Вам также может понравиться

- Multiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetДокумент15 страницMultiple Choice: Shade The Box Corresponding To Your Answer On The Answer SheetRhad EstoqueОценок пока нет

- Quality Control SystemДокумент4 страницыQuality Control SystemGlessey Mae Baito LuvidicaОценок пока нет

- Audit Theory QuizzerДокумент71 страницаAudit Theory QuizzerKriztleKateMontealtoGelogoОценок пока нет

- Auditing Theory AuditДокумент77 страницAuditing Theory AuditAdam Smith0% (1)

- Feu - MakatiДокумент15 страницFeu - MakatiRica RegorisОценок пока нет

- AT Q1 Pre-Week - MAY 2019Документ17 страницAT Q1 Pre-Week - MAY 2019Aj Pacaldo100% (3)

- AGS CUP 6 Auditing Final RoundДокумент19 страницAGS CUP 6 Auditing Final RoundKenneth RobledoОценок пока нет

- Long Quiz 2Документ8 страницLong Quiz 2CattleyaОценок пока нет

- MANAGEMENT ADVISORY SERVICES BREAKEVENДокумент46 страницMANAGEMENT ADVISORY SERVICES BREAKEVENJoy Bernadette GruesoОценок пока нет

- Mock Cpa Board Exams Rfjpia R 12 WДокумент17 страницMock Cpa Board Exams Rfjpia R 12 Wlongix100% (2)

- Solving Construction Problems Step-by-StepДокумент6 страницSolving Construction Problems Step-by-StepAlexОценок пока нет

- General Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedДокумент2 страницыGeneral Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedRaca DesuОценок пока нет

- TxqnaДокумент31 страницаTxqnaJames Scold100% (1)

- Advac Solmal Chapter 13Документ16 страницAdvac Solmal Chapter 13john paul100% (1)

- Exam 3Документ8 страницExam 3Julie Ann Canlas0% (1)

- CPA ethics and principlesДокумент2 страницыCPA ethics and principlesMichОценок пока нет

- 09 X07 C ResponsibilityДокумент9 страниц09 X07 C ResponsibilityAnjo PadillaОценок пока нет

- DRAFTLevel 3Документ129 страницDRAFTLevel 3Mark Paul RamosОценок пока нет

- CHAPTER 7 Auditing-Theory-MCQs-by-Salosagcol-with-answersДокумент2 страницыCHAPTER 7 Auditing-Theory-MCQs-by-Salosagcol-with-answersMichОценок пока нет

- Substantive Test Cash and Cash Equivalents QuizДокумент2 страницыSubstantive Test Cash and Cash Equivalents QuizMarieОценок пока нет

- Salosagcol CompilationДокумент19 страницSalosagcol CompilationJasmine Lim100% (1)

- Long-Term Construction Contracts (Pfrs 15) : Start of DiscussionДокумент3 страницыLong-Term Construction Contracts (Pfrs 15) : Start of DiscussionErica DaprosaОценок пока нет

- AFAR Review Net Asset AcquisitionДокумент12 страницAFAR Review Net Asset AcquisitionThom Santos Crebillo100% (1)

- AssignmentДокумент2 страницыAssignmentAisha FajardoОценок пока нет

- CPA Exam Chapter 2 ReviewДокумент7 страницCPA Exam Chapter 2 Reviewlopo100% (1)

- Business Combinations ExplainedДокумент8 страницBusiness Combinations ExplainedLabLab ChattoОценок пока нет

- Cebu CPAR Mandaue City FINAL PREBOARD EXAMINATION AUDITING PROBLEMSДокумент9 страницCebu CPAR Mandaue City FINAL PREBOARD EXAMINATION AUDITING PROBLEMSLoren Lordwell MoyaniОценок пока нет

- AFAR May2021 1st Preboard With AnswerДокумент28 страницAFAR May2021 1st Preboard With Answerlllll100% (2)

- Metro Manila College: College of Business and AccountancyДокумент8 страницMetro Manila College: College of Business and AccountancyJeric TorionОценок пока нет

- Pfrs 15Документ4 страницыPfrs 15Roy Mitz Aggabao Bautista VОценок пока нет

- AUDITINGДокумент11 страницAUDITINGMaud Julie May FagyanОценок пока нет

- Nfjpia R12 Mock Board Examination: Page 1 of 8Документ8 страницNfjpia R12 Mock Board Examination: Page 1 of 8Leane MarcoletaОценок пока нет

- Answer: D. This Is A Function of Banks or Banking InstitutionsДокумент6 страницAnswer: D. This Is A Function of Banks or Banking InstitutionsKurt Del RosarioОценок пока нет

