Вам также может понравиться

- I Have Used These Techniques and Improved My Score by 100 Pts in Less Than 1 YearДокумент9 страницI Have Used These Techniques and Improved My Score by 100 Pts in Less Than 1 YearKNOWLEDGE SOURCE96% (51)

- Student Activity Packet SC-6.1Документ3 страницыStudent Activity Packet SC-6.1Chassidy AberdeenОценок пока нет

- United India Insurance Company Limited: WWW - Uiic.co - inДокумент2 страницыUnited India Insurance Company Limited: WWW - Uiic.co - inGulshan Datta0% (1)

- COMPLETED Book 7 BSBFIA303 - Accounts Payable and ReceivableДокумент10 страницCOMPLETED Book 7 BSBFIA303 - Accounts Payable and Receivabletanika0% (2)

- Something Went Sour at ParmalatДокумент1 страницаSomething Went Sour at Parmalatenergizerabby100% (1)

- Bank Letter For Fixed Deposit - SampleДокумент1 страницаBank Letter For Fixed Deposit - Sampletvaprasad75% (4)

- Tax Preparation for Beginners: The Easy Way to Prepare, Reduce, and File Taxes YourselfОт EverandTax Preparation for Beginners: The Easy Way to Prepare, Reduce, and File Taxes YourselfРейтинг: 5 из 5 звезд5/5 (1)

- IRS 3949-A American Bankers AssociationДокумент2 страницыIRS 3949-A American Bankers Associationrodclassteam100% (4)

- Opportunity KnocksДокумент1 страницаOpportunity KnocksOntario Trillium Foundation / Fondation Trillium de l'Ontario100% (1)

- 2021 Tax Tips-Karla Dennis EbookДокумент13 страниц2021 Tax Tips-Karla Dennis EbookShantrece MarshallОценок пока нет

- Compass Insights July 2008Документ2 страницыCompass Insights July 2008compassfinancial100% (2)

- PDF - How To Start A NonprofitДокумент4 страницыPDF - How To Start A NonprofitLyrics World РусскийОценок пока нет

- Repair Your CreditДокумент13 страницRepair Your Creditchris mcwilliamsОценок пока нет

- Challenges Faced by The Non - Profit OrganizationДокумент2 страницыChallenges Faced by The Non - Profit OrganizationTrupti DeoreОценок пока нет

- Audit Program For 4-H OrganizationsДокумент3 страницыAudit Program For 4-H OrganizationsZain FarozdaqОценок пока нет

- 10 Missteps With Tax-Sheltered AccountsДокумент10 страниц10 Missteps With Tax-Sheltered Accountsambasyapare1Оценок пока нет

- 2018 Guide For AUP For Local GovsДокумент28 страниц2018 Guide For AUP For Local GovsRahul BhanОценок пока нет

- Quick Administrative Process Plus Court Enforcement ProcessДокумент53 страницыQuick Administrative Process Plus Court Enforcement ProcessBrad100% (1)

- Letter From Congress Regarding OPM Retirement BacklogДокумент3 страницыLetter From Congress Regarding OPM Retirement BacklogFedSmith Inc.Оценок пока нет

- Professional Ethics - Case StudiesДокумент11 страницProfessional Ethics - Case StudiesOnyeuka CharlestonОценок пока нет

- ACOSS To Senator Scott - OverPayments - 12-06-2023-FINALwithSignatureREVДокумент3 страницыACOSS To Senator Scott - OverPayments - 12-06-2023-FINALwithSignatureREVWZZM NewsОценок пока нет

- Legal Resources - EFT (Electronic - Funds - Transfer) ExplainedДокумент9 страницLegal Resources - EFT (Electronic - Funds - Transfer) ExplainedBrad100% (4)

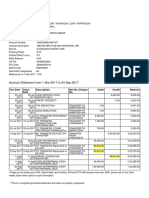

- Equity Bank Statement SampleДокумент8 страницEquity Bank Statement SampleNiyonagize HiraireОценок пока нет

- LLC 12 112021Документ8 страницLLC 12 112021robbie992371Оценок пока нет

- QuickAdminProcessDocs 082210Документ44 страницыQuickAdminProcessDocs 082210whiteb76100% (1)

- Statement of Affairs Instructions and Form1may2016Документ2 страницыStatement of Affairs Instructions and Form1may2016Hang TuahОценок пока нет

- UHY Not-For-Profit Newsletter - March 2012Документ2 страницыUHY Not-For-Profit Newsletter - March 2012UHYColumbiaMDОценок пока нет

- Fbar ThesisДокумент4 страницыFbar Thesisf1t1febysil2100% (2)

