Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Karv Nestle Co 60Документ3 страницыKarv Nestle Co 60mittleОценок пока нет

- Karv Nestle Co 51Документ3 страницыKarv Nestle Co 51mittleОценок пока нет

- Funding Position of Banks Improving. Spanish Banks'Документ3 страницыFunding Position of Banks Improving. Spanish Banks'mittleОценок пока нет

- 6) The EM Story Is Not Played Out, Though Future Outperformance Is Likely To Be More ModestДокумент4 страницы6) The EM Story Is Not Played Out, Though Future Outperformance Is Likely To Be More ModestmittleОценок пока нет

- Three Key Surprises For 2011: Ronan Carr, CFAДокумент3 страницыThree Key Surprises For 2011: Ronan Carr, CFAmittleОценок пока нет

- Karv Nestle Co 69Документ3 страницыKarv Nestle Co 69mittleОценок пока нет

- Karv Nestle Co 78Документ3 страницыKarv Nestle Co 78mittleОценок пока нет

- Valuation Dispersion Has Widened by 1SD Since Sep: Exhibit 46Документ4 страницыValuation Dispersion Has Widened by 1SD Since Sep: Exhibit 46mittleОценок пока нет

- Morg Stan 3Документ4 страницыMorg Stan 3mittleОценок пока нет

- Water Market Insights 1Документ5 страницWater Market Insights 1mittleОценок пока нет

- Morg Stan 2Документ4 страницыMorg Stan 2mittleОценок пока нет

- ISO Country Codes: Government Commonly Exerts Great Influence On Water IndustryДокумент5 страницISO Country Codes: Government Commonly Exerts Great Influence On Water IndustrymittleОценок пока нет

- Morg Stan 4Документ4 страницыMorg Stan 4mittleОценок пока нет

- Water Market Insights 5Документ8 страницWater Market Insights 5mittleОценок пока нет

- DB Food Insights 3Документ9 страницDB Food Insights 3mittleОценок пока нет

- Water Market Insights 4Документ5 страницWater Market Insights 4mittleОценок пока нет

- DB Food Insights 2Документ9 страницDB Food Insights 2mittleОценок пока нет

- DB Food Insights 1Документ9 страницDB Food Insights 1mittleОценок пока нет

- JSW Steel LTD Results ReviewДокумент7 страницJSW Steel LTD Results ReviewmittleОценок пока нет

- Water Market Insights 3Документ5 страницWater Market Insights 3mittleОценок пока нет

- DB Food Insights 4Документ9 страницDB Food Insights 4mittleОценок пока нет

- MacroEco Initiate BuyДокумент21 страницаMacroEco Initiate BuymittleОценок пока нет

- DB Food Insights 5Документ4 страницыDB Food Insights 5mittleОценок пока нет

- Capex JSWE InitiateДокумент13 страницCapex JSWE InitiatemittleОценок пока нет

- BGR Upside Buy RecoДокумент11 страницBGR Upside Buy RecomittleОценок пока нет

- Kotak Stratgy Whose Wealth Report PDFДокумент5 страницKotak Stratgy Whose Wealth Report PDFmittleОценок пока нет

- BGR Report Q4 2011 PDFДокумент4 страницыBGR Report Q4 2011 PDFmittleОценок пока нет

- JSWE Results ReviewДокумент7 страницJSWE Results ReviewmittleОценок пока нет

- Gujrat On The RoadДокумент15 страницGujrat On The RoadmittleОценок пока нет

- Sugar Space Update 2010Документ2 страницыSugar Space Update 2010mittleОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- EvalyДокумент14 страницEvalyIslam MajharulОценок пока нет

- Ordertrust Inc.: One-Stop Order Management Services For E-CommerceДокумент16 страницOrdertrust Inc.: One-Stop Order Management Services For E-CommerceMaribel EcheniqueОценок пока нет

- EcommerceДокумент59 страницEcommerceKyuoko TsugameiОценок пока нет

- E-Tailing/electronic Retailing Dissertation PresentationДокумент28 страницE-Tailing/electronic Retailing Dissertation PresentationSatyabrata SahuОценок пока нет

