Вам также может понравиться

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Check your MF answersДокумент19 страницCheck your MF answersyogidildar100% (1)

- Strategic Financial Management - Investment Appraisal - RCF, PP, DPP, TVM, ARR - Dayana MasturaДокумент23 страницыStrategic Financial Management - Investment Appraisal - RCF, PP, DPP, TVM, ARR - Dayana MasturaDayana MasturaОценок пока нет

- PWC Basel III Capital Market Risk Final RuleДокумент30 страницPWC Basel III Capital Market Risk Final RuleSara HumayunОценок пока нет

- PR - Order in The Matter of M/s Wasankar Wealth Management Limited, Wasankar Investments and OthersДокумент1 страницаPR - Order in The Matter of M/s Wasankar Wealth Management Limited, Wasankar Investments and OthersShyam SunderОценок пока нет

- IAS 34 Interim Financial Reporting PDFДокумент26 страницIAS 34 Interim Financial Reporting PDFgeorgep0% (1)

- Report Petro ItauДокумент11 страницReport Petro ItauQuatroAОценок пока нет

- Financial ManagementДокумент31 страницаFinancial ManagementShashikant MishraОценок пока нет

- Group Statement of Financial Position RecapДокумент14 страницGroup Statement of Financial Position RecapSahilPatelОценок пока нет

- Translation of Foreign Currency Financial StatementsДокумент27 страницTranslation of Foreign Currency Financial StatementsSurip BachtiarОценок пока нет

- SWAPДокумент18 страницSWAPashish3009Оценок пока нет

- 3rdyr - 1stF - Accounting For Business Combinations - 2324Документ34 страницы3rdyr - 1stF - Accounting For Business Combinations - 2324zaounxosakubОценок пока нет

- 620000977631310-VAL APLNoticeДокумент2 страницы620000977631310-VAL APLNoticesiti awangОценок пока нет

- Depletion Notes: Disclaimer: Not EntirelyДокумент3 страницыDepletion Notes: Disclaimer: Not EntirelyRes GosanОценок пока нет

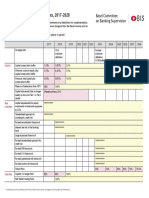

- Basel III transitional arrangements 2017-2028 summaryДокумент1 страницаBasel III transitional arrangements 2017-2028 summarygoonОценок пока нет

- Manch 4.0 Project List: For Internal Use OnlyДокумент8 страницManch 4.0 Project List: For Internal Use OnlyHimanshu KumarОценок пока нет

- Difference Between Accounts & FinanceДокумент4 страницыDifference Between Accounts & Financesameer amjadОценок пока нет

- IFRS Vs US GAAPДокумент5 страницIFRS Vs US GAAPtibebu5420Оценок пока нет

- Apollo HospitalsДокумент18 страницApollo HospitalsvishalОценок пока нет

- Ecm & DCMДокумент114 страницEcm & DCMYuqingОценок пока нет

- Capital Budgeting Analysis of Overseas SubsidiaryДокумент12 страницCapital Budgeting Analysis of Overseas SubsidiaryThao Bui ThiОценок пока нет

- National University of Science and TechnologyДокумент8 страницNational University of Science and TechnologyPATIENCE MUSHONGAОценок пока нет

- MA2 Managing Cost - Finance Notes Complete FileДокумент129 страницMA2 Managing Cost - Finance Notes Complete FileUzairОценок пока нет

- Co Ensio Recovery Eav 02Документ7 страницCo Ensio Recovery Eav 02lucnesОценок пока нет

- Dresdner Struct Products Vicious CircleДокумент8 страницDresdner Struct Products Vicious CircleBoris MangalОценок пока нет

- VREIT - Final REIT Plan (2022 05 26) VFFДокумент1 454 страницыVREIT - Final REIT Plan (2022 05 26) VFFbptmaglinte951Оценок пока нет

- Answers To Final Exam Revision Practice QДокумент5 страницAnswers To Final Exam Revision Practice QMinSu YangОценок пока нет

- Case 4, BF - Goodrich WorksheetДокумент1 страницаCase 4, BF - Goodrich Worksheetisgigles157100% (2)

- 0205 ReposedДокумент45 страниц0205 ReposedLameuneОценок пока нет

- Understanding The 3 Financial Statements 1653805473Документ11 страницUnderstanding The 3 Financial Statements 1653805473RaikhanОценок пока нет

- Case2 Group2Документ11 страницCase2 Group2Yang ZhouОценок пока нет