- CHP 1 and 2 BbaДокумент73 страницыCHP 1 and 2 BbaBarkkha MakhijaОценок пока нет

- New Business Owner RoadmapДокумент10 страницNew Business Owner RoadmapMwauraОценок пока нет

- UHY Not-for-Profit Newsletter - August 2011Документ2 страницыUHY Not-for-Profit Newsletter - August 2011UHYColumbiaMDОценок пока нет

- LLC 12ncДокумент3 страницыLLC 12ncAli AldosОценок пока нет

- How Can A Foreigner Open A Company in The UNITED STATESДокумент4 страницыHow Can A Foreigner Open A Company in The UNITED STATESGenevieveОценок пока нет

- Reviewing Accounts - A Rough GuideДокумент6 страницReviewing Accounts - A Rough GuideImprovingSupportОценок пока нет

- Contacting Your LegislatorsДокумент1 страницаContacting Your Legislatorstravis neutzmanОценок пока нет

- Cashology Reports Clean Credit in A Month ! Start Living Without The Anxiety of Crippling DebtДокумент10 страницCashology Reports Clean Credit in A Month ! Start Living Without The Anxiety of Crippling DebtCashology ReportsОценок пока нет

- 5 Different Phases of Making An EnterpriseДокумент6 страниц5 Different Phases of Making An EnterpriseLianna RodriguezОценок пока нет

- Questions Chapter 2Документ4 страницыQuestions Chapter 2Minh Thư Phạm HuỳnhОценок пока нет

- Making Money From The MeltdownДокумент52 страницыMaking Money From The Meltdownrnj1230100% (1)

- You As A Creditor: FINANCIAL ACCOUNTING (Williams Et Al.) Suggested Answers For "Your Turn" CasesДокумент10 страницYou As A Creditor: FINANCIAL ACCOUNTING (Williams Et Al.) Suggested Answers For "Your Turn" CasesTamhaFatimaОценок пока нет

- Handling Disputes With The Canada Revenue AgencyДокумент6 страницHandling Disputes With The Canada Revenue AgencyRay BrooksОценок пока нет

- Gage College School of Graduate Studies Mba Program: FMA - Ethical Mini Case 01 - Assigned To Group 1 StudentsДокумент12 страницGage College School of Graduate Studies Mba Program: FMA - Ethical Mini Case 01 - Assigned To Group 1 StudentsEyasu JaworОценок пока нет

- Instruction Package - OSBDC-2018-06 PDFДокумент8 страницInstruction Package - OSBDC-2018-06 PDFHelen OlindoОценок пока нет

- De Leon - Interm1 - Online Discussion Prompt - Bfac02Документ2 страницыDe Leon - Interm1 - Online Discussion Prompt - Bfac02Earl De LeonОценок пока нет

- Amazing Facts About Big 4 Accounting FirmsДокумент20 страницAmazing Facts About Big 4 Accounting FirmssandyskadamОценок пока нет

- 2016 - 2017 Estate Planning Guide for Ontarians - “Completing the Puzzle”От Everand2016 - 2017 Estate Planning Guide for Ontarians - “Completing the Puzzle”Оценок пока нет

- Principles of Taxation For Business and Investment Planning 2016 19th Edition Jones Solutions Manual 1Документ36 страницPrinciples of Taxation For Business and Investment Planning 2016 19th Edition Jones Solutions Manual 1shannonwaltersqwdifntckm100% (27)

- Crazy EddieДокумент5 страницCrazy EddieAmos N. SandoОценок пока нет

- Research Paper Government ShutdownДокумент6 страницResearch Paper Government Shutdowngw10ka6s100% (1)

- Central Banker - Winter 2004Документ6 страницCentral Banker - Winter 2004Federal Reserve Bank of St. LouisОценок пока нет

- Attention Needed: Mismanagement at The Sba - The Gao FindingsДокумент40 страницAttention Needed: Mismanagement at The Sba - The Gao FindingsScribd Government DocsОценок пока нет

- Research Paper On Revenue CollectionДокумент8 страницResearch Paper On Revenue Collectionfyrqkxfq100% (1)

- Starting A Non Profit in 5 StepsДокумент2 страницыStarting A Non Profit in 5 StepsMerlyn BrownОценок пока нет

- Entrepreneurship Q2 M7Документ17 страницEntrepreneurship Q2 M7Primosebastian TarrobagoОценок пока нет

- Financial & Managerial Acct-Group Ass-01Документ12 страницFinancial & Managerial Acct-Group Ass-01Noah GunnОценок пока нет

