Вам также может понравиться

- Braced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationОт EverandBraced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationОценок пока нет

- 71746bos071022 Inter P6aДокумент10 страниц71746bos071022 Inter P6aTutulОценок пока нет

- 2011 Winter SolutionsДокумент7 страниц2011 Winter SolutionsSaadat AkhundОценок пока нет

- At Quiz 2 - October 2019Документ3 страницыAt Quiz 2 - October 2019Mitchiejash CruzОценок пока нет

- 8int 2011 Jun AДокумент9 страниц8int 2011 Jun ADawn CaldeiraОценок пока нет

- CAF 8 Autumn 2021Документ7 страницCAF 8 Autumn 2021hamizОценок пока нет

- 8sgp 2011 Jun AДокумент9 страниц8sgp 2011 Jun Awina meschaОценок пока нет

- Aud689 Feb2022 SsДокумент6 страницAud689 Feb2022 SsAlexОценок пока нет

- Winter 2018Документ7 страницWinter 2018Muhammad QamarОценок пока нет

- Auditing - AnswersДокумент9 страницAuditing - Answerspriyanshagrawal907Оценок пока нет

- Rrpao 1Документ12 страницRrpao 1mr rahulОценок пока нет

- NFJPIA Mock Board 2016 - AuditingДокумент8 страницNFJPIA Mock Board 2016 - AuditingClareng Anne100% (1)

- A. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientДокумент7 страницA. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientRenОценок пока нет

- At.3602 - Introduction To Audit and Other Assurance ServicesДокумент7 страницAt.3602 - Introduction To Audit and Other Assurance ServicesRona Amor MundaОценок пока нет

- Preliminary Engagement and Audit Planning QuizДокумент7 страницPreliminary Engagement and Audit Planning QuizGraceila P. CalopeОценок пока нет

- Audit & Assurance: Suggested AnswersДокумент9 страницAudit & Assurance: Suggested AnswersMuhammad HussainОценок пока нет

- Practice Question AnswersДокумент15 страницPractice Question AnswersSANDALI FERNANDOОценок пока нет

- 2009 Winter SolutionsДокумент5 страниц2009 Winter SolutionsSaadat AkhundОценок пока нет

- Audit Suggested Ans CA Inter Nov 20Документ14 страницAudit Suggested Ans CA Inter Nov 20Priyansh KhatriОценок пока нет

- Examenes 07 14 November 2015 Questions and AnswersДокумент78 страницExamenes 07 14 November 2015 Questions and Answerskris mОценок пока нет

- Acctg 34 ReviewerДокумент9 страницAcctg 34 ReviewerAboc May AnОценок пока нет

- ATДокумент8 страницATNoemi MacatangayОценок пока нет

- CAF 8 Spring 2022Документ6 страницCAF 8 Spring 2022hamizОценок пока нет

- Solution Aud589 - Dec 2015Документ7 страницSolution Aud589 - Dec 2015LANGITBIRUОценок пока нет

- 73662bos59508 Inter P6aДокумент10 страниц73662bos59508 Inter P6adeepika devsaniОценок пока нет

- MTP 3 21 Answers 1681446073Документ10 страницMTP 3 21 Answers 1681446073shoaibinamdar1454Оценок пока нет

- A3 - Topic 1Документ7 страницA3 - Topic 1jgames777Оценок пока нет

- Cfap 6 Winter 2018 AnsДокумент8 страницCfap 6 Winter 2018 AnsMariya AmberОценок пока нет

- Department of Accountancy: Page - 1Документ17 страницDepartment of Accountancy: Page - 1NoroОценок пока нет

- Preboard Exam - AuditДокумент10 страницPreboard Exam - AuditLeopoldo Reuteras Morte IIОценок пока нет

- © The Institute of Chartered Accountants of India: (2 X 7 14 Marks)Документ14 страниц© The Institute of Chartered Accountants of India: (2 X 7 14 Marks)Kirthiga dhinakaranОценок пока нет

- December 20 SolutionsДокумент9 страницDecember 20 SolutionsVincent LyОценок пока нет

- ACY55 Summative Exam Answer KeyДокумент3 страницыACY55 Summative Exam Answer KeyAMIKO OHYAОценок пока нет

- AuditNew Nov18 Suggested Ans CA InterДокумент15 страницAuditNew Nov18 Suggested Ans CA InterRishabh jainОценок пока нет

- ReSA B45 AUD First PB Exam - Questions, Answers - SolutionsДокумент21 страницаReSA B45 AUD First PB Exam - Questions, Answers - SolutionsDhainne Enriquez100% (1)

