Вам также может понравиться

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)От EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Оценок пока нет

- ACCA F3 Jan 2014 Examiner ReportДокумент4 страницыACCA F3 Jan 2014 Examiner Reportolofamojo2Оценок пока нет

- Barings Bank and Nick LeesonДокумент76 страницBarings Bank and Nick LeesonTri Ratna PamikatsihОценок пока нет

- CR Pocket NoteДокумент166 страницCR Pocket NoteLaffin Ebi LaffinОценок пока нет

- Traders World 56Документ116 страницTraders World 56Massimo RaffaeleОценок пока нет

- Brown Marine Supply CompanyДокумент21 страницаBrown Marine Supply CompanyMuiz HassanОценок пока нет

- Equity Valuation: Models from Leading Investment BanksОт EverandEquity Valuation: Models from Leading Investment BanksJan ViebigОценок пока нет

- Reoprt On "Portfolio Management Services" by Sharekhan Stock Broking LimitedДокумент111 страницReoprt On "Portfolio Management Services" by Sharekhan Stock Broking LimitedAshutosh Rathod91% (22)

- (CB MODULE) Module 3 - Problem 3.1 To 3.20 Answer Keys (Pages 156 To 167)Документ29 страниц(CB MODULE) Module 3 - Problem 3.1 To 3.20 Answer Keys (Pages 156 To 167)Grace Alipoyo Fortuito-tanОценок пока нет

- Capital Reduction 2Документ6 страницCapital Reduction 2SANJIB SHARMAОценок пока нет

- Sums On Cash Flow StatementДокумент5 страницSums On Cash Flow StatementAstha ParmanandkaОценок пока нет

- Adobe Scan Jan 30, 2023Документ6 страницAdobe Scan Jan 30, 2023Karan RajakОценок пока нет

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Документ2 страницыFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalОценок пока нет

- Balance Sheet CompanyДокумент16 страницBalance Sheet CompanyNidhi ShahОценок пока нет

- PART-B Analysis Test YtДокумент8 страницPART-B Analysis Test YtRiddhi GuptaОценок пока нет

- Adv Acc Q.P 2Документ7 страницAdv Acc Q.P 2Swetha ReddyОценок пока нет

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionДокумент7 страницCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiОценок пока нет

- Analysis of Financial StatementДокумент23 страницыAnalysis of Financial StatementMohammad Tariq AnsariОценок пока нет

- Company and Cost ManagementДокумент11 страницCompany and Cost ManagementPadmambigai Chandra SekaranОценок пока нет

- 1 Financial Statements of CompaniesДокумент21 страница1 Financial Statements of CompaniesShivaram ShivaramОценок пока нет

- Master of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Документ4 страницыMaster of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Namrata RamgadeОценок пока нет

- Valuation of GoodwillДокумент15 страницValuation of Goodwillbtsa1262013Оценок пока нет

- DocumentДокумент4 страницыDocumentTûshar ThakúrОценок пока нет

- CMA Final CFR MarathonДокумент30 страницCMA Final CFR MarathonRamanpreet KaurОценок пока нет

- AFM Assignment 2021Документ7 страницAFM Assignment 2021NARENDRA PATTELAОценок пока нет

- Company Accounts, Cost and Management AccountingДокумент10 страницCompany Accounts, Cost and Management AccountingmeetwithsanjayОценок пока нет

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Документ3 страницыAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaОценок пока нет

- 12 Acs (S) - Set A 19.7.2021Документ3 страницы12 Acs (S) - Set A 19.7.2021Sakshi NagotkarОценок пока нет

- Accounting Redemption of Debentures 1642416359Документ19 страницAccounting Redemption of Debentures 1642416359Shashank SikarwarОценок пока нет

- FR Suggested May 2018Документ31 страницаFR Suggested May 2018Rahul NandurkarОценок пока нет

- Internal Reconstruction - ProblemsДокумент8 страницInternal Reconstruction - ProblemsNaomi SaldanhaОценок пока нет

- 73535bos59345 Final p2qДокумент6 страниц73535bos59345 Final p2qSakshi vermaОценок пока нет

- 027 Practice Test 09 Accounting Test Solution Subjective Udesh RegularДокумент6 страниц027 Practice Test 09 Accounting Test Solution Subjective Udesh Regulardeathp006Оценок пока нет

- Buy Back of Shares HandoutДокумент15 страницBuy Back of Shares Handoutdhiren.c.shekar99Оценок пока нет

- Master Questions, Advance Level Questions and Additional Questions-Chapter 4Документ18 страницMaster Questions, Advance Level Questions and Additional Questions-Chapter 4manmeet0001Оценок пока нет

- Corrporate ModelДокумент10 страницCorrporate Modelnithinjoseph562005Оценок пока нет

