Вам также может понравиться

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОт EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОценок пока нет

- Tunisia Review PolicyДокумент13 страницTunisia Review PolicyAmna EhsanОценок пока нет

- ACCT 2211 Assignment 2Документ17 страницACCT 2211 Assignment 2Tannaz SОценок пока нет

- Accounting Adjusting EntriesДокумент6 страницAccounting Adjusting EntriescamilleОценок пока нет

- Assign 1& 2Документ8 страницAssign 1& 2AreebaОценок пока нет

- Assignment 1Документ19 страницAssignment 1Areeba100% (1)

- Adjusting EntriesДокумент38 страницAdjusting EntriesKae Abegail GarciaОценок пока нет

- Adjusting The AccountsДокумент17 страницAdjusting The AccountsDira SabillaОценок пока нет

- CH 3 HomeworkДокумент6 страницCH 3 HomeworkAxel OngОценок пока нет

- Sodapdf Converted 1Документ3 страницыSodapdf Converted 1jiregna gadisaОценок пока нет

- AHM13e - Chapter 01 - Key To EOC Problems and CasesДокумент14 страницAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Klausur WS2021-22-1Документ6 страницKlausur WS2021-22-1marynayarmak.stОценок пока нет

- April Joy CompanyДокумент1 страницаApril Joy CompanyQueen ValleОценок пока нет

- Group Assignment - Questions - RevisedДокумент6 страницGroup Assignment - Questions - Revised31231023949Оценок пока нет

- Kimmel, Weygandt, Kieso: Tools For Business Decision Making, 3rd EdДокумент50 страницKimmel, Weygandt, Kieso: Tools For Business Decision Making, 3rd Edujjval10Оценок пока нет

- Correct Response Answer ChoicesДокумент11 страницCorrect Response Answer ChoicesArjay Dela PenaОценок пока нет

- Accounting Exercises PDFДокумент7 страницAccounting Exercises PDFMoni TafechОценок пока нет

- 2016-12 ICMAB FL 001 PAC Year Question December 2016Документ3 страницы2016-12 ICMAB FL 001 PAC Year Question December 2016Mohammad ShahidОценок пока нет

- Adjustment of Financial StatementДокумент33 страницыAdjustment of Financial StatementAlish BaОценок пока нет

- Casos de Ajuste.Документ9 страницCasos de Ajuste.Alguien algunoОценок пока нет

- MerchandisingДокумент11 страницMerchandisingAIRA NHAIRE MECATE100% (1)

- Sha1 ACT 201 Final Exam-Fall 2021Документ4 страницыSha1 ACT 201 Final Exam-Fall 2021Ifaz Mohammed IslamОценок пока нет

- Accounting For ReceivablesДокумент4 страницыAccounting For ReceivablesMega Pop Locker50% (2)

- Accruals and Deferral Chapter 4 ExercisesДокумент6 страницAccruals and Deferral Chapter 4 ExercisesSiraj KabbaraОценок пока нет

- Case 2 Adjusting Entries F 18Документ6 страницCase 2 Adjusting Entries F 18rcbcsk csk0% (1)

- De Cuong Lich Su Dang Co To UyenДокумент91 страницаDe Cuong Lich Su Dang Co To UyenTrần HùngОценок пока нет

- Accounting Transaction Processing Chapter 3Документ73 страницыAccounting Transaction Processing Chapter 3Rupesh PolОценок пока нет

- ACT 2100 Worksheet IVДокумент7 страницACT 2100 Worksheet IVAshmini PershadОценок пока нет

- FSA ExercisesДокумент23 страницыFSA ExercisesBel NochuОценок пока нет

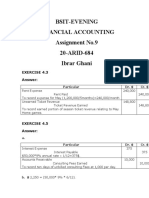

- Bsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar GhaniДокумент3 страницыBsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar Ghaniibrar ghani100% (1)

- Accounting Process With AnsДокумент6 страницAccounting Process With AnsMichael BongalontaОценок пока нет

- Accounting Process HandoutsДокумент6 страницAccounting Process HandoutsMichael BongalontaОценок пока нет

- Arab Final 90% Fall2021 (YS)Документ8 страницArab Final 90% Fall2021 (YS)ahmed abuzedОценок пока нет

- Tugas Akt Perusahaan DagangДокумент4 страницыTugas Akt Perusahaan DagangRizkita Sukma Gayanti0% (1)