- EligibilityResultsNotice 5Документ16 страницEligibilityResultsNotice 5ymtfyjywzfОценок пока нет

- Key Factor For Granting LoansДокумент1 страницаKey Factor For Granting LoanstoushigaОценок пока нет

- Amazing Facts About Big 4 Accounting FirmsДокумент20 страницAmazing Facts About Big 4 Accounting FirmsMoralVolcanoОценок пока нет

- 501 C 3Документ26 страниц501 C 3api-370055350% (2)

- ERISA Insider - April 2015Документ2 страницыERISA Insider - April 2015UHYColumbiaMDОценок пока нет

- UHY Government Contractor Insider - February 2015Документ2 страницыUHY Government Contractor Insider - February 2015UHYColumbiaMDОценок пока нет

- Government Contractor Insider - April 2015Документ2 страницыGovernment Contractor Insider - April 2015UHYColumbiaMDОценок пока нет

- Nonprofit Insider - May 2015Документ2 страницыNonprofit Insider - May 2015UHYColumbiaMDОценок пока нет

- UHY Technology Insider - February 2015Документ2 страницыUHY Technology Insider - February 2015UHYColumbiaMDОценок пока нет

- UHY Nonprofit Insider - December 2014Документ2 страницыUHY Nonprofit Insider - December 2014UHYColumbiaMDОценок пока нет

- Nonprofit Insider - March 2015Документ2 страницыNonprofit Insider - March 2015UHYColumbiaMDОценок пока нет

- UHY ERISA Insider - February 2015Документ2 страницыUHY ERISA Insider - February 2015UHYColumbiaMDОценок пока нет

- UHY Nonprofit Insider - April 2014Документ2 страницыUHY Nonprofit Insider - April 2014UHYColumbiaMDОценок пока нет

- UHY Nonprofit Insider - June 2014Документ2 страницыUHY Nonprofit Insider - June 2014UHYColumbiaMDОценок пока нет

- UHY Nonprofit Insider - August 2014Документ2 страницыUHY Nonprofit Insider - August 2014UHYColumbiaMDОценок пока нет

- UHY Nonprofit Insider - October 2014Документ2 страницыUHY Nonprofit Insider - October 2014UHYColumbiaMDОценок пока нет

- UHY NonProfit Insider December 2013Документ2 страницыUHY NonProfit Insider December 2013UHYColumbiaMDОценок пока нет

- UHY NonProfit Insider February 2014Документ2 страницыUHY NonProfit Insider February 2014UHYColumbiaMDОценок пока нет

- UHY Government Contractor Insider Feb 2014Документ2 страницыUHY Government Contractor Insider Feb 2014UHYColumbiaMDОценок пока нет

- UHY NonProfit Insider February 2014Документ2 страницыUHY NonProfit Insider February 2014UHYColumbiaMDОценок пока нет

- UHY Government Contractor Insider - December, 2013Документ2 страницыUHY Government Contractor Insider - December, 2013UHYColumbiaMDОценок пока нет

- UHY Government Contractor Insider - April 2014Документ2 страницыUHY Government Contractor Insider - April 2014UHYColumbiaMDОценок пока нет

- UHY Government Contractor Insider Feb 2014Документ2 страницыUHY Government Contractor Insider Feb 2014UHYColumbiaMDОценок пока нет

- UHY Technology Insider - April 2014Документ2 страницыUHY Technology Insider - April 2014UHYColumbiaMDОценок пока нет

- Nonprofit Insider: What Is Your Form 990 Telling The IRS?Документ2 страницыNonprofit Insider: What Is Your Form 990 Telling The IRS?UHYColumbiaMDОценок пока нет

- UHY NonProfit Insider December 2013Документ2 страницыUHY NonProfit Insider December 2013UHYColumbiaMDОценок пока нет

- UHY Not-for-Profit Newsletter - August 2013Документ2 страницыUHY Not-for-Profit Newsletter - August 2013UHYColumbiaMDОценок пока нет

- UHY Government Contractor Newsletter - May 2013Документ4 страницыUHY Government Contractor Newsletter - May 2013UHYColumbiaMDОценок пока нет

- UHY Not-for-Profit Newsletter - January 2013Документ2 страницыUHY Not-for-Profit Newsletter - January 2013UHYColumbiaMDОценок пока нет

- UHY Technology Newsletter - July 2013Документ4 страницыUHY Technology Newsletter - July 2013UHYColumbiaMDОценок пока нет

- UHY Not-for-Profit Newsletter - February 2013Документ2 страницыUHY Not-for-Profit Newsletter - February 2013UHYColumbiaMDОценок пока нет