- CFAP 6 Winter 2022 PDFДокумент7 страницCFAP 6 Winter 2022 PDFAli HaiderОценок пока нет

- 75781bos61308 p6Документ15 страниц75781bos61308 p6pratimca592Оценок пока нет

- © The Institute of Chartered Accountants of IndiaДокумент14 страниц© The Institute of Chartered Accountants of IndialovedesuzaОценок пока нет

- Auditing Theory Chapter 9 Summary NotesДокумент10 страницAuditing Theory Chapter 9 Summary NotesJwyneth Royce DenolanОценок пока нет

- Long Test Part 2 QuestionnaireДокумент6 страницLong Test Part 2 QuestionnaireHarold FilomenoОценок пока нет

- Solution Aud610 - Jan 2012Документ8 страницSolution Aud610 - Jan 2012Emelia AnizaОценок пока нет

- CH05 PDFДокумент58 страницCH05 PDFPhatma Ezahra ManaiОценок пока нет

- Tutorial 3-Audit Risk and Materiality MCQДокумент10 страницTutorial 3-Audit Risk and Materiality MCQcynthiama7777Оценок пока нет

- Preliminary Exam Reviewer1Документ77 страницPreliminary Exam Reviewer1Adam Smith0% (1)

- Chapter 4 Risks and Materiality: Answer 1Документ4 страницыChapter 4 Risks and Materiality: Answer 1AhmadYaseenОценок пока нет

- Excel Professional Services, Inc.: Discussion QuestionsДокумент4 страницыExcel Professional Services, Inc.: Discussion QuestionsSadAccountantОценок пока нет

- Auditing RevisionДокумент6 страницAuditing RevisionCodyxanssОценок пока нет

- Test Banks - Auditing TheoriesДокумент8 страницTest Banks - Auditing TheoriesDawn Rei DangkiwОценок пока нет

- Acctg 16a - Midterm ExamДокумент6 страницAcctg 16a - Midterm ExamChriestal SorianoОценок пока нет

- Auditing QuestionДокумент7 страницAuditing QuestionWaqar AmjadОценок пока нет

- Common Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesДокумент8 страницCommon Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesNur Dina AbsbОценок пока нет

- CA Final Audit Nov'2020 Old Syllabus-SAДокумент16 страницCA Final Audit Nov'2020 Old Syllabus-SABhumeeka GargОценок пока нет

- Auditing: Page 1 of 8Документ8 страницAuditing: Page 1 of 8jeams vidalОценок пока нет

- MTP m21 A Ans 2Документ8 страницMTP m21 A Ans 2sakshiОценок пока нет

- Audit Questions - RACДокумент7 страницAudit Questions - RACJean PaladaОценок пока нет

- CA Inter Audit A MTP 2 May 23Документ10 страницCA Inter Audit A MTP 2 May 23Sam KukrejaОценок пока нет

- Accountancy Review Center (ARC) of The Philippines Inc.: First Preboard ExamДокумент3 страницыAccountancy Review Center (ARC) of The Philippines Inc.: First Preboard ExamCarlo AgravanteОценок пока нет

- Harisenin Mini School - To AuditДокумент17 страницHarisenin Mini School - To AuditFitria Ramadhani AyuningtyasОценок пока нет

- Misc. Practice QuestionsДокумент2 страницыMisc. Practice QuestionsMuhammadNaumanОценок пока нет

- FAUINT 2012 Jun A PDFДокумент9 страницFAUINT 2012 Jun A PDFMessi GenaroОценок пока нет

- The Institute of Chartered Accountants of PakistanДокумент4 страницыThe Institute of Chartered Accountants of PakistanAОценок пока нет

- Audit and Assurance: Certificate in Accounting and Finance Stage ExaminationДокумент2 страницыAudit and Assurance: Certificate in Accounting and Finance Stage ExaminationAОценок пока нет

- The Institute of Chartered Accountants of PakistanДокумент5 страницThe Institute of Chartered Accountants of PakistanAОценок пока нет

- Introduction - To - Financial - AccountingДокумент3 страницыIntroduction - To - Financial - AccountingAОценок пока нет

- Subject: CAF-7 FAR II (Test 4) Teacher: Sir Nasir Abbas Date: May 29, 2021Документ2 страницыSubject: CAF-7 FAR II (Test 4) Teacher: Sir Nasir Abbas Date: May 29, 2021AОценок пока нет