- Lecture-6 Adjusted Trial BalanceДокумент22 страницыLecture-6 Adjusted Trial BalanceWajiha NadeemОценок пока нет

- ACCT 251 Practice Set 2021 - 1Документ28 страницACCT 251 Practice Set 2021 - 1Earl Justine FerrerОценок пока нет

- ACT301 (Final), Spring-21Документ4 страницыACT301 (Final), Spring-21Papon SarkerОценок пока нет

- Topic 4 - Adjusting Accounts and Preparing Financial StatementsДокумент18 страницTopic 4 - Adjusting Accounts and Preparing Financial Statementsapi-388504348100% (1)

- Unit 1 TestДокумент10 страницUnit 1 TestLoic Lim-YookОценок пока нет

- Practice ProblemsДокумент15 страницPractice ProblemsBringinthehypeОценок пока нет

- Course: Financial Accounting (5004)Документ4 страницыCourse: Financial Accounting (5004)ZeeshanОценок пока нет

- CH 02Документ4 страницыCH 02flrnciairnОценок пока нет

- Whatever - Ciclo ContableДокумент6 страницWhatever - Ciclo ContablemillionextupОценок пока нет

- Practice Exam - QuestionsДокумент5 страницPractice Exam - QuestionsHoàng Võ Như QuỳnhОценок пока нет

- Answers To Handout 1 Financial AccountingДокумент40 страницAnswers To Handout 1 Financial AccountingMohand ElbakryОценок пока нет

- (Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-MailДокумент3 страницы(Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-MailMichael BongalontaОценок пока нет

- Adjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingДокумент9 страницAdjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingHassan AliОценок пока нет

- E13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofДокумент4 страницыE13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofChupa HesОценок пока нет

- E3-5 (LO 3) Adjusting Entries: InstructionsДокумент6 страницE3-5 (LO 3) Adjusting Entries: InstructionsAntonios Fahed0% (1)

- CH 03Документ8 страницCH 03Rabie HarounОценок пока нет

- Diagnostic Quiz On Accounting 2Документ9 страницDiagnostic Quiz On Accounting 2Anne Ford67% (3)

- Liabilities Exercises SolutionsДокумент8 страницLiabilities Exercises Solutionsthanh subОценок пока нет

- Accounting ProcessДокумент3 страницыAccounting Processabernardino.forschoolОценок пока нет

- Orie 3150 HW1 Fa17Документ5 страницOrie 3150 HW1 Fa17Carl WeinfieldОценок пока нет

- Notes Adjusting EntriesДокумент14 страницNotes Adjusting EntriesGelesabeth Garcia100% (1)

- Excercise Sheet Lectures 1 and 2 Spring 2022Документ16 страницExcercise Sheet Lectures 1 and 2 Spring 2022Mohamed ZaitoonОценок пока нет

- Soal Akuntansi OSN Ekonomi Dan PembahasaДокумент6 страницSoal Akuntansi OSN Ekonomi Dan PembahasaQurrotul AyuniОценок пока нет

- Tan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMДокумент6 страницTan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMvanessaОценок пока нет

- Analyzing TransactionsДокумент8 страницAnalyzing TransactionsUgaas yare21Оценок пока нет

- Accountants Divide The Economic Life of A Business Into Reporting PeriodsДокумент36 страницAccountants Divide The Economic Life of A Business Into Reporting PeriodsCОценок пока нет

- Ministry of Finance - Government of PakistanДокумент16 страницMinistry of Finance - Government of Pakistanmuhammad nazirОценок пока нет

- Monthly Bulletin of Statistics - May, 2018Документ315 страницMonthly Bulletin of Statistics - May, 2018Anonymous f7wV1lQKRОценок пока нет

- The Marketing Research ProcessДокумент21 страницаThe Marketing Research ProcessSaurav RawatОценок пока нет

- Determinants of The Decision To Adopt Islamic Finance: Evidence From OmanДокумент21 страницаDeterminants of The Decision To Adopt Islamic Finance: Evidence From OmanAnonymous f7wV1lQKRОценок пока нет

- The Strategic Triangle (Bagan)Документ15 страницThe Strategic Triangle (Bagan)Monalia SakwatiОценок пока нет

