Вам также может понравиться

- Lecture 5 - Customer Relationship ManagementДокумент5 страницLecture 5 - Customer Relationship Managementmariam1990hatemОценок пока нет

- Warranty Cost Models State-Of-Art A Practical ReviewДокумент10 страницWarranty Cost Models State-Of-Art A Practical Reviewniketa engineerОценок пока нет

- Maintenance BusinessДокумент13 страницMaintenance BusinessArdyas Wisnu BaskoroОценок пока нет

- Building A Competitive Edge MXДокумент4 страницыBuilding A Competitive Edge MXsgieldaОценок пока нет

- Why Service Recovery Fails: Tensions Among Customer, Employee, and Process PerspectivesДокумент21 страницаWhy Service Recovery Fails: Tensions Among Customer, Employee, and Process PerspectivesAltair CamargoОценок пока нет

- Handling Customer Complaints - A Best Practice GuideДокумент8 страницHandling Customer Complaints - A Best Practice GuideDina Tarek TomoumОценок пока нет

- Handling Customer Complaints - A Best Practice GuideДокумент8 страницHandling Customer Complaints - A Best Practice GuideCharlie KebasoОценок пока нет

- Quality Management, in Which Manufacturers Strive To Create An Environment That Will EnableДокумент1 страницаQuality Management, in Which Manufacturers Strive To Create An Environment That Will Enablebarlie3824Оценок пока нет

- Customer Relationship Management in Organizations: January 2011Документ10 страницCustomer Relationship Management in Organizations: January 2011Ayaz RazaОценок пока нет

- Value Driven Maintenance & Asset Management: Competing With Aging AssetsДокумент5 страницValue Driven Maintenance & Asset Management: Competing With Aging AssetsMILTON ANDRES ANGULO MORRISОценок пока нет

- The Performance Prism in Practice: Measuring Business Excellence June 2001Документ8 страницThe Performance Prism in Practice: Measuring Business Excellence June 2001John CastilloОценок пока нет

- 202 - Varun Thomas - 4AДокумент9 страниц202 - Varun Thomas - 4AVarun ThomasОценок пока нет

- External Influences On Management Accounting: Unit 1 SectionДокумент4 страницыExternal Influences On Management Accounting: Unit 1 SectionBabamu Kalmoni JaatoОценок пока нет

- B1 PDFДокумент5 страницB1 PDFkhktvnОценок пока нет

- Assessing PoorДокумент13 страницAssessing PoorPeter AbesigaОценок пока нет

- BciДокумент19 страницBciblutnt0% (1)

- The Efficient Practice: Transform and Optimize Your Financial Advisory Practice for Greater ProfitsОт EverandThe Efficient Practice: Transform and Optimize Your Financial Advisory Practice for Greater ProfitsОценок пока нет

- How to Manage Future Costs and Risks Using Costing and MethodsОт EverandHow to Manage Future Costs and Risks Using Costing and MethodsОценок пока нет

- The Customer Relationship Management Process Its MДокумент15 страницThe Customer Relationship Management Process Its MBruna DiléoОценок пока нет

- THESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementДокумент46 страницTHESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementVon Ianelle AguilaОценок пока нет

- Benefits of Maintenance Management SoftwareДокумент5 страницBenefits of Maintenance Management Softwaregranados.saderОценок пока нет

- GX Deloitte Uk ECRS ReportДокумент21 страницаGX Deloitte Uk ECRS Reportsimha1177Оценок пока нет

- The Customer Service Management ProcessДокумент2 страницыThe Customer Service Management ProcessFahimОценок пока нет

- The Logic of Management Consulting 2Документ27 страницThe Logic of Management Consulting 2Xyz YxzОценок пока нет

- Document Management and Printing Solutions For The Insurance Industry 1Документ13 страницDocument Management and Printing Solutions For The Insurance Industry 1api-420810931Оценок пока нет

- Customer Relationship Management in Organizations: January 2011Документ10 страницCustomer Relationship Management in Organizations: January 2011Yudha PriambodoОценок пока нет

- Management Accounting Techniques 1Документ15 страницManagement Accounting Techniques 1Ekin BaharinОценок пока нет

- Customer Complaints Management Drive Loyality and Mitigate Risk Across Your OrganizationДокумент10 страницCustomer Complaints Management Drive Loyality and Mitigate Risk Across Your Organizationtolga aktasОценок пока нет

- Customer ValueДокумент17 страницCustomer ValueK BОценок пока нет

- Sustainable Business Practices: Balancing Profit and Environmental ResponsibilityОт EverandSustainable Business Practices: Balancing Profit and Environmental ResponsibilityОценок пока нет

