Вам также может понравиться

- Digital Realty Trust Inc: Analyst's NotesДокумент5 страницDigital Realty Trust Inc: Analyst's NotesJeff SturgeonОценок пока нет

- Argus Analyst ReportДокумент7 страницArgus Analyst ReportEr DiОценок пока нет

- NeuStar Argus 12.6.08Документ8 страницNeuStar Argus 12.6.08Dinesh MoorjaniОценок пока нет

- 7 Undervalued Stocks With High Growth Potential Over Next One YearДокумент6 страниц7 Undervalued Stocks With High Growth Potential Over Next One Yearhoney1002Оценок пока нет

- Argus - TMUSДокумент6 страницArgus - TMUSJeff SturgeonОценок пока нет

- EPD - Argus PDFДокумент5 страницEPD - Argus PDFJeff SturgeonОценок пока нет

- Intel - Argus - Q1-09 - Q4 EarningsДокумент5 страницIntel - Argus - Q1-09 - Q4 EarningsBUGGI1000Оценок пока нет

- Structured Products Solutions - Tata Capital Financial ServicesДокумент19 страницStructured Products Solutions - Tata Capital Financial ServicesAnonymous bdUhUNm7JОценок пока нет

- Expected Returns For Real Estate PDFДокумент12 страницExpected Returns For Real Estate PDFJaja JAОценок пока нет

- REITs - Listed REITs Have Failed To Sparkle - The Economic TimesДокумент2 страницыREITs - Listed REITs Have Failed To Sparkle - The Economic Timeskausthubh vitthalОценок пока нет

- HP - Argus PDFДокумент5 страницHP - Argus PDFJeff SturgeonОценок пока нет

- Duluth Holdings Inc.: October 8, 2018 DLTH - NasdaqДокумент3 страницыDuluth Holdings Inc.: October 8, 2018 DLTH - Nasdaqashok yadavОценок пока нет

- L 3 Ss 12 Los 25Документ12 страницL 3 Ss 12 Los 25pier AcostaОценок пока нет

- Insights Looking Overseas Amid Property Market Correction PDFДокумент310 страницInsights Looking Overseas Amid Property Market Correction PDFmonami.sankarsanОценок пока нет

- Initiating Coverage of Single-Family Rental Reits With Favorable View - Buy SFRДокумент50 страницInitiating Coverage of Single-Family Rental Reits With Favorable View - Buy SFRtempvjОценок пока нет

- Netflix Inc.: Content Ramp Adding Torque To The FlywheelДокумент30 страницNetflix Inc.: Content Ramp Adding Torque To The FlywheelKeyaОценок пока нет

- Netflix Inc.: Content Ramp Adding Torque To The FlywheelДокумент30 страницNetflix Inc.: Content Ramp Adding Torque To The FlywheelManvinder SinghОценок пока нет

- OKE - ArgusДокумент5 страницOKE - ArgusJeff SturgeonОценок пока нет

- Cie LKPДокумент9 страницCie LKPRajiv HandaОценок пока нет

- Sep 2017 Page 1Документ27 страницSep 2017 Page 1ajujkОценок пока нет

- Convertible Bonds Yield SingaporeДокумент18 страницConvertible Bonds Yield Singaporeapi-26109152Оценок пока нет

- Coffee With Dave 042110Документ3 страницыCoffee With Dave 042110Glenn BuschОценок пока нет

- WH at Is T H e M Ar K Et Doin G? Take A Look at The M Ajor Indices (SPY, IWM, QQQ) and The Equity SectorsДокумент4 страницыWH at Is T H e M Ar K Et Doin G? Take A Look at The M Ajor Indices (SPY, IWM, QQQ) and The Equity SectorsCSОценок пока нет

- Edelweiss Report PDFДокумент218 страницEdelweiss Report PDFabhilodhiyaОценок пока нет

- S&P Morning Briefing 20 November 2018Документ7 страницS&P Morning Briefing 20 November 2018Abdullah18Оценок пока нет

- Nasdaq 100 Index Product GuideДокумент3 страницыNasdaq 100 Index Product GuideNdemeОценок пока нет

- Earn Higher Returns With A Low Risk Asset Class: Drip CapitalДокумент2 страницыEarn Higher Returns With A Low Risk Asset Class: Drip CapitalMohammed Abrar AsifОценок пока нет

- Broking - Update - Mar19 - HDFC Sec-201903191711243793044Документ16 страницBroking - Update - Mar19 - HDFC Sec-201903191711243793044Sanjay RijhwaniОценок пока нет