- CFAP 6 AARS Winter 2020Документ4 страницыCFAP 6 AARS Winter 2020AОценок пока нет

- Section: C-1 CAF-04: BMBS Teacher:Mr Zia-Ul-Haq Total Marks:20 Time Allowed: 35 Minutes DateДокумент2 страницыSection: C-1 CAF-04: BMBS Teacher:Mr Zia-Ul-Haq Total Marks:20 Time Allowed: 35 Minutes DateAОценок пока нет

- CAF-09 Audit & Assurance: Re Me MB Er Me in PrayersДокумент1 страницаCAF-09 Audit & Assurance: Re Me MB Er Me in PrayersAОценок пока нет

- Test 4Документ1 страницаTest 4AОценок пока нет

- Audit, Assurance and Related Services: Page 1 of 10Документ10 страницAudit, Assurance and Related Services: Page 1 of 10AОценок пока нет

- 01 Mark For Discussing Each Relevant Audit Risk 0.5 Mark For Each Key Audit Procedure To Be Performed Against The Identified RisksДокумент1 страница01 Mark For Discussing Each Relevant Audit Risk 0.5 Mark For Each Key Audit Procedure To Be Performed Against The Identified RisksAОценок пока нет

- Cfap 1 Afr Winter 2020Документ5 страницCfap 1 Afr Winter 2020AОценок пока нет

- CFAP 1 AAFR Winter 2020Документ2 страницыCFAP 1 AAFR Winter 2020AОценок пока нет

- Human Heart PDFДокумент1 страницаHuman Heart PDFAОценок пока нет

- Ucm 307643 PDFДокумент2 страницыUcm 307643 PDFAОценок пока нет

- Audit Icap Updated Chapterwise Past Paper With Solution V1 Prepared by Fahad Irfan-1Документ1 страницаAudit Icap Updated Chapterwise Past Paper With Solution V1 Prepared by Fahad Irfan-1AОценок пока нет

- AERACardio - Client Brochure - Heart Disease and Congestive HeartДокумент2 страницыAERACardio - Client Brochure - Heart Disease and Congestive HeartAОценок пока нет

- Introduction To Accounting and Bookkeeping (20-30)Документ1 страницаIntroduction To Accounting and Bookkeeping (20-30)AОценок пока нет

- RISE Book: Chapter 5 (LO 12 Half) ICAP S Study Text Reference: 5.4.5 ICAP S Question Bank Reference: 5.17, 5.18, 5.19, 5.20, 5.21Документ1 страницаRISE Book: Chapter 5 (LO 12 Half) ICAP S Study Text Reference: 5.4.5 ICAP S Question Bank Reference: 5.17, 5.18, 5.19, 5.20, 5.21AОценок пока нет

- CAF01 25 Days PDFДокумент1 страницаCAF01 25 Days PDFAОценок пока нет

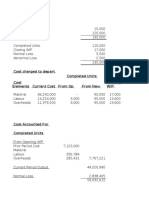

- Costing Solution: Ahmed Raza Mir, ACAДокумент2 страницыCosting Solution: Ahmed Raza Mir, ACAAОценок пока нет

- Costing Solution: Proposed Case Current CaseДокумент5 страницCosting Solution: Proposed Case Current CaseAОценок пока нет

- TAX Mock PACДокумент6 страницTAX Mock PACAОценок пока нет

- CAF01 25 DaysДокумент1 страницаCAF01 25 DaysAОценок пока нет

- MemoryMic Quick Guide 04 2018Документ2 страницыMemoryMic Quick Guide 04 2018AОценок пока нет

- Costing Solution: Manaufacturing Cost X1 X2 X3 X4Документ3 страницыCosting Solution: Manaufacturing Cost X1 X2 X3 X4AОценок пока нет

- CAF-07 FAR-II Q. Paper (Final)Документ5 страницCAF-07 FAR-II Q. Paper (Final)AОценок пока нет

- Question 4Документ3 страницыQuestion 4AОценок пока нет

- Introduction To Economics and Finance: MOCK (Spring 2013) Section: B 100 Marks-3hoursДокумент5 страницIntroduction To Economics and Finance: MOCK (Spring 2013) Section: B 100 Marks-3hoursAОценок пока нет

- ACCA p1 Notes PDFДокумент230 страницACCA p1 Notes PDFmullazakОценок пока нет

- Northwell Health 2019 Audited Financial StatementsДокумент81 страницаNorthwell Health 2019 Audited Financial StatementsJonathan LaMantiaОценок пока нет

