class Number: - Datechristine_pineda_2Оценок пока нет

- Final Drill No. 2Документ8 страницFinal Drill No. 2anon_492858278Оценок пока нет

- Tips on Accounting for Troubled Debt Restructuring and BondsДокумент35 страницTips on Accounting for Troubled Debt Restructuring and BondsLexter Dave C EstoqueОценок пока нет

- QUIZ REVIEW Homework Tutorial Chapter 5Документ5 страницQUIZ REVIEW Homework Tutorial Chapter 5Cody TarantinoОценок пока нет

- Exercises/Assignments Answer The Following ProblemsДокумент22 страницыExercises/Assignments Answer The Following ProblemsLuigi Enderez BalucanОценок пока нет

- Pas 8Документ5 страницPas 8Angelica Danuco25% (4)

- Acquiring IMMATURE: Estimating GoodwillДокумент1 страницаAcquiring IMMATURE: Estimating GoodwillRiselle Ann Sanchez50% (2)

- Premiums and WarrantiesДокумент3 страницыPremiums and WarrantiesMicaella Grande50% (2)

- ECO 444 Investments Test Bank-No AnswersДокумент17 страницECO 444 Investments Test Bank-No AnswersAllan Genesis Romblon100% (1)

- Answer Key Week 4Документ10 страницAnswer Key Week 4Chin FiguraОценок пока нет

- Use The Following Information For The Next Two QuestionsДокумент7 страницUse The Following Information For The Next Two QuestionsJohn Carlo Aquino0% (1)

- PDF Acc 109 Intermediate Accounting 4 Mock Phinma Exam 2s1920 Key Answer - CompressДокумент19 страницPDF Acc 109 Intermediate Accounting 4 Mock Phinma Exam 2s1920 Key Answer - CompressGeraldine Martinez DonaireОценок пока нет

- Leases Part 2: Name: Date: Professor: Section: Score: Quiz 1Документ2 страницыLeases Part 2: Name: Date: Professor: Section: Score: Quiz 1Jamie Rose AragonesОценок пока нет

- Lease calculation problemДокумент7 страницLease calculation problemGelo Owss33% (9)

- Chapter 03Документ30 страницChapter 03ajbalcitaОценок пока нет

- MergerДокумент3 страницыMergerJohn BalanquitОценок пока нет

- Lecture Notes On Quasi-ReorganizationДокумент2 страницыLecture Notes On Quasi-ReorganizationalyssaОценок пока нет

- Takehome Assessment No. 4Документ9 страницTakehome Assessment No. 4Raezel Carla Santos Fontanilla0% (4)

- Accounting 162 - Material 006: For The Next Few RequirementsДокумент3 страницыAccounting 162 - Material 006: For The Next Few RequirementsAngelli LamiqueОценок пока нет

- On January 1Документ3 страницыOn January 1Jude Santos0% (1)

- Stock Acquisition Quiz 100% AnswerДокумент2 страницыStock Acquisition Quiz 100% AnswerJohn BalanquitОценок пока нет

- QUIZ_CHAPTER-14_BOOK-VALUE-PER-SHARE_2021Документ5 страницQUIZ_CHAPTER-14_BOOK-VALUE-PER-SHARE_2021Krezza Amor MabanОценок пока нет

- Course:: Financial AccountingДокумент4 страницыCourse:: Financial AccountingNudrat ZaraОценок пока нет

- BVPS For DiscussionДокумент2 страницыBVPS For DiscussionSpongebob SquarepantsОценок пока нет

- Accounting RemovedДокумент204 страницыAccounting RemovedHaris Storage1Оценок пока нет

- Answer 4 - Excel For Diff. Acctg.Документ42 страницыAnswer 4 - Excel For Diff. Acctg.Rheu ReyesОценок пока нет

- Vaughn Co current liabilitiesДокумент3 страницыVaughn Co current liabilitiesRheu ReyesОценок пока нет

- General Accounting 3 - Express Handling and DeliveryДокумент9 страницGeneral Accounting 3 - Express Handling and DeliveryRheu ReyesОценок пока нет

- Answer 3 - "Different Random Answers To Various Accounting Questions"Документ21 страницаAnswer 3 - "Different Random Answers To Various Accounting Questions"Rheu ReyesОценок пока нет

- Answer 2 - Answers Only For Crane Company, Swifty Company, Pharaoh Company, and Random Accounting QuestionsДокумент10 страницAnswer 2 - Answers Only For Crane Company, Swifty Company, Pharaoh Company, and Random Accounting QuestionsRheu ReyesОценок пока нет

- Answer 5 - " Modern Appliances Corporation"Документ4 страницыAnswer 5 - " Modern Appliances Corporation"Rheu ReyesОценок пока нет

- Accounting for margin of safety, break-even pointДокумент5 страницAccounting for margin of safety, break-even pointRheu ReyesОценок пока нет

- Answer 1 - Blue Bill CorporationДокумент2 страницыAnswer 1 - Blue Bill CorporationRheu ReyesОценок пока нет

- TRAIN HighlightsДокумент86 страницTRAIN HighlightsJehugem BayawaОценок пока нет

- Business Plan ProposalДокумент4 страницыBusiness Plan ProposalRheu ReyesОценок пока нет

- General Accounting 1 - Indianola Pharmaceutical CompanyДокумент7 страницGeneral Accounting 1 - Indianola Pharmaceutical CompanyRheu ReyesОценок пока нет

- Practical Accounting 1Документ32 страницыPractical Accounting 1EdenA.Mata100% (9)

