Вам также может понравиться

- Credit PlanningДокумент9 страницCredit PlanningMonika Saini100% (1)

- Credit Control by RBIДокумент10 страницCredit Control by RBIRishi exportsОценок пока нет

- Brief History of RBI: Hilton Young CommissionДокумент24 страницыBrief History of RBI: Hilton Young CommissionharishОценок пока нет

- Industrial Securities MarketДокумент16 страницIndustrial Securities MarketNaga Mani Merugu100% (3)

- Profits and Gains of Business or ProfessionДокумент14 страницProfits and Gains of Business or Professionsadathnoori100% (1)

- Law and Practice of BankingДокумент2 страницыLaw and Practice of BankingJobin George100% (2)

- Modes of Charging SecuritiesДокумент11 страницModes of Charging SecuritiesKopal Agarwal50% (4)

- Special Types of CustomersДокумент17 страницSpecial Types of CustomersAakash Jain100% (1)

- Special CustomersДокумент16 страницSpecial CustomersAnuj KakkarОценок пока нет

- Banker Customer Relationship: Nature, Type - General and SpecialДокумент59 страницBanker Customer Relationship: Nature, Type - General and Specialrajin_rammsteinОценок пока нет

- Functions of SEBIДокумент6 страницFunctions of SEBIKumar Raghav MauryaОценок пока нет

- Income Tax Authorities - Power and HierarchyДокумент13 страницIncome Tax Authorities - Power and HierarchyHIMANSHI HIMANSHIОценок пока нет

- Indian Financial SystemДокумент16 страницIndian Financial Systemshankarinadar100% (1)

- Intermediaries in New Issue MarketДокумент5 страницIntermediaries in New Issue MarketSandeep Savarkar33% (3)

- Commercial BankДокумент13 страницCommercial BankVedant JhunjhunwalaОценок пока нет

- New Issue MarketДокумент13 страницNew Issue MarketKanivarasi Hercule100% (2)

- Organizational Structure, Development of Banks in IndiaДокумент54 страницыOrganizational Structure, Development of Banks in Indiaanand_lamani100% (1)

- Divisible ProfitДокумент5 страницDivisible ProfitAzhar Ahmed SheikhОценок пока нет

- Call Money MarketДокумент24 страницыCall Money MarketiyervsrОценок пока нет

- BrokersДокумент47 страницBrokersManjunath ShettigarОценок пока нет

- Collecting BankerДокумент12 страницCollecting Bankersagarg94gmailcom100% (3)

- Tandon Committee PresentationДокумент13 страницTandon Committee PresentationNitharshini Kannan0% (1)

- BoДокумент22 страницыBomonik50% (2)

- Indian Financial SystemДокумент16 страницIndian Financial SystemSarada NagОценок пока нет

- Introduction To Indian Financial SystemДокумент31 страницаIntroduction To Indian Financial SystemManoher Reddy100% (2)

- Functions of Commercial BanksДокумент19 страницFunctions of Commercial BanksAravind Kumar G100% (1)

- IRBIДокумент15 страницIRBIVicky Hatwal100% (2)

- Credit Creation & Credit ControlsДокумент31 страницаCredit Creation & Credit ControlsVishnu thankachan100% (2)

- Value Added StatementДокумент14 страницValue Added StatementInigorani0% (2)

- Main Role and Functions of RBIДокумент9 страницMain Role and Functions of RBImalathi100% (1)

- Sbi FunctionsДокумент10 страницSbi FunctionsDeepanker Bhardwaj33% (3)

- Valuation of Bonds and DebenturesДокумент10 страницValuation of Bonds and DebenturescnagadeepaОценок пока нет

- Management of Primary ReservesДокумент13 страницManagement of Primary ReservesNuhman.MОценок пока нет

- EXIM PolicyДокумент6 страницEXIM PolicyVikas ChauhanОценок пока нет

- Difference Between A Private LTD and Public LTDДокумент4 страницыDifference Between A Private LTD and Public LTDShoaib Shaik0% (1)