- Auditing and Assurance Specialized IndustriesДокумент61 страницаAuditing and Assurance Specialized IndustriesCrizza Demecillo100% (2)

- CA Final SA Concept by Siddharth AgarwalДокумент54 страницыCA Final SA Concept by Siddharth Agarwalvishnuverma100% (1)

- Comprehensive Annual: Mayor Chokwe A. LumumbaДокумент237 страницComprehensive Annual: Mayor Chokwe A. Lumumbathe kingfishОценок пока нет

- Commercial Bank Examination Manual PDFДокумент1 818 страницCommercial Bank Examination Manual PDFJoshua Sygnal GutierrezОценок пока нет

- THESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementДокумент46 страницTHESIS Measures Taken by SMEs in Bacolod City For Financial Audit Quality EnhancementVon Ianelle AguilaОценок пока нет

- Cobit 2019Документ12 страницCobit 2019Nur Ifawati ArfanОценок пока нет

- GTB 2017aДокумент386 страницGTB 2017afisayobabs11Оценок пока нет

- Bank AuditingДокумент38 страницBank AuditingClene DoconteОценок пока нет

- PrE1 Auditor's ResponsibityДокумент17 страницPrE1 Auditor's ResponsibityAbegail Kaye BiadoОценок пока нет

- Auditing Intangible Assets and Evaluating Fair Market Value: The Case of Reacquired Franchise RightsДокумент18 страницAuditing Intangible Assets and Evaluating Fair Market Value: The Case of Reacquired Franchise RightsResgitanadila MasyaОценок пока нет

- Administrative Manual: St. Andrew Montessori and High School, IncДокумент9 страницAdministrative Manual: St. Andrew Montessori and High School, Incrhey100% (1)

- At 04 Audit Evidence and Audit Documentation PDFДокумент6 страницAt 04 Audit Evidence and Audit Documentation PDFMadelyn Jane IgnacioОценок пока нет

- Chapter 19 AuditingДокумент12 страницChapter 19 AuditingMisshtaCОценок пока нет

- Oracle Risk Management Key Use CasesДокумент13 страницOracle Risk Management Key Use CasesToqeer AhmedОценок пока нет

- Test Bank For Accounting Information Systems 1e by Turner and WeickgenanntДокумент16 страницTest Bank For Accounting Information Systems 1e by Turner and Weickgenanntcynthiaacostabsjeiaxmqk100% (37)

- Internal Auditing Assurance and Advisory Services 4th Edition PPT PresentationДокумент18 страницInternal Auditing Assurance and Advisory Services 4th Edition PPT PresentationBunga Asokawati Putri Darajat100% (1)

- DPPL Annual Report 2016-17Документ63 страницыDPPL Annual Report 2016-17xyzОценок пока нет

- 1.sa Question Bank Latest Atul Agarwal Studyfromnotes - Com WДокумент59 страниц1.sa Question Bank Latest Atul Agarwal Studyfromnotes - Com WDeepakОценок пока нет

- Pending Points To Be DiscussedДокумент6 страницPending Points To Be DiscussedGaurav ModiОценок пока нет

- e-CAT OrientationДокумент24 страницыe-CAT OrientationGreggy Roy Marquez100% (1)

- ACCA-AB - Workbook - Student Copy - Jan2019 PDFДокумент460 страницACCA-AB - Workbook - Student Copy - Jan2019 PDFLinh Thuy100% (1)

- AR 11-31 Army Security Cooperation PolicyДокумент19 страницAR 11-31 Army Security Cooperation PolicyfahmynastОценок пока нет

- A20 Midterm ReviewerДокумент2 страницыA20 Midterm ReviewerEy EmОценок пока нет

- Accounting ControlsДокумент3 страницыAccounting ControlsPankaj GautamОценок пока нет

- Japanese Guidelines For Internal Control Reporting Finalized Differences in Requirements Between The U.S. Sarbanes-Oxley Act and JДокумент10 страницJapanese Guidelines For Internal Control Reporting Finalized Differences in Requirements Between The U.S. Sarbanes-Oxley Act and JManna MahadiОценок пока нет

- Independent Director Exam Questions and AnswersДокумент185 страницIndependent Director Exam Questions and AnswersRitesh Bhatia100% (8)

- (Admission of Associate Member Is Optional) : Credit Coopertive By-LawsДокумент24 страницы(Admission of Associate Member Is Optional) : Credit Coopertive By-LawsErrand MercadoОценок пока нет

- Audit ExamДокумент29 страницAudit Exam101bus85% (13)