- Brilliant Cosmetics 2017 financial statement adjustmentsДокумент3 страницыBrilliant Cosmetics 2017 financial statement adjustmentsVilma Tayum100% (1)

- Department of Accountancy: Page - 1Документ18 страницDepartment of Accountancy: Page - 1Noro0% (1)

- AccAud ProbДокумент9 страницAccAud ProbCarlo Frio100% (1)

- 1PB - Ar6Документ12 страниц1PB - Ar6KimОценок пока нет

- REVIEW OF AUDITING THEORYДокумент12 страницREVIEW OF AUDITING THEORYLlyod Francis LaylayОценок пока нет

- Drill Problems - ConsolidationДокумент6 страницDrill Problems - Consolidationgun attaphanОценок пока нет

- Aud Theo Dept. MIDTERM EXAMДокумент8 страницAud Theo Dept. MIDTERM EXAMChristine Joy OriginalОценок пока нет

- James HallДокумент8 страницJames Hallyunusprasetyo21Оценок пока нет

- Ans: D: Multiple ChoiceДокумент14 страницAns: D: Multiple ChoiceNah HamzaОценок пока нет

- This Study Resource Was: Multiple Choice QuestionsДокумент7 страницThis Study Resource Was: Multiple Choice QuestionsCarol PagalОценок пока нет

- CHAPTER 8 Auditing-Theory-MCQs-by-Salosagcol-with-answersДокумент1 страницаCHAPTER 8 Auditing-Theory-MCQs-by-Salosagcol-with-answersMichОценок пока нет

- RFBT Q 1 2Документ63 страницыRFBT Q 1 2Sean SanchezОценок пока нет

- Quiz Acctng 603Документ10 страницQuiz Acctng 603LJ AggabaoОценок пока нет

- STRATEGIC COSTMan QUIZ 3Документ5 страницSTRATEGIC COSTMan QUIZ 3StephannieArreolaОценок пока нет

- MASДокумент3 страницыMASjoenalynОценок пока нет

- Final Exam - Strategic - OVILLOДокумент4 страницыFinal Exam - Strategic - OVILLOMaria Angelica100% (1)

- MAS AbitiagoДокумент6 страницMAS AbitiagoJoris YapОценок пока нет

- Comprehensive Exam Part 1 QuestionnaireДокумент9 страницComprehensive Exam Part 1 QuestionnaireMac b IBANEZОценок пока нет

- MAS First Monthly AssessmentДокумент10 страницMAS First Monthly AssessmentdsndcwnnfnhОценок пока нет

- Instructions: Cpa Review School of The PhilippinesДокумент17 страницInstructions: Cpa Review School of The PhilippinesCyn ThiaОценок пока нет

- Managerial Accounting Sample ExamДокумент4 страницыManagerial Accounting Sample ExamJerome Delos Reyes100% (1)

- Pre FinalДокумент8 страницPre Finalpdmallari12Оценок пока нет

- Take Home Midterms Mix 30Документ6 страницTake Home Midterms Mix 30rizzelОценок пока нет

- Intermediate 1Документ11 страницIntermediate 1Mary Anne ManaoisОценок пока нет

- Management Advisory Services (MAS)Документ10 страницManagement Advisory Services (MAS)jaymark canaya50% (2)

- Strategic Management - Midterm Quiz 2Документ5 страницStrategic Management - Midterm Quiz 2Uy Samuel0% (1)

- MS-MidtermExam 5thyrABSA 2019 AnsДокумент8 страницMS-MidtermExam 5thyrABSA 2019 AnsKarla OñasОценок пока нет

- Loca Gov't Units ReviewerДокумент2 страницыLoca Gov't Units ReviewerFrancine HollerОценок пока нет

- AUDProb TEST BANKДокумент28 страницAUDProb TEST BANKFrancine HollerОценок пока нет

- Audit of Inventories - STДокумент7 страницAudit of Inventories - STFrancine Holler0% (2)

- Negotiable Instruments ReviewerДокумент1 страницаNegotiable Instruments ReviewerFrancine HollerОценок пока нет

- Auditing and internal controlsДокумент3 страницыAuditing and internal controlsFrancine Holler67% (3)

- Professional Responsibilities (AUD THEO)Документ5 страницProfessional Responsibilities (AUD THEO)Francine HollerОценок пока нет

- DANKOTUWA PORCELAIN ANNUAL REPORT 2017/18Документ184 страницыDANKOTUWA PORCELAIN ANNUAL REPORT 2017/18DinukaDeshanОценок пока нет