- What's A Business Case and FAQДокумент14 страницWhat's A Business Case and FAQshashisxОценок пока нет

- Mayanja Yasin ProposalДокумент15 страницMayanja Yasin ProposalSuleiman AbdulОценок пока нет

- Weirather Mcs Case9 Ch11Документ5 страницWeirather Mcs Case9 Ch11Johannes WeiratherОценок пока нет

- Strategic Management of Professional Service Firms: Theory and PracticeОт EverandStrategic Management of Professional Service Firms: Theory and PracticeОценок пока нет

- The Customer Relationship Management Process Its M PDFДокумент15 страницThe Customer Relationship Management Process Its M PDFBruna DiléoОценок пока нет

- quản,lý và ksoat cp ẩnДокумент4 страницыquản,lý và ksoat cp ẩnNguyễn Thị Hồng NhânОценок пока нет

- Management AccountingДокумент13 страницManagement AccountingEr Amit MathurОценок пока нет

- Mcdonald 2016Документ10 страницMcdonald 2016Andrika SaputraОценок пока нет

- White Paper Oracle Vertical CRM Applications: Realizing Business Benefit Through Industry Best PracticesДокумент11 страницWhite Paper Oracle Vertical CRM Applications: Realizing Business Benefit Through Industry Best PracticesSIVAKUMAR_GОценок пока нет

- Unit-9 Introduction To Service OperationДокумент11 страницUnit-9 Introduction To Service Operationdubeyvimal389Оценок пока нет

- Insurance Industry ProcessesДокумент16 страницInsurance Industry Processesadeptia100% (1)

- Unit I-III Cost PDFДокумент83 страницыUnit I-III Cost PDFRupak ChandnaОценок пока нет

- Continuous Assessment 31 January 2022. Department of Information Systems Course: Ifs 413 - Business Process ReengineeringДокумент35 страницContinuous Assessment 31 January 2022. Department of Information Systems Course: Ifs 413 - Business Process ReengineeringToby TeddyОценок пока нет

- The 8D Methodology An Effective Way To Reduce Recu PDFДокумент7 страницThe 8D Methodology An Effective Way To Reduce Recu PDFDany AriasОценок пока нет

- Production NotesДокумент19 страницProduction NotesShabi AhmedОценок пока нет

- 论文题目 (Paper Title) : Earnings Management: A Study on the origination,Документ9 страниц论文题目 (Paper Title) : Earnings Management: A Study on the origination,Md. Asiqur RahmanОценок пока нет

- Making The Most of Customer Complaints - Handling ComplaintsДокумент31 страницаMaking The Most of Customer Complaints - Handling ComplaintsNele KrivokapićОценок пока нет

- Business Assurance More Than ERMДокумент5 страницBusiness Assurance More Than ERMAssuringBusinessОценок пока нет

- Implementing Third-Party Assurance in Integrated Reporting: Companies ' Motivation and Auditors' RoleДокумент25 страницImplementing Third-Party Assurance in Integrated Reporting: Companies ' Motivation and Auditors' RolemariОценок пока нет

- Jurnal 3Документ13 страницJurnal 3Heldi SahputraОценок пока нет

- STRATEGIC COST MANAGEMENT Chapter 3Документ3 страницыSTRATEGIC COST MANAGEMENT Chapter 3JanelleОценок пока нет

- OM Operation Management Module One 1Документ6 страницOM Operation Management Module One 1Eric GuapinОценок пока нет

- Chapter 1 Answer Cost Accounting PDFДокумент5 страницChapter 1 Answer Cost Accounting PDFCris VillarОценок пока нет

- Introduction To Managerial Accounting: Discussion QuestionsДокумент5 страницIntroduction To Managerial Accounting: Discussion QuestionsParth GandhiОценок пока нет

- Cut Costs, Grow Stronger : A Strategic Approach to What to Cut and What to KeepОт EverandCut Costs, Grow Stronger : A Strategic Approach to What to Cut and What to KeepРейтинг: 5 из 5 звезд5/5 (1)

- 239 2371 3 PBДокумент6 страниц239 2371 3 PBRituОценок пока нет

- Chapter 2Документ51 страницаChapter 2payal joshiОценок пока нет

- Module 3 Learner GuideДокумент228 страницModule 3 Learner Guidealex.cooney4Оценок пока нет

- MCQ's On Intellectual Property Act - SpeakHRДокумент6 страницMCQ's On Intellectual Property Act - SpeakHRTkОценок пока нет

