Вам также может понравиться

- Malaysia q1Документ3 страницыMalaysia q1IT manОценок пока нет

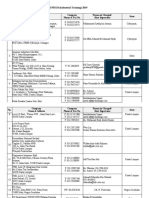

- List of Recommended Companies 2019Документ6 страницList of Recommended Companies 2019IT man100% (1)

- The Binomial, Poisson, and Normal Distributions: Modified After Powerpoint by Carlos J. Rosas-AndersonДокумент39 страницThe Binomial, Poisson, and Normal Distributions: Modified After Powerpoint by Carlos J. Rosas-AndersonIT manОценок пока нет

- Topic 3 - System AnalysisДокумент39 страницTopic 3 - System AnalysisIT manОценок пока нет

- Application For An Industrial Training Placement: Diploma in Computer ScienceДокумент3 страницыApplication For An Industrial Training Placement: Diploma in Computer ScienceIT manОценок пока нет

- Org and IS No Organization Information System Matrix No. Ending WithДокумент1 страницаOrg and IS No Organization Information System Matrix No. Ending WithIT manОценок пока нет

- MEMB221 SEM 2 1718 Mechanics and Materials Lab Section 3 Group 1 ID NameДокумент2 страницыMEMB221 SEM 2 1718 Mechanics and Materials Lab Section 3 Group 1 ID NameIT manОценок пока нет

- Tutorial Questions 4 PDFДокумент1 страницаTutorial Questions 4 PDFIT manОценок пока нет

- Tutorial For Quiz 1 PDFДокумент2 страницыTutorial For Quiz 1 PDFIT manОценок пока нет

- CEPB323 - Project Report Cover (Part 2 - Project Management Report) Sem Special 1920Документ1 страницаCEPB323 - Project Report Cover (Part 2 - Project Management Report) Sem Special 1920IT manОценок пока нет

- Tutorial For Quiz 1 PDFДокумент2 страницыTutorial For Quiz 1 PDFIT manОценок пока нет

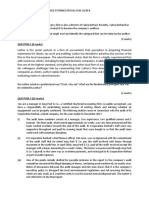

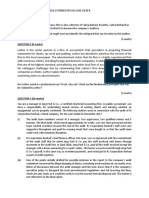

- Review Questions: Introduction To Internal Auditing: AUDB323 Audit and InvestigationДокумент1 страницаReview Questions: Introduction To Internal Auditing: AUDB323 Audit and InvestigationIT manОценок пока нет

- Company Facts PresentationДокумент25 страницCompany Facts PresentationIT manОценок пока нет

- Topic 3 PDFДокумент40 страницTopic 3 PDFIT manОценок пока нет

- Tutorial 8 PDFДокумент1 страницаTutorial 8 PDFIT manОценок пока нет

- Tutorial 5 PDFДокумент1 страницаTutorial 5 PDFIT manОценок пока нет

- Review Questions: Effect of Post-Balance Sheet EventsДокумент1 страницаReview Questions: Effect of Post-Balance Sheet EventsIT manОценок пока нет

- CISB474 Business Analytics Sem 2 Year 2016/2017 Lab 8 Linear RegressionДокумент4 страницыCISB474 Business Analytics Sem 2 Year 2016/2017 Lab 8 Linear RegressionIT manОценок пока нет

- Topic 4 PDFДокумент15 страницTopic 4 PDFIT manОценок пока нет

- Exercises/Problems:) R 1 (Ue Termnalval VCF) R 1 (VCF) R 1 (VCF) R 1 (VCF) R 1 (VCFДокумент1 страницаExercises/Problems:) R 1 (Ue Termnalval VCF) R 1 (VCF) R 1 (VCF) R 1 (VCF) R 1 (VCFIT manОценок пока нет

- Entrepreneurial Finance Leach & Melicher: Venture Capital Valuation MethodsДокумент29 страницEntrepreneurial Finance Leach & Melicher: Venture Capital Valuation MethodsIT manОценок пока нет

- Role of Information Systems in HealthcareДокумент3 страницыRole of Information Systems in HealthcareIT manОценок пока нет