- Activities On CIP and BAsket Value With AnswersДокумент2 страницыActivities On CIP and BAsket Value With AnswersRheu ReyesОценок пока нет

- Aud Theo Explanation From 72-108Документ11 страницAud Theo Explanation From 72-108Rheu ReyesОценок пока нет

- Nationalized or Partly Nationalized Corporations 1. 100 % FilipinosДокумент1 страницаNationalized or Partly Nationalized Corporations 1. 100 % FilipinosRheu ReyesОценок пока нет

- Form For Application For Acad ScholarshipДокумент1 страницаForm For Application For Acad ScholarshipRheu ReyesОценок пока нет

- AuditingДокумент5 страницAuditingJona Mae Milla0% (1)

- Accounting 204anfinal Exams Compilation Old NotesДокумент1 страницаAccounting 204anfinal Exams Compilation Old NotesRheu ReyesОценок пока нет

- Aud Theo Explanation From 72-108Документ11 страницAud Theo Explanation From 72-108Rheu ReyesОценок пока нет

- Auditing Theory FinalsДокумент17 страницAuditing Theory FinalsRheu ReyesОценок пока нет

- Acctg 205A Quiz NOV. 6,2020Документ3 страницыAcctg 205A Quiz NOV. 6,2020Rheu ReyesОценок пока нет

- Learner Enrollment and Survey Form: Grade Level and School InformationДокумент2 страницыLearner Enrollment and Survey Form: Grade Level and School InformationCyrus Emmanuel Casil100% (1)

- The Sound of Stone: Income Statement For The Year Ended Decemeber 31, 2013Документ5 страницThe Sound of Stone: Income Statement For The Year Ended Decemeber 31, 2013Wendy Janine BalucoОценок пока нет

- Accounting & Finance Module: B: Ca R. C. JoshiДокумент131 страницаAccounting & Finance Module: B: Ca R. C. JoshiRahul GuptaОценок пока нет

- Krakatau Steel EVA AnalysisДокумент5 страницKrakatau Steel EVA AnalysisYudhatama MohamadОценок пока нет

- Q.1) The Following Trial Balance Has Been Extracted From The Books of Rajesh On 31st December, 2016Документ11 страницQ.1) The Following Trial Balance Has Been Extracted From The Books of Rajesh On 31st December, 2016Aarya Khedekar100% (2)

- Stock Market Workshop PDFДокумент3 страницыStock Market Workshop PDFLokesh Basappa50% (2)

- Far-1 Revaluation JE 2Документ2 страницыFar-1 Revaluation JE 2Janie HookeОценок пока нет

- Cash Flow and Financial PlanningДокумент64 страницыCash Flow and Financial PlanningKARL PASCUAОценок пока нет

- Test Bank For Australian Financial Accounting 7th Edition by Deegan PDFДокумент14 страницTest Bank For Australian Financial Accounting 7th Edition by Deegan PDFGen S.Оценок пока нет

- Module 1 Introduction To Accounting For BSOA &1BSENTREPДокумент21 страницаModule 1 Introduction To Accounting For BSOA &1BSENTREPjilliantrcieОценок пока нет

- Barclays - Tesco1Q2324salesreview-strongUKLFLsales (90) - Jun - 16 - 2023Документ22 страницыBarclays - Tesco1Q2324salesreview-strongUKLFLsales (90) - Jun - 16 - 2023Edward LaiОценок пока нет

- NestleДокумент8 страницNestleYasmin khanОценок пока нет

- Tran Date Value Date Tran Particular Credit Debit BalanceДокумент96 страницTran Date Value Date Tran Particular Credit Debit BalanceGenji MaОценок пока нет

- Karnataka II PUC Accountancy Sample Question Paper 18Документ6 страницKarnataka II PUC Accountancy Sample Question Paper 18Kishu KishoreОценок пока нет

- Fixed AssetsДокумент46 страницFixed AssetsSprancenatu Lavinia0% (1)

- Advantages and Disadvantages of An IPOДокумент2 страницыAdvantages and Disadvantages of An IPOHemali100% (1)

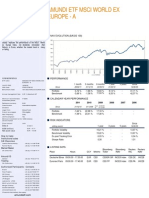

- Amundi ETF Tracks World ex Europe StocksДокумент2 страницыAmundi ETF Tracks World ex Europe Stockshp24714303Оценок пока нет

- Due Diligence Checklist - Small Business - SME - M&a - Caprica OnlineДокумент3 страницыDue Diligence Checklist - Small Business - SME - M&a - Caprica OnlineHungreo411Оценок пока нет

- INENTITYДокумент43 страницыINENTITYsriatluriОценок пока нет

- Performance Analysis of Life Insurance Companies in BangladeshДокумент41 страницаPerformance Analysis of Life Insurance Companies in Bangladeshtauhidult67% (3)

- Gale BrewerДокумент3 страницыGale BrewerWulandariОценок пока нет

- Variableabsorption CostingДокумент77 страницVariableabsorption Costingandrea arapocОценок пока нет

- Accounting What The Numbers Mean 11th Edition Marshall Test BankДокумент43 страницыAccounting What The Numbers Mean 11th Edition Marshall Test Bankmalabarhumane088100% (28)

- Company Law ct1Документ7 страницCompany Law ct1TANISHA ISLAM SHENIZОценок пока нет

- AIF Guide to Alternative Investment Funds in IndiaДокумент33 страницыAIF Guide to Alternative Investment Funds in IndiaHarsh ChhabraОценок пока нет

- WoolworthsДокумент55 страницWoolworthsjohnsmithlovestodo69Оценок пока нет