- EXERCISE Cashflow of The CompanyДокумент41 страницаEXERCISE Cashflow of The CompanyDev lakhaniОценок пока нет

- Siddharth Education Services LTDДокумент5 страницSiddharth Education Services LTDBasanta K SahuОценок пока нет

- Internal Reconstruction NotesДокумент16 страницInternal Reconstruction NotesAkash Mehta100% (1)

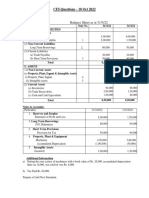

- CFS Questions - 18 - OCT - 2022Документ5 страницCFS Questions - 18 - OCT - 2022Kartik SujanОценок пока нет

- Delhi Public School Jodhpur: General InstructionsДокумент4 страницыDelhi Public School Jodhpur: General Instructionssamyak patwaОценок пока нет

- Paper18 Solution PDFДокумент24 страницыPaper18 Solution PDFI'm Just FunnyОценок пока нет

- Gujarat Technological UniversityДокумент6 страницGujarat Technological UniversitymansiОценок пока нет

- AFM ProblemsДокумент4 страницыAFM ProblemskuselvОценок пока нет

- Solution:: Equity and LiabilitiesДокумент4 страницыSolution:: Equity and LiabilitiesNIMROD MOCHAHARIОценок пока нет

- Fin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningДокумент12 страницFin Reporting and FSA-fund Flow Statment 6th Sem by VS (Vinay Shaw0 For MorningSarfraz AhmedОценок пока нет

- Ancial Accounting October 2010Документ6 страницAncial Accounting October 2010vinit tandelОценок пока нет

- Internal ReconstructionДокумент26 страницInternal ReconstructionRajesh NangaliaОценок пока нет

- CA Bcom PH 3rd Sem 2016Документ7 страницCA Bcom PH 3rd Sem 2016Gursirat KaurОценок пока нет

- Dwaraka Doss Goverdhan Doss Vaishnav College (Autonomous) Arumbakkam, Chennai - 600 106. Department of Corporate Secretaryship Core Paper V-Corporate AccountingДокумент4 страницыDwaraka Doss Goverdhan Doss Vaishnav College (Autonomous) Arumbakkam, Chennai - 600 106. Department of Corporate Secretaryship Core Paper V-Corporate AccountingNeeraj DОценок пока нет

- AdvДокумент19 страницAdvashwin krishnaОценок пока нет

- Assignment For AccountancyДокумент3 страницыAssignment For AccountancyKamlesh PandeyОценок пока нет

- Financial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)Документ5 страницFinancial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)tanmoy sardarОценок пока нет

- CR Assignemt Unit 3Документ25 страницCR Assignemt Unit 3Calida SoaresОценок пока нет

- 12 Accountancy Notes CH12 Cash Flow Statement 02Документ28 страниц12 Accountancy Notes CH12 Cash Flow Statement 02Gourab GoraiОценок пока нет

- 232 FM AssignmentДокумент17 страниц232 FM Assignmentbhupesh joshiОценок пока нет

- 3054 Faca-V L 8Документ8 страниц3054 Faca-V L 8ab6154951Оценок пока нет

- Balance Sheet FormatДокумент30 страницBalance Sheet Formatpre.meh21Оценок пока нет

- Age No 5Документ126 страницAge No 5Deeran DhayanithiRPОценок пока нет

- 19013comp Sugans Pe2 Accounting Cp8 5Документ12 страниц19013comp Sugans Pe2 Accounting Cp8 5Ubaidulla MachingalОценок пока нет

- Management Accounitng - 104 (I)Документ4 страницыManagement Accounitng - 104 (I)Rudraksh PareyОценок пока нет

- Problems Set On Ratio AnalysisДокумент7 страницProblems Set On Ratio AnalysispriyankaОценок пока нет

- Test - Section B - Corporate AccountingДокумент3 страницыTest - Section B - Corporate AccountingNathoОценок пока нет

- Class 12 Accountancy CBSE Cash Flow StatementДокумент7 страницClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharОценок пока нет

- 9 Consolidated Financial StatementsДокумент20 страниц9 Consolidated Financial StatementsArpan SinghОценок пока нет

- Buy-Back Assignment PDFДокумент1 страницаBuy-Back Assignment PDFDhairya ShahОценок пока нет

- MacroEco PPT USAДокумент15 страницMacroEco PPT USADhairya ShahОценок пока нет

- Forest CoverДокумент12 страницForest CoverDhairya ShahОценок пока нет

- Buy-Back Assignment Note Batch - IДокумент1 страницаBuy-Back Assignment Note Batch - IDhairya ShahОценок пока нет