- Priority Sector LendingДокумент9 страницPriority Sector Lendingjhumli100% (1)

- Topic: Markowitz Theory (With Assumptions) IntroductionДокумент3 страницыTopic: Markowitz Theory (With Assumptions) Introductiondeepti sharmaОценок пока нет

- Basic Principles of Sound LendingДокумент20 страницBasic Principles of Sound LendingEknath Birari90% (21)

- Paying Banker and Collecting BankerДокумент21 страницаPaying Banker and Collecting BankerFRANCIS JOSEPH67% (3)

- Challenges For Commercial BanksДокумент6 страницChallenges For Commercial Banksshahrukhzia100% (1)

- Depository ServicesДокумент7 страницDepository ServicesakhilОценок пока нет

- Credit Control MethodsДокумент3 страницыCredit Control Methodsprasal75% (4)

- income From Salary-Problems, Theory and Solutions: by Prof - Augustin AmaladasДокумент76 страницincome From Salary-Problems, Theory and Solutions: by Prof - Augustin AmaladasAnkit Dhyani100% (6)

- Financial Aspects in RetailДокумент31 страницаFinancial Aspects in RetailPink100% (4)

- Banker's RightДокумент10 страницBanker's Rightsagarg94gmailcomОценок пока нет

- Corporate Tax PlanningДокумент21 страницаCorporate Tax Planninggauravbpit100% (3)

- Functions of Banks I Primary and SecondaryДокумент6 страницFunctions of Banks I Primary and SecondaryAmace Placement KanchipuramОценок пока нет

- Narasimham Committee Report I & IIДокумент5 страницNarasimham Committee Report I & IITejas Makwana0% (3)

- Banking Regulation Act 1949Документ17 страницBanking Regulation Act 1949Sargam MehtaОценок пока нет

- 19P0310314 - Corporate Tax Planning - Meaning, Objectives and ScopeДокумент8 страниц19P0310314 - Corporate Tax Planning - Meaning, Objectives and ScopePriya KudnekarОценок пока нет

- Insurance Service PPT MbaДокумент23 страницыInsurance Service PPT MbaBabasab Patil (Karrisatte)100% (3)

- Regulatory Framework For Banking in IndiaДокумент12 страницRegulatory Framework For Banking in IndiaSidhant NaikОценок пока нет

- Meaning and Functions of Commercial BankДокумент4 страницыMeaning and Functions of Commercial BankP Janaki Raman100% (6)

- Perform The Following Functions: I. Accepting Deposits From Public/others (Deposits) II. Lending Money To Public (Loans)Документ9 страницPerform The Following Functions: I. Accepting Deposits From Public/others (Deposits) II. Lending Money To Public (Loans)supatraОценок пока нет

- Purpose of Banks: Different Types of Bank AccountsДокумент4 страницыPurpose of Banks: Different Types of Bank Accountsneilbryan bolañoОценок пока нет

- What Is Credit Creation?Документ6 страницWhat Is Credit Creation?WondaferewChalaОценок пока нет

- Assignment 23550Документ6 страницAssignment 23550WondaferewChalaОценок пока нет

- What Is Credit Creation?Документ6 страницWhat Is Credit Creation?WondaferewChalaОценок пока нет

- Explain Origin of Commercial BankingДокумент6 страницExplain Origin of Commercial Bankingዳግማዊ ጌታነህ ግዛው ባይህОценок пока нет

- Indian Bank Home LoanДокумент60 страницIndian Bank Home Loanriyazmaideen17Оценок пока нет

- Refund and Bursary Payout Form March 2018a.zp177151Документ1 страницаRefund and Bursary Payout Form March 2018a.zp177151Lucas NongОценок пока нет

- Make Money Fast With Cash Fiesta (New Version)Документ10 страницMake Money Fast With Cash Fiesta (New Version)Phi Van HoeОценок пока нет

