Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- New Civil CodeДокумент212 страницNew Civil Codeautumn moon100% (1)

- Solution Manual For Munson Young and Okiishis Fundamentals of Fluid Mechanics 8th by GerhartДокумент9 страницSolution Manual For Munson Young and Okiishis Fundamentals of Fluid Mechanics 8th by GerhartEunice Scarpello100% (36)

- 2G N 16Документ43 страницы2G N 16Fernando Mondragon100% (1)

- Sample Letter For Damages To PropertyДокумент14 страницSample Letter For Damages To PropertyQuinton Nick100% (1)

- Cocoa ReportДокумент78 страницCocoa Reportmyjoyonline.comОценок пока нет

- The Sorrowful MysteriesДокумент6 страницThe Sorrowful MysteriesSJ SimonОценок пока нет

- GoldenДокумент1 страницаGoldenSJ SimonОценок пока нет

- Healthy Meal ScheduleДокумент9 страницHealthy Meal ScheduleSJ SimonОценок пока нет

- Module III-A Moral LawДокумент17 страницModule III-A Moral LawSJ SimonОценок пока нет

- Instructions:: Candor Cash Flow SolutionДокумент1 страницаInstructions:: Candor Cash Flow SolutionPirvuОценок пока нет

- (ACYFAR2) Toribio Critique Paper K36.editedДокумент12 страниц(ACYFAR2) Toribio Critique Paper K36.editedHannah Jane ToribioОценок пока нет

- Group3 GroupResearchAssignmentДокумент23 страницыGroup3 GroupResearchAssignmentGajulin, April JoyОценок пока нет

- GAP Model On Mac Donald's: Presented by Group No: 3Документ20 страницGAP Model On Mac Donald's: Presented by Group No: 3Dipesh KotechaОценок пока нет

- Lesson 7B Organization StructureДокумент9 страницLesson 7B Organization StructureChristine LogdatОценок пока нет

- G MX Ez Qy Uk RFBJ Qy Ej NДокумент1 страницаG MX Ez Qy Uk RFBJ Qy Ej NMahmudur Rahman SunnyОценок пока нет

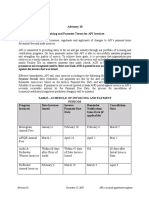

- API Advisory 10 Invoicing and Payment Terms English Translation 20191220Документ2 страницыAPI Advisory 10 Invoicing and Payment Terms English Translation 20191220Yusri WyeuserieyОценок пока нет

- Case Study of Central Business DistrictДокумент16 страницCase Study of Central Business DistrictMilena Mari FamilaraОценок пока нет

- Cost Volume Profit Analysis Cost Accounting 2022 P1Документ6 страницCost Volume Profit Analysis Cost Accounting 2022 P1jay-an DahunogОценок пока нет

- Dynamic Systems Development Method, The StandardДокумент18 страницDynamic Systems Development Method, The StandardaiaoeОценок пока нет

- Do American Consumers Need A Financial Protection Agency?: E: 2.4 Kevin MeskillДокумент6 страницDo American Consumers Need A Financial Protection Agency?: E: 2.4 Kevin MeskillKevinОценок пока нет

- Job Application Letter FormatДокумент7 страницJob Application Letter Formatbcreq2m5100% (2)

- Beauty Salon Company Profile SampleДокумент9 страницBeauty Salon Company Profile SampleSanjay TulsankarОценок пока нет

- ExpandedAppendixChapter12 PDFДокумент4 страницыExpandedAppendixChapter12 PDFfunam2Оценок пока нет

- Reading 20 Discounted Dividend ValuationДокумент55 страницReading 20 Discounted Dividend Valuationdhanh.bdn.hsv.neuОценок пока нет

- AssignmentДокумент21 страницаAssignmentTabeer HashmiОценок пока нет

- The Philippine IT BPM Industry Roadmap Executive Summary CompressedДокумент55 страницThe Philippine IT BPM Industry Roadmap Executive Summary Compressedpavanbagade27Оценок пока нет

- Inventory ValuationДокумент4 страницыInventory ValuationMary AmoОценок пока нет

- Kantar MediaДокумент4 страницыKantar MediaAnjana JogyОценок пока нет

- ch14 Managerial AccountingДокумент36 страницch14 Managerial AccountingMОценок пока нет

- Personnel Planning and Recruiting: Gary DesslerДокумент34 страницыPersonnel Planning and Recruiting: Gary DesslerRohit ChaudharyОценок пока нет

- Silang2018 Audit Report PDFДокумент113 страницSilang2018 Audit Report PDFLomo LomoОценок пока нет

- Appraisal of Machinery and EquipmentДокумент3 страницыAppraisal of Machinery and EquipmentJen ManriqueОценок пока нет

- Indonesia Jakarta Rental Apartment Q1 2021Документ2 страницыIndonesia Jakarta Rental Apartment Q1 2021Grace SaragihОценок пока нет

- BC 5years Solved Question PaperДокумент25 страницBC 5years Solved Question PaperYashwanth KumarОценок пока нет

- Chapter 4 Process SelectionДокумент18 страницChapter 4 Process Selectionmohammed mohammedОценок пока нет