- Air Asia Case StudyДокумент11 страницAir Asia Case StudyIT man100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Letter From LysandraДокумент1 страницаLetter From Lysandraapi-513508097Оценок пока нет

- Resume - Neidow 2020Документ2 страницыResume - Neidow 2020api-275293617Оценок пока нет

- AF - Aquaculture NC II 20151119Документ28 страницAF - Aquaculture NC II 20151119Michael ParejaОценок пока нет

- Jenny Totman ResumeДокумент1 страницаJenny Totman Resumeapi-317206363Оценок пока нет

- VisualSpeller by Garborro.D (2011)Документ52 страницыVisualSpeller by Garborro.D (2011)LydiaRyooОценок пока нет

- Scale Drawing AssessmentДокумент2 страницыScale Drawing Assessmentapi-251328165100% (1)

- Nepf Lesson Plan PrepДокумент2 страницыNepf Lesson Plan Prepapi-460649413100% (1)

- Session F-2 - Statistics and Probability For Middle-School Math Te PDFДокумент25 страницSession F-2 - Statistics and Probability For Middle-School Math Te PDFFloravy Dimple Baisac ParantarОценок пока нет

- Short Story Lesson PlanДокумент4 страницыShort Story Lesson Planapi-372387144Оценок пока нет

- Research MethodologyДокумент338 страницResearch MethodologyKabutu Chuunga75% (8)

- Teaching Portfolio Rationale - Standard 3 - Sub 3Документ1 страницаTeaching Portfolio Rationale - Standard 3 - Sub 3api-457603008Оценок пока нет

- O Level Pakistan Studies 2059/01: Unit 14Документ3 страницыO Level Pakistan Studies 2059/01: Unit 14mstudy123456Оценок пока нет

- 07car Assmnt & MBTI - McCaulleyДокумент22 страницы07car Assmnt & MBTI - McCaulleyaiklussОценок пока нет

- AIMTDR BrochureДокумент6 страницAIMTDR Brochurekachu0408Оценок пока нет

- Feminism in The French RevolutionДокумент21 страницаFeminism in The French RevolutionSarianaDTОценок пока нет

- Group Leadership Case StudyДокумент5 страницGroup Leadership Case StudymatthewivanОценок пока нет

- Benefits of ReadingДокумент4 страницыBenefits of ReadingKelly Cham100% (4)

- Greg Hardin CVДокумент7 страницGreg Hardin CVgreg hardinОценок пока нет

- The Leadership ChalengeДокумент88 страницThe Leadership ChalengeSrinivas Rao GunjaОценок пока нет

- Why College & MajorДокумент29 страницWhy College & MajorbmegamenОценок пока нет

- Imb Teacher InterviewДокумент3 страницыImb Teacher Interviewapi-237871207Оценок пока нет

- Nursing AuditДокумент28 страницNursing Auditmarsha100% (1)

- The Revolutionarys Guide To Learning and Teaching LanguagesДокумент26 страницThe Revolutionarys Guide To Learning and Teaching LanguagesNataVОценок пока нет

- CV - Danielle BerkelmansДокумент3 страницыCV - Danielle Berkelmansapi-228252473Оценок пока нет

- Narrative Report On Buwan NG Pagbasa Celebration With PictorialsДокумент6 страницNarrative Report On Buwan NG Pagbasa Celebration With PictorialsJolymar Liquigan100% (1)

- Creativity TestДокумент8 страницCreativity TestHaslina SaidОценок пока нет

- University of Cambridge International ExaminationsДокумент5 страницUniversity of Cambridge International ExaminationsHubbak KhanОценок пока нет

- TTT Presentation Skills Workbook PDFДокумент61 страницаTTT Presentation Skills Workbook PDFgopalranjan_2000939Оценок пока нет

- ATSEP Guidelines Competence Assesment L7-Released Issue With SignatureДокумент44 страницыATSEP Guidelines Competence Assesment L7-Released Issue With SignatureHANSA blogОценок пока нет

- Curriculum VitaeДокумент3 страницыCurriculum Vitaeᜐᜋᜒ ᜀᜈᜓОценок пока нет