- UHY Government Contractor Newsletter - February 2013Документ2 страницыUHY Government Contractor Newsletter - February 2013UHYColumbiaMDОценок пока нет

- UHY Not-For-Profit Newsletter - August 2012Документ2 страницыUHY Not-For-Profit Newsletter - August 2012UHYColumbiaMDОценок пока нет

- Insider: Plan Sponsors, Are You Ready For The New Regulations?Документ2 страницыInsider: Plan Sponsors, Are You Ready For The New Regulations?UHYColumbiaMDОценок пока нет

- Acctg 111 - TPДокумент4 страницыAcctg 111 - TPElizabeth Espinosa ManilagОценок пока нет

- LoanДокумент2 страницыLoanpratheeshОценок пока нет

- Applied Auditing: 3/F F. Facundo Hall, B & E Bldg. Matina, Davao City Philippines Phone No.: (082) 305-0645Документ7 страницApplied Auditing: 3/F F. Facundo Hall, B & E Bldg. Matina, Davao City Philippines Phone No.: (082) 305-0645Bryan PiañarОценок пока нет

- Accounting BasicsДокумент144 страницыAccounting BasicsSabyasachi Srimany100% (1)

- Problems Identified by The Narasimham CommitteeДокумент3 страницыProblems Identified by The Narasimham Committeeshaikhaamir21Оценок пока нет

- Nacif V White-SorensonДокумент46 страницNacif V White-SorensonDinSFLAОценок пока нет

- En 20120404Документ24 страницыEn 20120404Hai Hoang ThanhОценок пока нет

- Whole Life InsuranceДокумент4 страницыWhole Life Insuranceprasanthgeni22Оценок пока нет

- Intp LK TW Iv 2019Документ141 страницаIntp LK TW Iv 2019Davila RAОценок пока нет

- Export Import Management UTS SummaryДокумент9 страницExport Import Management UTS SummaryRajendra Khalil AfifОценок пока нет

- TcsДокумент21 страницаTcsSyedadam HasnainОценок пока нет

- Last 5 Months Expected Banking Questions From Current AffairsДокумент9 страницLast 5 Months Expected Banking Questions From Current AffairsAnuj KumarОценок пока нет

- "Moment of Truth" For Canada's Banks - Victor Dodig Interview Part 2Документ1 страница"Moment of Truth" For Canada's Banks - Victor Dodig Interview Part 2GenieОценок пока нет

- Paper 16Документ71 страницаPaper 16pkaul1Оценок пока нет

- SLC - Gndu.ac - in StudentArea SLC TutitionFeeBankSlip - AspxДокумент1 страницаSLC - Gndu.ac - in StudentArea SLC TutitionFeeBankSlip - AspxGurnoor SinghОценок пока нет

- Interim Order in The Matter of Mr. Anirudh SethiДокумент14 страницInterim Order in The Matter of Mr. Anirudh SethiShyam SunderОценок пока нет

- Mba Employment Statistics PDFДокумент52 страницыMba Employment Statistics PDFDwarakanath MuraliОценок пока нет

- I. What Is Equitable Mortgage?Документ6 страницI. What Is Equitable Mortgage?Jhon Allain HisolaОценок пока нет

- Bus Law Mcqs 2016Документ6 страницBus Law Mcqs 2016Anonymous 03JIPKRkОценок пока нет

- Global & Regional League Tables 2021: Financial AdvisorsДокумент39 страницGlobal & Regional League Tables 2021: Financial AdvisorsLiam KimОценок пока нет

- First Women Bank Ltd. (FWBL) : Unique Credit PoliciesДокумент2 страницыFirst Women Bank Ltd. (FWBL) : Unique Credit PoliciesMIan MuzamilОценок пока нет

- Unit-1/ Introduction To Housing and Housing Issues - Indian Context /10 HoursДокумент32 страницыUnit-1/ Introduction To Housing and Housing Issues - Indian Context /10 HoursPriyankaОценок пока нет

- Sonali Bank Loan CalculationДокумент7 страницSonali Bank Loan CalculationEngineering EntertainmentОценок пока нет

- Elizabeth Wangui Wangoo Theory For InclusionДокумент81 страницаElizabeth Wangui Wangoo Theory For Inclusionliemuel100% (1)

- Problem 1Документ14 страницProblem 1Jerry DiazОценок пока нет

- Incoterms - ExworkДокумент16 страницIncoterms - ExworkAnonymous duzV27Mx3Оценок пока нет

- Suffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Документ29 страницSuffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Foreclosure FraudОценок пока нет

- Central BankingДокумент29 страницCentral BankingMarcy ViernesGalasinao MaguigadCabacunganОценок пока нет