- Obli AnswersДокумент3 страницыObli AnswersDakila MaloyОценок пока нет

- Introduction To AccountingДокумент180 страницIntroduction To Accountingmuzamilmf5Оценок пока нет

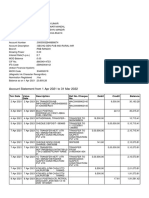

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент14 страницAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandОценок пока нет

- SV - INFO 31787 Accounting Information Systems Midterm Theory Exam - Summer 2017 Version A1 PDFДокумент7 страницSV - INFO 31787 Accounting Information Systems Midterm Theory Exam - Summer 2017 Version A1 PDFGamersОценок пока нет

- Bank Reconciliation StatementДокумент27 страницBank Reconciliation Statementkimuli FreddieОценок пока нет

- Suggested Answer NilДокумент27 страницSuggested Answer NilAndrei ArkovОценок пока нет

- Isave Account Terms and ConditionsДокумент10 страницIsave Account Terms and Conditionsfennie ilinah molinaОценок пока нет

- Cash and Cash EquivДокумент8 страницCash and Cash EquivMonina Cabalag0% (1)

- PCLaw7 Instructions Cheats (18.10.2007)Документ15 страницPCLaw7 Instructions Cheats (18.10.2007)Lc KohОценок пока нет

- PCBUДокумент1 страницаPCBUchityalasriaktnh0000Оценок пока нет

- LIC Housing Finance LTD FDДокумент6 страницLIC Housing Finance LTD FDDwiref VoraОценок пока нет

- Penyata Kad / Card Statement: Yap Foot Kean 11A JALAN SS2/28 47300 Petaling Jaya 12 SEP 2023 RM 10,000 02 OCT 2023Документ4 страницыPenyata Kad / Card Statement: Yap Foot Kean 11A JALAN SS2/28 47300 Petaling Jaya 12 SEP 2023 RM 10,000 02 OCT 2023waiwahphinОценок пока нет

- Revenue Officer-Fesco Application Form PDFДокумент3 страницыRevenue Officer-Fesco Application Form PDFMuhammad SaadОценок пока нет

- Eimas Cepswam 2023 GreenvellДокумент4 страницыEimas Cepswam 2023 GreenvellnajihahОценок пока нет

- Payment Systems Part 1Документ282 страницыPayment Systems Part 1ashimadania100% (2)

- Payment: Commercial CorrespondenceДокумент8 страницPayment: Commercial CorrespondencestrawberryktОценок пока нет

- MANULIFE Policy Holder's GuideДокумент29 страницMANULIFE Policy Holder's GuidelexxОценок пока нет

- Statement of Account For The Period 01-Jun-2020 To 23-May-2021Документ23 страницыStatement of Account For The Period 01-Jun-2020 To 23-May-2021Chandrakanth KhannaОценок пока нет

- Green Banking Practice in BangladeshДокумент48 страницGreen Banking Practice in BangladeshAshiq Hossain100% (5)

- Manupatra 7303Документ2 страницыManupatra 7303Karthik SaranganОценок пока нет

- AudДокумент46 страницAudJane ConstantinoОценок пока нет

- Internship Report ON A Review of Financial Situation of Krishi BankДокумент36 страницInternship Report ON A Review of Financial Situation of Krishi BankNur H PalashОценок пока нет

- Telephone Number, Fax and E-Mail Address Spain Andalusia RíofrioДокумент2 страницыTelephone Number, Fax and E-Mail Address Spain Andalusia Ríofriofadilah kamalОценок пока нет

- Loan Approval Process (Commercial and Consumer Loans)Документ8 страницLoan Approval Process (Commercial and Consumer Loans)Vinit JetwaniОценок пока нет

- Standing Order FormДокумент3 страницыStanding Order FormMaissa Hassan100% (1)

- Wa0006.Документ32 страницыWa0006.Abhirami RОценок пока нет

- Electricity Bill: Due Date: 11-07-2011Документ1 страницаElectricity Bill: Due Date: 11-07-2011Anjani GroverОценок пока нет