- MSCI Real Estate Pitch DeckДокумент58 страницMSCI Real Estate Pitch DeckRianovel MareОценок пока нет

- Capital Market - Thematic Report - 28 Nov 22Документ123 страницыCapital Market - Thematic Report - 28 Nov 22bharat.divineОценок пока нет

- Cheat Sheet For Valuation (2) - 1Документ2 страницыCheat Sheet For Valuation (2) - 1RISHAV BAIDОценок пока нет

- India Grid Trust: Recalibrating The Growth PitchДокумент19 страницIndia Grid Trust: Recalibrating The Growth Pitchrchawdhry123Оценок пока нет

- Deck How To Trade SlidesДокумент39 страницDeck How To Trade SlidesN.a. M. TandayagОценок пока нет

- India REIT Paper - Nov 20Документ10 страницIndia REIT Paper - Nov 20Maitri maheshwariОценок пока нет

- Constructing A Systematic Asset Allocation Strategy:: The S&P Dynamic Tactical Allocation IndexДокумент26 страницConstructing A Systematic Asset Allocation Strategy:: The S&P Dynamic Tactical Allocation IndexSrinivasaОценок пока нет

- IDT Corp. (NYSE: IDT) : Unlocking Value With One of The World's Best Capital AllocatorsДокумент55 страницIDT Corp. (NYSE: IDT) : Unlocking Value With One of The World's Best Capital Allocatorsatgy1996Оценок пока нет

- Ratio AnalysisДокумент25 страницRatio AnalysisJulveОценок пока нет

- S&P Morning Briefing 4 Dec. 2018Документ8 страницS&P Morning Briefing 4 Dec. 2018Abdullah18Оценок пока нет

- Pidilite Industries: Robust Recovery Margin Pressure AheadДокумент15 страницPidilite Industries: Robust Recovery Margin Pressure AheadIS group 7Оценок пока нет

- Infosys: ESG Disclosure ScoreДокумент13 страницInfosys: ESG Disclosure ScoreShayan RCОценок пока нет

- Kotak International REIT FOF: India's First Global REIT Fund of FundДокумент27 страницKotak International REIT FOF: India's First Global REIT Fund of FundVinit ShahОценок пока нет

- SISF Global Equity SA enДокумент2 страницыSISF Global Equity SA enpcbethellОценок пока нет

- Case StudyДокумент4 страницыCase StudyJAYESH VAYAОценок пока нет

- Chapter12 ExercisesДокумент6 страницChapter12 ExercisesCharis ElОценок пока нет

- Akre Focus Fund Commentary First Quarter 2021Документ2 страницыAkre Focus Fund Commentary First Quarter 2021Pranab PattanaikОценок пока нет

- Investment Banking Valuation - Equity Value - and Enterprise ValueДокумент18 страницInvestment Banking Valuation - Equity Value - and Enterprise ValuejyguygОценок пока нет

- GS Cross Asset CarryДокумент16 страницGS Cross Asset CarryHarry MarkowitzОценок пока нет

- Prudent Investing: Invest in Mirae Asset Prudence Fund (MAPF)Документ2 страницыPrudent Investing: Invest in Mirae Asset Prudence Fund (MAPF)api-349453187Оценок пока нет

- Ntflix StockResearch Report MorningStarДокумент13 страницNtflix StockResearch Report MorningStarPendi AgarwalОценок пока нет

- Winslow Drake SMAДокумент9 страницWinslow Drake SMATodd SullivanОценок пока нет

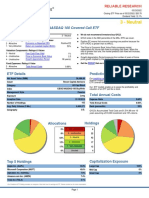

- 3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFДокумент3 страницы3 - Neutral: Global X Funds: Global X NASDAQ 100 Covered Call ETFphysicallen1791Оценок пока нет

- Key Takeaways: Terminologies With Their Scope & MeaningДокумент2 страницыKey Takeaways: Terminologies With Their Scope & MeaningSunanda MathuriaОценок пока нет

- S&P Morning Briefing 28 Nov 2018Документ7 страницS&P Morning Briefing 28 Nov 2018Abdullah18Оценок пока нет

- Thinking in Bets (Homage To Annie Duke) : Greenhaven Road CapitalДокумент9 страницThinking in Bets (Homage To Annie Duke) : Greenhaven Road Capitall chanОценок пока нет

- Secondary MarketДокумент13 страницSecondary Marketgpriyanshi1606Оценок пока нет

- Nirmal Bang 26th July 2018 IPO NoteДокумент13 страницNirmal Bang 26th July 2018 IPO NoteNiruОценок пока нет