- Ministry of Finance - Government of PakistanДокумент16 страницMinistry of Finance - Government of Pakistanmuhammad nazirОценок пока нет

- CAPM AssignmentДокумент12 страницCAPM AssignmentAnonymous f7wV1lQKRОценок пока нет

- This Crypto Still Has A Lot of Potential Even After A 50% Move in Just Three Days!Документ4 страницыThis Crypto Still Has A Lot of Potential Even After A 50% Move in Just Three Days!Anonymous f7wV1lQKRОценок пока нет

- Aysha Khan Babar: House#4, Street#1, Islampura, Mumtazabad. MultanДокумент2 страницыAysha Khan Babar: House#4, Street#1, Islampura, Mumtazabad. MultanAnonymous f7wV1lQKRОценок пока нет

- 5015Документ6 страниц5015Anonymous f7wV1lQKRОценок пока нет

- Lodovico SlidesCarnivalДокумент39 страницLodovico SlidesCarnivalShairel GesimОценок пока нет

- Sandys SlidesCarnivalДокумент40 страницSandys SlidesCarnivalEman KhanОценок пока нет

- Black and White Corporate Business Proposal PresentationДокумент1 страницаBlack and White Corporate Business Proposal PresentationAnonymous f7wV1lQKRОценок пока нет

- Multi-Level Governance and Local Government Reform in PakistanДокумент33 страницыMulti-Level Governance and Local Government Reform in PakistanRauf MangalОценок пока нет

- Year Cash Flow Present ValueДокумент2 страницыYear Cash Flow Present ValueAnonymous f7wV1lQKRОценок пока нет

- This Crypto Still Has A Lot of Potential Even After A 50% Move in Just Three Days!Документ4 страницыThis Crypto Still Has A Lot of Potential Even After A 50% Move in Just Three Days!Anonymous f7wV1lQKRОценок пока нет

- Determinants of The Decision To Adopt Islamic Finance: Evidence From OmanДокумент21 страницаDeterminants of The Decision To Adopt Islamic Finance: Evidence From OmanAnonymous f7wV1lQKRОценок пока нет

- Account StatementДокумент4 страницыAccount StatementAnonymous f7wV1lQKRОценок пока нет

- Summary of ArticlesДокумент6 страницSummary of ArticlesAnonymous f7wV1lQKRОценок пока нет

- Concepts of Strategic ManagementДокумент40 страницConcepts of Strategic ManagementMohamed ZakaryaОценок пока нет

- Mughal BeddingДокумент1 страницаMughal BeddingAnonymous f7wV1lQKRОценок пока нет

- Computing The Present Value: Discount Rate Year Cash Flow PVДокумент2 страницыComputing The Present Value: Discount Rate Year Cash Flow PVAnonymous f7wV1lQKRОценок пока нет

- With Different Cash FlowsДокумент2 страницыWith Different Cash FlowsAnonymous f7wV1lQKRОценок пока нет

- Questionnaire 1 Strongly Disagree While 7 Strongly AgreeДокумент4 страницыQuestionnaire 1 Strongly Disagree While 7 Strongly AgreeAnonymous f7wV1lQKRОценок пока нет

- LAB SSP-514 (M.phil-SSP-O3-F19)Документ6 страницLAB SSP-514 (M.phil-SSP-O3-F19)Anonymous f7wV1lQKRОценок пока нет

- Economertics LectureДокумент1 страницаEconomertics LectureAnonymous f7wV1lQKRОценок пока нет

- Name: Sajeel Khan Roll#:M.phil-SSP-03-F19 Class: M.phil SSP (Morning) Subject: Optical Properties of Solid Submitted TOДокумент8 страницName: Sajeel Khan Roll#:M.phil-SSP-03-F19 Class: M.phil SSP (Morning) Subject: Optical Properties of Solid Submitted TOAnonymous f7wV1lQKRОценок пока нет

- SN Description Rs. SN Description Rs. SN Description Rs. SN Description Rs. SN Description RsДокумент1 страницаSN Description Rs. SN Description Rs. SN Description Rs. SN Description Rs. SN Description RsAnonymous f7wV1lQKRОценок пока нет

- Brazil - Return China - Return India - Return Russia - ReturnДокумент1 страницаBrazil - Return China - Return India - Return Russia - ReturnAnonymous f7wV1lQKRОценок пока нет