- Top 10 Pci Dss Compliance PitfallsДокумент4 страницыTop 10 Pci Dss Compliance PitfallsdurgasainathОценок пока нет

- 1 19 15Документ45 страниц1 19 15api-281708263Оценок пока нет

- NRF-MRI-Blueprint v1.0.0 Full VersionДокумент177 страницNRF-MRI-Blueprint v1.0.0 Full VersionJonatan Evald BuusОценок пока нет

- Cyber Law II Unit 4Документ17 страницCyber Law II Unit 4Vidhi LoyaОценок пока нет

- Thomas Harris CV 2023Документ3 страницыThomas Harris CV 2023Thanh X TranОценок пока нет

- McKinsey Profile Up1 1201Документ94 страницыMcKinsey Profile Up1 1201007003sОценок пока нет

- How To Create A Self-Signed SSL CertificateДокумент4 страницыHow To Create A Self-Signed SSL CertificatesuttoraОценок пока нет

- Effective Internet Marketing Strategies For Online Food Businesses in Rizal Province III BTLEDДокумент31 страницаEffective Internet Marketing Strategies For Online Food Businesses in Rizal Province III BTLEDJM100% (1)

- Assignment: Kurbanova RabiyamДокумент12 страницAssignment: Kurbanova Rabiyamrabiyam100% (2)

- 1.1 ICT (Information and Communications Technology)Документ15 страниц1.1 ICT (Information and Communications Technology)abs shakilОценок пока нет

- Buy Bitcoin Instantly Noones 2Документ1 страницаBuy Bitcoin Instantly Noones 2yj74865fc9Оценок пока нет

- 29-CM-STE ManualДокумент46 страниц29-CM-STE ManualRitesh Jadhav100% (1)

- Future of B2B Sales The Big ReframeДокумент37 страницFuture of B2B Sales The Big ReframeDental Wiz50% (2)

- 1 Intro To EC Concepts 2019Документ25 страниц1 Intro To EC Concepts 2019уавдОценок пока нет

- E-Business and E-Commerce Management - Book ReviewДокумент2 страницыE-Business and E-Commerce Management - Book ReviewTô Lê Minh ThanhОценок пока нет

- E-Commerce - Vogue HiveДокумент42 страницыE-Commerce - Vogue HiveAlok jhaОценок пока нет

- Sample StraMa Paper of Puregold From San Beda CollegeДокумент86 страницSample StraMa Paper of Puregold From San Beda CollegeLheanne Zacarias RectoОценок пока нет

- TalentPop Questions PDFДокумент3 страницыTalentPop Questions PDFlizzawambo9Оценок пока нет

- Practical Issues With TLS Client CertificateДокумент13 страницPractical Issues With TLS Client Certificatelucassamuel_777Оценок пока нет

- 305 MKT: Sales & Distribution ManagementДокумент2 страницы305 MKT: Sales & Distribution ManagementDr. Milind Narayan DatarОценок пока нет

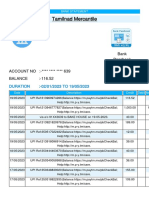

- Tamilnad Mercantile1684550531048Документ25 страницTamilnad Mercantile1684550531048Miracle KhordsОценок пока нет

- AOC SAQ D v20 - Service ProviderДокумент5 страницAOC SAQ D v20 - Service ProviderprinsessafionaОценок пока нет

- PetMeds Analysis 2Документ10 страницPetMeds Analysis 2Марго КоваленкоОценок пока нет

- Reaching Strategic EdgeДокумент14 страницReaching Strategic EdgeVivek ReddyОценок пока нет

- Introduction To E-Commerce: Lecturer: MS Lam Hong Thanh Email: Thanhlh@uel - Edu.vnДокумент20 страницIntroduction To E-Commerce: Lecturer: MS Lam Hong Thanh Email: Thanhlh@uel - Edu.vnAmieОценок пока нет

- SAML Integration GuideДокумент13 страницSAML Integration GuideDaren DarrowОценок пока нет