- Convertible SecuritiesДокумент10 страницConvertible SecuritiesLoren RosariaОценок пока нет

- Financial Performance AnalysisДокумент18 страницFinancial Performance AnalysisVineet SwamiОценок пока нет

- Mechanics of Financial Accounting RevisedДокумент4 страницыMechanics of Financial Accounting RevisedalakshendraОценок пока нет

- Cpa Review School of The Philippines ManilaДокумент5 страницCpa Review School of The Philippines ManilaAljur SalamedaОценок пока нет

- Sambung Bab 2Документ30 страницSambung Bab 2Shanti GunaОценок пока нет

- Parliamentary Committee Report Lok Sabha On Companies Bill 2011Документ111 страницParliamentary Committee Report Lok Sabha On Companies Bill 2011anielnair5695Оценок пока нет

- Final Guidelines For Payment BanksДокумент3 страницыFinal Guidelines For Payment BanksAnkaj MohindrooОценок пока нет

- Rothschild Bank AG Annual Report 2011/2012Документ60 страницRothschild Bank AG Annual Report 2011/2012blyzerОценок пока нет

- Cpa Review School of The Philippines ManilaДокумент5 страницCpa Review School of The Philippines ManilaSamuel Cedrick AbalosОценок пока нет

- Contoh Soal - Ch15Документ52 страницыContoh Soal - Ch15Nurhanifah SoedarsОценок пока нет

- Free Cash FlowsДокумент8 страницFree Cash FlowsParvesh AghiОценок пока нет

- Taxation of Corporations GuideДокумент4 страницыTaxation of Corporations GuideJohn Kayle BorjaОценок пока нет

- Straight Line MethodДокумент3 страницыStraight Line MethodKhaez Almariego CaindoyОценок пока нет

- Student Number (UWL Registration Number) : 21452742 Assignment Name: Consolidation and Analysis On The MusicalДокумент19 страницStudent Number (UWL Registration Number) : 21452742 Assignment Name: Consolidation and Analysis On The MusicalSavithri NandadasaОценок пока нет

- Disclosure Guide Matrix: A Comprehensive Disclosure Checklist For The GIPS StandardsДокумент27 страницDisclosure Guide Matrix: A Comprehensive Disclosure Checklist For The GIPS StandardsMartin RosОценок пока нет

- Mas Must AnswersДокумент15 страницMas Must AnswersX YlmarixeОценок пока нет

- Factsheet - 0305709591 - CONG TY CO PHAN PHONG PHU SAC VIET - Company ReportДокумент10 страницFactsheet - 0305709591 - CONG TY CO PHAN PHONG PHU SAC VIET - Company ReportHung NguyenОценок пока нет

- Cash BudgetДокумент3 страницыCash Budgetkeshav madamОценок пока нет

- Adjusting Journal EntryДокумент52 страницыAdjusting Journal EntryJenny PadillaОценок пока нет

- Audit of Cash PDFДокумент3 страницыAudit of Cash PDFVincent SampianoОценок пока нет

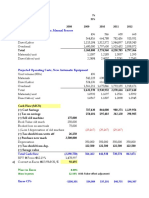

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Документ4 страницыProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyОценок пока нет

- Capital & Derivatives MarketДокумент12 страницCapital & Derivatives Marketvikas_bhatia2007Оценок пока нет

- ACT 202 Project Master Budgeting Naznin Islam Nipa 1512356030Документ5 страницACT 202 Project Master Budgeting Naznin Islam Nipa 1512356030Naznin NipaОценок пока нет

- Wave 1 Toa AnswersДокумент7 страницWave 1 Toa AnswerschelissamaerojasОценок пока нет

- TMS Boutique Profit Loss 2020Документ2 страницыTMS Boutique Profit Loss 2020Syaza AisyahОценок пока нет

- Cel 1 Prac 1 Answer KeyДокумент15 страницCel 1 Prac 1 Answer KeyNJ MondigoОценок пока нет

- Capital Budgeting Techniques and Project EvaluationДокумент12 страницCapital Budgeting Techniques and Project EvaluationIfraОценок пока нет

- How To Account For Investment in Gold Under IFRS - CPDbox - Making IFRS EasyДокумент13 страницHow To Account For Investment in Gold Under IFRS - CPDbox - Making IFRS Easytunlinoo.067433Оценок пока нет

- Fundamentals AnswerДокумент12 страницFundamentals AnswerRienalyn Dumlao Duldulao-DaligconОценок пока нет