- 7-Global Capital MarketsДокумент8 страниц7-Global Capital MarketsAnonymous f7wV1lQKRОценок пока нет

- South Africa Income Tax - Exemptions PBOДокумент8 страницSouth Africa Income Tax - Exemptions PBOmusvibaОценок пока нет

- AnswerДокумент4 страницыAnswerZati TyОценок пока нет

- Leases Part IIДокумент21 страницаLeases Part IICarl Adrian ValdezОценок пока нет

- Aviation Management Page - 1Документ12 страницAviation Management Page - 1YamОценок пока нет

- ITC Working CapitalДокумент72 страницыITC Working Capitaltulasinad12356% (9)

- NCAA Financial Report FY2019-Coastal CarolinaДокумент79 страницNCAA Financial Report FY2019-Coastal CarolinaMatt BrownОценок пока нет

- Chilime Hydropower ProjectДокумент24 страницыChilime Hydropower ProjectChaudhari Awadhesh67% (3)

- Jet Airways Case StudyДокумент7 страницJet Airways Case StudySachin KinareОценок пока нет

- LGU Budget CycleДокумент3 страницыLGU Budget CycleDelfinОценок пока нет

- Personal Budget - WikipediaДокумент6 страницPersonal Budget - WikipediaRameenaОценок пока нет

- Capital Budgeting 2Документ4 страницыCapital Budgeting 2rebecabeczОценок пока нет

- Guide Notes On Local Government TaxationДокумент27 страницGuide Notes On Local Government TaxationNayadОценок пока нет

- Teachers Welfare and Privileges - Docx Jessa VillareteДокумент19 страницTeachers Welfare and Privileges - Docx Jessa VillareteNikka Jean Duero Lachica0% (1)

- Business Organizations 631 Assignment 14 Watson 6830Документ3 страницыBusiness Organizations 631 Assignment 14 Watson 6830wootenr2002100% (1)

- Yousaf Weaving Mills LTD - 2003: Balance Sheet As at September 30, 2003Документ8 страницYousaf Weaving Mills LTD - 2003: Balance Sheet As at September 30, 2003Anonymous pCZJ4KhОценок пока нет

- 3 Analysis of Foreign Financial StatementsДокумент32 страницы3 Analysis of Foreign Financial StatementsMeselech Girma100% (1)

- Session 10 Chapter 10 Making Capital InvestmentDecisionДокумент35 страницSession 10 Chapter 10 Making Capital InvestmentDecisionLili YaniОценок пока нет

- CBN Exchange Control ManualДокумент133 страницыCBN Exchange Control ManualAhmad Invaluable AdenijiОценок пока нет

- Mass HousingДокумент46 страницMass HousingSanjeev BumbОценок пока нет

- Goverment Accounting AllotmentsДокумент20 страницGoverment Accounting AllotmentsKaith BorjaskyОценок пока нет

- CamlinДокумент48 страницCamlinJugal ShahОценок пока нет

- Fin Man - Module 3Документ38 страницFin Man - Module 3Francine PrietoОценок пока нет

- Tata & Corus: Presented By:-Ankur Keshari Ashish Lal Priyanka Jain Ritu Gautam Presented To: - Ms. Parul NagarДокумент25 страницTata & Corus: Presented By:-Ankur Keshari Ashish Lal Priyanka Jain Ritu Gautam Presented To: - Ms. Parul Nagarnikzz_jainОценок пока нет

- Strategic Cost - CVP Analysis ReviewerДокумент2 страницыStrategic Cost - CVP Analysis ReviewerChristine AltamarinoОценок пока нет

- Lecture Notes On Quasi-ReorganizationДокумент2 страницыLecture Notes On Quasi-ReorganizationalyssaОценок пока нет

- TESCO Financial AnalysisДокумент18 страницTESCO Financial AnalysisFadekemi Fdk100% (1)

- 2016 SALN Form - JudithdocДокумент2 страницы2016 SALN Form - JudithdocNDAP DavaoОценок пока нет

- UBL Internship FinlllДокумент102 страницыUBL Internship FinlllAbdul JabbarОценок пока нет

- Action Aid International Staff ManualДокумент138 страницAction Aid International Staff Manualejazahmad5100% (1)

- Solution To Problems - Chapter 9Документ25 страницSolution To Problems - Chapter 9GFGSHSОценок пока нет