- Financial Terms Glossary LMДокумент15 страницFinancial Terms Glossary LMphilipsdОценок пока нет

- Greenlight Capital 4Q20 Investor LetterДокумент7 страницGreenlight Capital 4Q20 Investor LetterGabriel AntonieОценок пока нет

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingОт EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingОценок пока нет

- Summary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoОт EverandSummary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoОценок пока нет

- EPD - Schwab PDFДокумент16 страницEPD - Schwab PDFJeff SturgeonОценок пока нет

- Schwab Ratios User GuideДокумент2 страницыSchwab Ratios User GuideJeff SturgeonОценок пока нет

- EPD - Argus PDFДокумент5 страницEPD - Argus PDFJeff SturgeonОценок пока нет

- HEP - Ratings PDFДокумент4 страницыHEP - Ratings PDFJeff SturgeonОценок пока нет

- MMP - RatingsДокумент4 страницыMMP - RatingsJeff SturgeonОценок пока нет

- Magellan Midstream Partners LP: Analyst's NotesДокумент4 страницыMagellan Midstream Partners LP: Analyst's NotesJeff SturgeonОценок пока нет

- MMP - RatingsДокумент4 страницыMMP - RatingsJeff SturgeonОценок пока нет

- HP - Argus PDFДокумент5 страницHP - Argus PDFJeff SturgeonОценок пока нет

- MDP - SchwabДокумент5 страницMDP - SchwabJeff SturgeonОценок пока нет

- OKE - SchwabДокумент5 страницOKE - SchwabJeff SturgeonОценок пока нет

- MMP - SchwabДокумент17 страницMMP - SchwabJeff SturgeonОценок пока нет

- OHI - RatingsДокумент4 страницыOHI - RatingsJeff SturgeonОценок пока нет

- OKE - ArgusДокумент5 страницOKE - ArgusJeff SturgeonОценок пока нет

- MDP - RatingsДокумент4 страницыMDP - RatingsJeff SturgeonОценок пока нет

- High DividendsДокумент2 страницыHigh DividendsJeff SturgeonОценок пока нет

- Growth - DividendДокумент6 страницGrowth - DividendJeff SturgeonОценок пока нет

- Aztec Gold Dry RubДокумент9 страницAztec Gold Dry RubJeff SturgeonОценок пока нет

- OKE - RatingsДокумент4 страницыOKE - RatingsJeff SturgeonОценок пока нет

- Oxford Income Letter 0420 Sal93Документ12 страницOxford Income Letter 0420 Sal93Jeff SturgeonОценок пока нет

- The All American DogДокумент4 страницыThe All American DogJeff SturgeonОценок пока нет

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFДокумент16 страницBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonОценок пока нет

- Baseball Team StatsДокумент6 страницBaseball Team StatsJeff SturgeonОценок пока нет

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFДокумент16 страницBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonОценок пока нет

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFДокумент16 страницBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonОценок пока нет

- Leibold RF Weaver 3B Collins 2B Jackson LF Felsch CF Gandil 1B Risberg SS Schalk C PДокумент12 страницLeibold RF Weaver 3B Collins 2B Jackson LF Felsch CF Gandil 1B Risberg SS Schalk C PJeff SturgeonОценок пока нет

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFДокумент16 страницBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonОценок пока нет

- Slagle CF Sheckard LF Schulte RF Chance 1B Steinfeldt 3B Tinker SS Evers 2B Kling C PДокумент12 страницSlagle CF Sheckard LF Schulte RF Chance 1B Steinfeldt 3B Tinker SS Evers 2B Kling C PJeff SturgeonОценок пока нет

- Byrne 3B Leach CF Clarke LF Wagner SS Miller 2B Abstein 1B Wilson RF Gibson C PДокумент12 страницByrne 3B Leach CF Clarke LF Wagner SS Miller 2B Abstein 1B Wilson RF Gibson C PJeff SturgeonОценок пока нет

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFДокумент16 страницBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonОценок пока нет

- Browne RF Donlin CF Mcgann 1B Mertes LF Dahlen Ss Devlin 3B Gilbert 2B Bresnahan C PДокумент12 страницBrowne RF Donlin CF Mcgann 1B Mertes LF Dahlen Ss Devlin 3B Gilbert 2B Bresnahan C PJeff SturgeonОценок пока нет

- Forecast Error (Control Chart)Документ2 страницыForecast Error (Control Chart)Jane OngОценок пока нет

- Contracts ChecklistДокумент3 страницыContracts ChecklistSteve WatmoreОценок пока нет