- Practice Problems On Long Term Financing and Cost of CapitalДокумент8 страницPractice Problems On Long Term Financing and Cost of CapitalDhairya ShahОценок пока нет

- Turnbull Corp., Cost of Capital Based On Book ValueДокумент9 страницTurnbull Corp., Cost of Capital Based On Book ValueDhairya ShahОценок пока нет

- Abstract Submission - Fintech FinalДокумент15 страницAbstract Submission - Fintech FinalYashvi ShahОценок пока нет

- Elements of Law: EL Batch Number Group NumberДокумент15 страницElements of Law: EL Batch Number Group NumberDhairya ShahОценок пока нет

- Data Collection of CGДокумент60 страницData Collection of CGDhairya ShahОценок пока нет

- Take Home Quiz PDFДокумент5 страницTake Home Quiz PDFDhairya ShahОценок пока нет

- Dhairya Shah AU1813069 Response Paper 1Документ5 страницDhairya Shah AU1813069 Response Paper 1Dhairya ShahОценок пока нет

- Take Home Quiz PDFДокумент5 страницTake Home Quiz PDFDhairya ShahОценок пока нет

- Dhairya Shah AU1813069 Response Paper 2Документ6 страницDhairya Shah AU1813069 Response Paper 2Dhairya ShahОценок пока нет

- Dhairya Shah 1813069 CG Response Paper 3Документ6 страницDhairya Shah 1813069 CG Response Paper 3Dhairya ShahОценок пока нет

- Take Home Quiz PDFДокумент5 страницTake Home Quiz PDFDhairya ShahОценок пока нет

- Tutorial 4 AnswerДокумент7 страницTutorial 4 AnswernajihahОценок пока нет

- Practical Accounting 1 Vol 2 ValixДокумент349 страницPractical Accounting 1 Vol 2 ValixJan Vincent De JesusОценок пока нет

- Advanced Financial Accounting and Reporting Course OutlineДокумент3 страницыAdvanced Financial Accounting and Reporting Course Outlineselman AregaОценок пока нет

- Chapter 1Документ2 страницыChapter 1Nguyễn Thùy LinhОценок пока нет

- Topic 2 Financial EnvironmentДокумент11 страницTopic 2 Financial EnvironmentMardi UmarОценок пока нет

- Topic: Financial Management Function: Advantages of Profit MaximizationДокумент4 страницыTopic: Financial Management Function: Advantages of Profit MaximizationDilah PhsОценок пока нет

- A Dummy's Guide To Marketing - The ISB HandbookДокумент85 страницA Dummy's Guide To Marketing - The ISB Handbookmanavgupta2656Оценок пока нет

- Topic: Investment Analysis: About Aditya Birla Money LimitedДокумент3 страницыTopic: Investment Analysis: About Aditya Birla Money LimitedRaja ShekerОценок пока нет

- M and N 1Документ1 страницаM and N 1DDdОценок пока нет

- Income Statement and Related Information: Intermediate AccountingДокумент64 страницыIncome Statement and Related Information: Intermediate AccountingAdnan AbirОценок пока нет

- Pran AnalysisДокумент11 страницPran AnalysisMd TaimurОценок пока нет

- Mama Earth-1Документ20 страницMama Earth-1Manpreet SinghОценок пока нет

- Redemption of DebenturesДокумент14 страницRedemption of DebenturesHitesh Mendiratta100% (1)

- Assets and Liability Management: A Project Report ONДокумент12 страницAssets and Liability Management: A Project Report ONMohmmedKhayyumОценок пока нет

- MC 2022 25 CooperativesДокумент79 страницMC 2022 25 CooperativesRonnell Vic Cañeda YuОценок пока нет

- Titman - PPT - CH04 - Financial Analysis v4Документ68 страницTitman - PPT - CH04 - Financial Analysis v4Hein HОценок пока нет

- Folio Detail ReportДокумент50 страницFolio Detail ReportBaljit kaurОценок пока нет

- Graduation Project Report: Modelling Liquidity Dynamics in North America's Stock MarketsДокумент66 страницGraduation Project Report: Modelling Liquidity Dynamics in North America's Stock MarketsKhalil M'hamedОценок пока нет

- 12 x10 Financial Statement AnalysisДокумент19 страниц12 x10 Financial Statement AnalysisHazel Jael HernandezОценок пока нет

- Regulatory Changes: Initiated by SEBIДокумент6 страницRegulatory Changes: Initiated by SEBINachammai SwaminathanОценок пока нет

- A Study of Awareness About Forex Market at DharwadДокумент17 страницA Study of Awareness About Forex Market at DharwadSanjay KaradiОценок пока нет

- Chap 2 Cost of Capital MainДокумент33 страницыChap 2 Cost of Capital Maintemesgen yohannesОценок пока нет