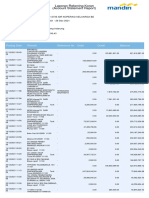

- RK Mandiri SPДокумент2 страницыRK Mandiri SPakun hiburanОценок пока нет

- Quant Checklist 476 by Aashish Arora For Bank Exams 2024Документ118 страницQuant Checklist 476 by Aashish Arora For Bank Exams 2024palanimesh420Оценок пока нет

- Paper ThanhTram ThanhSn2019 Version1 ConferenceICSAFE-ENДокумент66 страницPaper ThanhTram ThanhSn2019 Version1 ConferenceICSAFE-ENTHU PHAN THI THANHОценок пока нет

- Final RFPs For Medical Devices Study (3-07-2023) v1.5Документ9 страницFinal RFPs For Medical Devices Study (3-07-2023) v1.5Hafiz Saddique MalikОценок пока нет

- Demand, Supply and Manufacturing Planning and ControlДокумент482 страницыDemand, Supply and Manufacturing Planning and ControlDipannita DasОценок пока нет

- Smart TrolleyДокумент41 страницаSmart Trolleyhelene ganawaОценок пока нет

- Ken Lipinski - Resume & Cover Letter - KareoДокумент3 страницыKen Lipinski - Resume & Cover Letter - KareoJoshua YoungОценок пока нет

- Investing in Breakthrough Corporate Venture CapitalДокумент64 страницыInvesting in Breakthrough Corporate Venture CapitalAJ MerloОценок пока нет

- Cost Control and Cost ReductionДокумент34 страницыCost Control and Cost Reductionshreepal1940% (5)

- Final Term Topics Professional Development and Applied EthicsДокумент12 страницFinal Term Topics Professional Development and Applied EthicsAngelica Mae Ablanque100% (1)

- Discussion Materials Prepared by Lazard Asia (Hong Kong) LimitedДокумент67 страницDiscussion Materials Prepared by Lazard Asia (Hong Kong) LimitedpriyanshuОценок пока нет

- Vanraj TractorsДокумент24 страницыVanraj TractorsAjay Choudhary100% (1)

- Digital Economy For Africa (DE4A) - OverviewДокумент3 страницыDigital Economy For Africa (DE4A) - OverviewAbuniGamaОценок пока нет

- Analysis of Investment Options Mba ProjectДокумент59 страницAnalysis of Investment Options Mba Projectbalki12383% (12)

- Position PaperДокумент3 страницыPosition PaperJeffrey MedinaОценок пока нет

- IIM Kashipur: Foundation For Innovation and Entrepreneurship DevelopmentДокумент2 страницыIIM Kashipur: Foundation For Innovation and Entrepreneurship DevelopmentNikhil KumarОценок пока нет

- Ru2000 Membershiplist 20180625 0Документ29 страницRu2000 Membershiplist 20180625 0Jameson CorderoОценок пока нет

- Working Captal ManagementДокумент42 страницыWorking Captal Managementjonna mae rapanutОценок пока нет

- Known Businesses With Links To Steven C. Brigham-FinalДокумент4 страницыKnown Businesses With Links To Steven C. Brigham-FinalCheryl SullengerОценок пока нет

- Distribution Channel Literature ReviewДокумент7 страницDistribution Channel Literature Reviewc5g10bt2100% (1)

- The Sale of Goods ActДокумент19 страницThe Sale of Goods Actdee deeОценок пока нет

- 7Ps of Marketing MixДокумент67 страниц7Ps of Marketing MixMslkОценок пока нет

- Development of A Design - Ime Estimation Model For Complex Engineering ProcessesДокумент10 страницDevelopment of A Design - Ime Estimation Model For Complex Engineering ProcessesJosip StjepandicОценок пока нет

- MRP Vs APSДокумент1 страницаMRP Vs APSVishwanath RavindranОценок пока нет

- Security Licence Renewal ReciptДокумент1 страницаSecurity Licence Renewal ReciptAyyappan AlaguОценок пока нет

- Sample - China BIM in Construction Market - Industry Dynamics Market Size and Opportunity Forecast To 2027Документ72 страницыSample - China BIM in Construction Market - Industry Dynamics Market Size and Opportunity Forecast To 2027Jackie YongОценок пока нет

- International MarketingДокумент26 страницInternational MarketingSikiru Issa NuhuОценок пока нет

- Avon Rewards Booklet October 2022 and Training2Документ9 страницAvon Rewards Booklet October 2022 and Training2Nazneen AliОценок пока нет