- 2022BusinessManagement ReportДокумент17 страниц2022BusinessManagement ReportkianaОценок пока нет

- Measures-English, Metric, and Equivalents PDFДокумент1 страницаMeasures-English, Metric, and Equivalents PDFluz adolfoОценок пока нет

- JURDING (Corticosteroids Therapy in Combination With Antibiotics For Erysipelas)Документ21 страницаJURDING (Corticosteroids Therapy in Combination With Antibiotics For Erysipelas)Alif Putri YustikaОценок пока нет

- A Tool For The Assessment of Project Com PDFДокумент9 страницA Tool For The Assessment of Project Com PDFgskodikara2000Оценок пока нет

- Bossa Nova Book PDFДокумент5 страницBossa Nova Book PDFschmimiОценок пока нет

- Olinger v. The Church of Jesus Christ of Latter Day Saints Et Al - Document No. 1Документ4 страницыOlinger v. The Church of Jesus Christ of Latter Day Saints Et Al - Document No. 1Justia.comОценок пока нет

- Ogayon Vs PeopleДокумент7 страницOgayon Vs PeopleKate CalansinginОценок пока нет

- CHAPTER 4 (B)Документ6 страницCHAPTER 4 (B)Jon Lester De VeyraОценок пока нет

- Ylarde vs. Aquino, GR 33722 (DIGEST)Документ1 страницаYlarde vs. Aquino, GR 33722 (DIGEST)Lourdes Loren Cruz67% (3)

- Commercial CrimesДокумент3 страницыCommercial CrimesHo Wen HuiОценок пока нет

- Scribe FormДокумент2 страницыScribe FormsiddharthgamreОценок пока нет

- Water On Mars PDFДокумент35 страницWater On Mars PDFAlonso GarcíaОценок пока нет

- Unsung Ancient African Indigenous Heroines and HerosДокумент27 страницUnsung Ancient African Indigenous Heroines and Herosmsipaa30Оценок пока нет

- Context: Lesson Author Date of DemonstrationДокумент4 страницыContext: Lesson Author Date of DemonstrationAR ManОценок пока нет

- J of Cosmetic Dermatology - 2019 - Zhang - A Cream of Herbal Mixture To Improve MelasmaДокумент8 страницJ of Cosmetic Dermatology - 2019 - Zhang - A Cream of Herbal Mixture To Improve Melasmaemily emiОценок пока нет

- Filipino HousesДокумент4 страницыFilipino HousesjackОценок пока нет

- Quarter 2-Module 7 Social and Political Stratification: Department of Education Republic of The PhilippinesДокумент21 страницаQuarter 2-Module 7 Social and Political Stratification: Department of Education Republic of The Philippinestricia100% (5)

- Fascinating Numbers: Some Numbers of 3 Digits or More Exhibit A Very Interesting PropertyДокумент2 страницыFascinating Numbers: Some Numbers of 3 Digits or More Exhibit A Very Interesting PropertyAnonymous JGW0KRl6Оценок пока нет

- Public BudgetingДокумент15 страницPublic BudgetingTom Wan Der100% (4)

- Welcome To The Jfrog Artifactory User Guide!Документ3 страницыWelcome To The Jfrog Artifactory User Guide!RaviОценок пока нет

- Internship Report On Effects of Promotion System On Employee Job Satisfaction of Janata Bank Ltd.Документ57 страницInternship Report On Effects of Promotion System On Employee Job Satisfaction of Janata Bank Ltd.Tareq Alam100% (1)

- Inside Out or Outside inДокумент6 страницInside Out or Outside inΧΡΗΣΤΟΣ ΠΑΠΑΔΟΠΟΥΛΟΣОценок пока нет

- E 18 - 02 - Rte4ltay PDFДокумент16 страницE 18 - 02 - Rte4ltay PDFvinoth kumar SanthanamОценок пока нет

- Clothing, Personality and Impressions PDFДокумент11 страницClothing, Personality and Impressions PDFAhmad RaoОценок пока нет

- AIDA Deconstruction of Surf Excel AdДокумент6 страницAIDA Deconstruction of Surf Excel AdRoop50% (2)

- Ministry of Truth Big Brother Watch 290123Документ106 страницMinistry of Truth Big Brother Watch 290123Valentin ChirilaОценок пока нет

- Sale Deed Document Rajyalakshmi, 2222222Документ3 страницыSale Deed Document Rajyalakshmi, 2222222Madhav Reddy100% (2)

- Analysing Worship in The Pentateuch and Its ApplicationДокумент12 страницAnalysing Worship in The Pentateuch and Its ApplicationDaniel Solomon100% (1)